Last updated: April 24, 2026

Linezolid is a synthetic oxazolidinone antibacterial whose commercial cycle has shifted from exclusivity-led growth to largely generic-driven volume with persistent demand from hard-to-treat Gram-positive infections. Financial outcomes track patent expiry and competitive entry timing across major markets, with revenue increasingly concentrated in hospital formularies, antimicrobial stewardship, and payer policies that favor lowest-cost options once generics are approved.

How has linezolid’s market structure evolved?

What was the exclusivity-to-generic transition path?

Linezolid’s originator position was supported by first-in-class and broad clinical adoption in complicated skin and soft tissue infections (cSSSI) and hospital-acquired and ventilator-associated pneumonia (HAP/VAP), including MRSA and VRE settings. The market then moved through a series of “barrier breaks” driven by generic approvals.

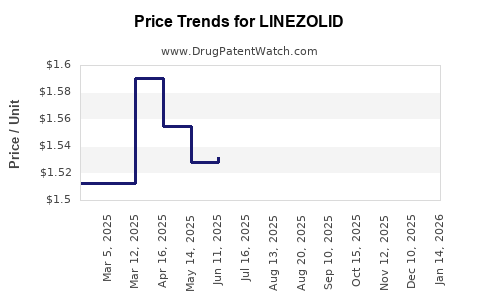

Commercial consequence: the product’s revenue curve typically shows a high plateau during brand exclusivity, followed by step-downs in price and margin as oral and IV generic portfolios expand in each geography. Persistent clinical use keeps the addressable volume from collapsing, but pricing follows a generic descent.

Where does demand come from now?

Linezolid’s demand drivers remain durable:

- Hospital-focused prescribing for resistant Gram-positive pathogens (MRSA, VRE) and infections where alternatives are limited by resistance patterns.

- Formulary placement tied to stewardship protocols that manage broad-spectrum use and linezolid access windows.

- Dosing convenience (IV-to-oral switch) that supports throughput and reduces inpatient stay friction compared with some alternatives.

Competitive set

In most markets, linezolid’s main “commercial” competition is not another single molecule but a set of branded-to-generic swaps across Gram-positive categories. Typical classes that compete for formulary and payer share include:

- MRSA agents (including other anti-Gram-positive antibiotics used depending on resistance and site of infection)

- VRE-active options used in stewardship-controlled scenarios

- Newer agents that can shift protocol behavior if they offer safety or efficacy advantages in specific indications

Bottom line: once generics arrive, the market dynamic becomes price-led within therapeutic class constraints, not purely efficacy-led competition.

What are the key market dynamics shaping pricing and volume?

1) Generic substitution and pricing elasticity

Once multiple generic suppliers enter, linezolid’s realized price tends to compress quickly. Price elasticity is high because:

- Clinicians often view linezolid as a “class interchangeable” option once susceptibility and route match.

- Hospitals and payers can standardize on lowest total acquisition cost (including dose-form and supply availability).

The practical result is a revenue profile dominated by:

- Volume stability (persistent hospital use)

- Margin compression (rapid generic price convergence)

2) Route mix: IV vs oral

Linezolid has both IV and oral formulations. Generic entry often expands both, but:

- IV use remains concentrated in acute settings and for patients without oral intake.

- Oral switching supports ongoing use during step-down care.

Shifts in IV-to-oral mix influence:

- Inventory and pharmacy handling costs

- Payer authorization friction (varies by system)

3) Stewardship and safety monitoring constraints

Linezolid has known safety tradeoffs that influence formulary controls, such as hematologic effects with prolonged courses and serotonin-related interaction management. These clinical constraints create a “rationed usage” pattern in some institutions, which:

- Limits runaway volume growth even when resistance patterns support use

- Sustains stable demand because the drug retains a clear niche

4) Treatment-setting growth and infection epidemiology

Long-term infection control, hospital case mix, and antibiotic resistance trends determine baseline demand:

- Resistant Gram-positive prevalence supports linezolid’s role.

- Improvements in infection prevention reduce overall antibiotic pressure and can reduce absolute volumes, even if resistance rates persist.

How has financial trajectory typically behaved for linezolid post-patent?

What does the revenue curve look like after generic entry?

A linezolid financial trajectory in major markets typically follows a three-stage pattern:

- Brand peak phase: high pricing power and formulary adoption

- Initial generic entry phase: steep price erosion with partial volume retention

- Mature generic phase: pricing plateaus at low levels, with revenue driven by sustained hospital utilization and tender dynamics

Why the third stage still produces revenue: linezolid remains a go-to option for certain resistant infections and site-specific indications. Generics keep therapy accessible, so utilization does not disappear.

Margin and profitability

In mature generic markets:

- Gross margins compress due to price competition.

- Net profitability depends on manufacturing scale, procurement contracts, and supply continuity.

- Manufacturers with stronger logistics and lower unit costs generally maintain better earnings profiles even as revenue declines in absolute terms.

Portfolio behavior

For companies holding linezolid manufacturing rights or distribution footprints, the business tends to shift from “brand-like margins” to “operations and procurement leverage.” Revenue depends on:

- Tender wins at hospital system level

- Contract pricing for IV and oral presentations

- Product availability across packaging formats and strength ranges

What is the likely regional pattern of revenue dynamics?

United States

In the US, linezolid revenue is strongly shaped by:

- ANDA-driven generic competition across strengths and dosage forms

- Hospital procurement and group purchasing organization (GPO) contracting cycles

- Formulary management and stewardship protocols

Financial implication: US revenue tends to show persistent volume with lower price per course after major generic penetration.

European markets

In Europe, dynamics are shaped by:

- National reimbursement rules and tender frameworks

- Competitive generic uptake often occurring in waves

- Variation in contract cycles and substitution rules across countries

Financial implication: European revenue often tracks country-by-country tender and payer switching schedules, producing uneven quarter-to-quarter trajectories.

Emerging markets

In emerging markets:

- Uptake can be slower due to procurement constraints and reimbursement heterogeneity

- Price competition accelerates as supply becomes established

Financial implication: emerging market revenues are often more volatile and sensitive to supply continuity and local tender outcomes.

How do linezolid-specific policy and payer factors affect realized sales?

Reimbursement controls and formulary gates

Payers and hospital committees often manage access through:

- Prior authorization in certain settings

- Restrictions on prolonged therapy durations

- Stepping logic that promotes oral switch when clinically appropriate

These controls reduce utilization variability but can cap upside, meaning:

- Growth relies on infection burden and resistance ecology more than on unrestrained prescribing.

Switching incentives

When generics are available, switching incentives rise:

- Pharmacy and procurement policies favor lower-cost equivalents.

- Standardization across therapeutic classes reduces clinician-to-product variation.

Net effect: the market becomes more price-driven and contract-driven.

What are the principal business risks to linezolid’s future financial performance?

1) Additional protocol displacement

If competing agents gain formulary share for specific infections (MRSA and VRE in particular), linezolid’s utilization can decline even if resistance remains.

2) Further generic price erosion

As more suppliers enter and procurement volume concentrates among large players, linezolid’s price can fall faster than volume rises.

3) Supply chain or quality events

In mature generic markets, unit margins can be thin, so supply disruptions can sharply affect quarterly sales even when demand exists.

4) Safety-driven stewardship tightening

If stewardship policies become more restrictive due to safety-monitoring burden, course length and usage frequency can drop.

What would investors and R&D leaders watch to map the trajectory?

Leading indicators

- Tender outcomes at major hospital systems

- Number of generic manufacturers and relative market share by dosage form

- Price per unit and course-level cost trends

- Hospital formulary changes for cSSSI and HAP/VAP settings

- Mix shifts between IV and oral

Lagging indicators

- Reported net revenue changes that reflect full contract cycles

- Changes in volume units and average selling price

- Profitability shifts due to manufacturing and logistics scale

Key Takeaways

- Linezolid’s market is transitioning from exclusivity-led pricing to a generic-driven, contract and tender-led environment with stable hospital demand but structurally lower margins.

- Financial trajectory remains volume-supported due to durable clinical niche in resistant Gram-positive infections, while realized revenue per unit compresses as generic competition matures.

- The main determinants of near-to-mid-term performance are tender/contract dynamics, route mix (IV-to-oral), stewardship controls, and protocol displacement by competing Gram-positive agents.

FAQs

1) Does linezolid still have growth potential in a generic market?

Yes, but it is typically driven by infection burden and hospital utilization rather than price increases. Upside is constrained by stewardship and protocol guidance.

2) What matters more to financial performance: price or volume?

In mature generic markets, price dominates. Volume tends to stay more stable due to clinical niche, while average selling prices decline with competitive entry.

3) How do safety monitoring requirements affect demand?

They can limit prolonged or broad use, which caps uncontrolled growth but also supports continued access within defined stewardship pathways.

4) Is IV or oral more important commercially?

Both matter, but IV-to-oral mix shifts influence revenue and procurement economics. Hospitals often manage step-down therapy to reduce costs and length of stay.

5) What could most quickly change the revenue trajectory?

A combination of new formulary displacement for relevant resistant pathogens and sudden competitive price pressure from additional generic entrants can accelerate revenue erosion.

References (APA)

[1] FDA. (n.d.). Drugs@FDA: Linezolid. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/

[2] EMA. (n.d.). Linezolid (Zyvox and generics): product information and assessment. European Medicines Agency. https://www.ema.europa.eu/

[3] National Center for Biotechnology Information (NCBI). (n.d.). Linezolid: clinical and pharmacology references. PubMed Central. https://www.ncbi.nlm.nih.gov/pmc/