Last updated: June 22, 2026

Lipitor (atorvastatin) market dynamics and financial trajectory: exclusivity, generics, and revenue exposure

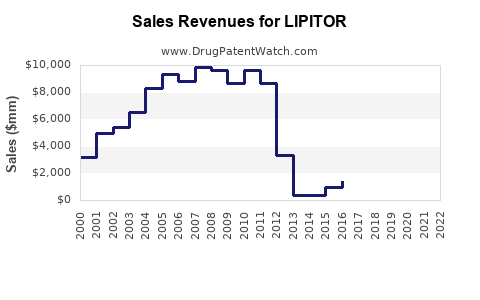

Lipitor (atorvastatin) has moved from brand exclusivity into a mature, heavily genericized statin market. The brand’s revenue trajectory is now driven mainly by (1) residual pricing, (2) remaining managed-care positioning in high-value accounts, (3) payer restrictions versus competing statins, and (4) generic consolidation risk and margin compression among suppliers. Patent-driven pricing power ended early versus U.S. cash peaks, so financial performance since then has tracked market share losses to low-cost generics and pricing dynamics rather than clinical differentiation.

How did Lipitor’s revenue evolve after FDA approval and into generic competition?

Executive answer

Lipitor’s financial trajectory followed a typical pattern for a blockbuster whose core U.S. patent and exclusivity headroom expired, followed by rapid generic share loss and sustained price erosion.

Key demand drivers

- Clinical class adoption: Statins became standard of care for primary and secondary prevention, supporting long duration of demand despite brand erosion.

- Formulary mechanics: Over time, payers steered to lower-cost statins, first via therapeutic interchange and later via explicit formulary restriction to generic atorvastatin.

- Dose breadth: Lipitor’s established dosing range supported wide prescribing across risk tiers, making it easy for prescribers to keep “atorvastatin” even after brand replacement.

- Switching inertia: Lipitor maintained baseline demand after patent expiry because clinicians often continue the same molecule when tolerated.

Generic impact pattern

- Early generics moved the market from branded premium pricing to commodity-level pricing.

- Later entrant consolidation reduced competition at the supplier level but did not restore brand-like pricing because reimbursement and contracting kept prices low.

When did Lipitor lose exclusivity in the U.S. and what changed in the market afterward?

Executive answer

Lipitor’s U.S. brand exclusivity and patent protections ended, enabling generic atorvastatin entry and accelerating brand revenue decline. After generic entry, market dynamics were dominated by pricing and payer contracting rather than IP barriers.

Exclusivity framework

For small-molecule drugs like atorvastatin, revenue protection typically relied on:

- Composition-of-matter patent families (active ingredient and key chemical forms)

- Method-of-use claims (statin therapeutic uses)

- Formulation/process claims for specific dosage forms or manufacturing methods

Once those barriers were cleared, the commercial trajectory largely became a function of:

- Generic penetration speed

- State of payer formularies

- Gross-to-net pressure from rebates and contracting

Market outcomes post-entry

- Net price compression: Brand net pricing declines quickly as patients and prescribers shift to generic substitutes.

- Share displacement: Even where a brand retains some usage, the economic value shifts to volume-based and contract-driven business.

- Margin squeeze: The brand’s operating economics are pressured as the company shifts from brand premium pricing to defending limited share.

What patents protect Lipitor (atorvastatin) and how does the estate affect commercialization?

Executive answer

Lipitor’s patent estate historically covered atorvastatin compositions and related claims, with later layers sometimes addressing specific uses or formulations. For commercialization, what matters is whether claims block generic “same drug” entry or only constrain specific formulations or labeling positions.

How patent scope maps to business risk

- Composition-of-matter expiry is the largest commercial inflection for a generic entry timeline.

- Method-of-use claims can delay generic substitution for specific indications, but statins have broad clinical guidance, which often limits the practical ability to preserve brand dominance solely through use claims.

- Formulation/process claims can affect launch timing for certain dosage forms, but generic atorvastatin has multiple commercially established manufacturing routes.

Where the estate mattered most

- The estate mattered most during the window when payers had not locked in generic substitution contracts.

- After broad generic adoption, the brand typically competed on remaining protected territory, account-level contracts, and prescriber behavior.

Which companies sell generic atorvastatin and how does their competition affect Lipitor pricing and volumes?

Executive answer

Generic atorvastatin competition is high and pricing is contract-driven. The competitive set includes large multiproduct generic manufacturers and API/supply-chain participants, producing persistent downward price pressure.

Competitive mechanism

- Wholesale acquisition and rebate dynamics: Generic discounts and rebates drive net price down across channels.

- Contracting: Pharmacy benefit managers (PBMs) and large insurers negotiate aggressive discounts after generic acceptance.

- Supplier margin behavior: If suppliers face capacity constraints, prices can spike temporarily. Over time, additional supply reverts market pricing toward low levels.

Business implication for Lipitor

- Lipitor’s ability to maintain profitable revenue depends on:

- limited niches where brand is still preferred or restricted away from some competitors, and

- managed-care contracts that keep at least a portion of patient share on the brand.

How does Lipitor’s market share compare with other statins like Crestor (rosuvastatin) and Zocor (simvastatin)?

Executive answer

Lipitor has historically been a dominant statin in the U.S. due to high clinician familiarity and broad prescribing, but its share has faced sustained pressure from all generic statins, including rosuvastatin and simvastatin. Competitive dynamics are mostly about relative net price, payer formulary placement, and dose-response comfort.

Comparison dimensions that affect payer behavior

- Potency and dosing flexibility: Atorvastatin offers a wide dose range with strong LDL-lowering performance.

- Tolerance and switching: Prescribers prefer staying on the same statin if effective; however, payer-driven switching to cheaper options can occur.

- Formulary tiering: Preferred tiers often go to the lowest-cost agents meeting outcomes targets.

What generic entry risks exist for Lipitor and what would trigger faster erosion?

Executive answer

Once composition and key barriers were cleared, the remaining “risk” for Lipitor shifted from legal timing to market structure: incremental generic entrants, supply expansions, and PBM tier changes that reduce residual brand usage.

Triggers for additional share loss

- PBM formulary reassessment moving atorvastatin brands to non-preferred status

- Aggressive contracting by large generic wholesalers

- Broader adoption of therapeutic substitution protocols

- New supply chain capacity changes for generic atorvastatin

Trigger types

- Short-cycle: formulary and contracting changes can reprice the market within quarters.

- Structural: generic consolidation or new manufacturing capacity can reset price floors.

What is the Orange Book status of Lipitor and how do Orange Book listings shape launch timelines?

Executive answer

Orange Book listings historically tied Lipitor’s exclusivity to specific patents and exclusivity codes. For market dynamics, the Orange Book is the operational map used in Paragraph IV timing and for assessing whether a generic can file and when it can launch.

How listings translate to business decisions

- Patents listed for the drug product and related strengths dictate whether generic challengers can target “same” active moiety, dosage form, and route.

- Exclusivity codes determine whether even an unchallenged patent landscape still bars generic launch.

Commercial effect

Once Orange Book barriers clear, the expected outcome is:

- rapid replacement prescribing,

- steep price compression,

- sustained margin pressure across the brand’s remaining volume.

How does regulatory pathway history (505(b)(2), ANDA) affect the atorvastatin generic landscape?

Executive answer

For Lipitor’s molecule, most generic entries occur via ANDA pathways referencing FDA-approved atorvastatin labeling. The major regulatory barrier historically was patent and exclusivity rather than scientific reformulation hurdles.

Why regulatory pathway matters less post-barrier

- Generic atomization is straightforward for a stable small molecule.

- Once patents and exclusivity allow launch, regulatory approval becomes a gating function that is usually met quickly for multiple entrants.

What formulation or method-of-use patents mattered most for Lipitor’s protected revenue window?

Executive answer

For a blockbuster small molecule, formulation and method-of-use patents matter mainly when they can delay a specific generic dosage form or block a targeted indication. For Lipitor, market-wide adoption of generic atorvastatin means that method-of-use constraints typically do not stop broad therapeutic interchange at scale once major barriers expire.

Typical claim categories and commercial effect

- Extended-release formulations: relevant if the molecule has protected delivery systems.

- Specific patient populations/indications: relevant if labels are narrow and generic cannot use the same indication.

- Manufacturing processes: relevant if they require unique steps that raise generic development time, but rarely restore brand economics.

How do patent litigation and settlements affect Lipitor generics and timing of erosion?

Executive answer

Patent litigation involving Lipitor historically influenced timing for specific generic entrants. However, once core barriers expired and broad generic acceptance occurred, the dominant driver of Lipitor revenue became pricing and formulary behavior rather than incremental litigation delays.

Litigation channels that alter revenue

- Paragraph IV settlements can delay launch for some challengers.

- Adverse court outcomes can trigger quick launch for multiple ANDA filers.

- Injunctions can temporarily preserve brand volumes but typically fade once all key barriers clear.

What is the financial trajectory of Lipitor for the brand owner and how should investors model it?

Executive answer

Model Lipitor as a declining brand with residual share, where:

- revenue declines are driven by ongoing generic substitution and net pricing erosion, and

- inflection points occur only when competitive intensity or payer formularies change.

Investor modeling structure

- Volume: declines as generics gain share, with residual stickiness from tolerated patients and prescribing habits.

- Price (net): declines due to contracting and gross-to-net dynamics.

- Mix: any changes in dose mix affect net pricing and rebates but do not reverse the commodity structure once generic competition dominates.

Business exposure endpoints

- Downside: steeper PBM tiering changes or faster generic penetration.

- Upside: temporary brand-preferred contracting or slower payer migration in specific geographies.

How does Lipitor’s geographic market exposure influence revenue and competitive outcomes?

Executive answer

Lipitor’s geographic revenue dynamics track local generic launch timelines, local pricing regulation and reimbursement policies, and each country’s market structure (number of generic suppliers and PBM contracting practices where applicable).

Key geographic levers

- Patent enforcement and litigation tempo: affects whether certain countries see earlier or later generic entry.

- Pricing regulation: in some markets, government or payer-set prices compress brand revenues faster once generics appear.

- Generic supply density: more entrants accelerate price erosion.

Key Takeaways

- Lipitor’s financial trajectory is now primarily a function of generic substitution, contracting, and pricing compression, not new clinical differentiation or ongoing core IP.

- The post-exclusivity period created a stable pattern: rapid share loss, sustained net price erosion, and residual volume supported by payer behavior and clinical inertia.

- Remaining competitive sensitivity is tied to PBM formularies, contracting changes, and generic supply intensity.

- Patent and Orange Book status historically drove launch timing; once major barriers cleared, market structure became the primary determinant of brand revenue outcomes.

FAQs

1) What factors determine residual Lipitor brand share after generic atorvastatin launches?

Payer formulary tiering, rebate and contracting structure, patient switching behavior, and prescriber preference for maintaining a tolerated statin regimen.

2) Do method-of-use patents meaningfully delay generic competition for Lipitor indications?

They can delay specific carve-outs if generic labeling cannot be used, but broad statin guideline adoption and therapeutic interchange usually limit long-run impact.

3) How do PBM contracting changes typically show up in Lipitor financials?

They usually affect net pricing and volume quickly through tiering, formulary restrictions, and rebate renegotiations across affected lines of business.

4) What is the main commercial risk for Lipitor in mature generic markets?

Margin compression from low generic net prices combined with any incremental shift of patient volume away from the brand due to formulary and pharmacy benefit changes.

5) How should competitors position against Lipitor in a fully genericized statin environment?

Against a commodity molecule, differentiation depends on net cost to payers, formulary strategy, supply reliability, and patient-support programs rather than IP-led barriers.

References

- FDA. Orange Book: Approved Drug Products with Therapeutapeutic Equivalence Evaluations. U.S. Food and Drug Administration.

- FDA. Drug Approval Reports and Labeling for Lipitor (atorvastatin). U.S. Food and Drug Administration.