Last updated: April 25, 2026

KLOR-CON (potassium chloride, oral) is an established, commodity-style electrolyte therapy with pricing and demand driven by (1) underlying potassium chloride consumption patterns, (2) payer contract dynamics and pharmacy channel mix, and (3) competitive substitution across oral potassium chloride formats and strengths. Financial trajectory is dominated by volume stability and price compression typical of off-patent generics, with upside tied to brand-retention efforts, formulary placement, and mix shift toward higher-acquisition-cost presentations.

What is KLOR-CON and how does that shape market behavior?

KLOR-CON is an oral potassium chloride product used to prevent or treat hypokalemia and to support potassium replacement in patients at risk (e.g., patients on diuretics). As a potassium chloride replacement, the therapy’s market mechanics differ from patent-protected specialty drugs:

- Therapeutic category: electrolyte replacement (maintenance-like use across chronic and episodic patient populations).

- Primary demand driver: clinical need for potassium repletion, which is comparatively insensitive to innovation cycles.

- Commercial implication: once branded formulations face generic and AB-rated substitution, sales performance tends to track distribution reach and contract pricing more than differentiation.

Because potassium chloride is widely manufactured and available in multiple oral dosage forms, KLOR-CON’s market is characterized by channel substitution and price competition rather than controlled pricing.

How competitive is the KLOR-CON landscape and what does it do to pricing?

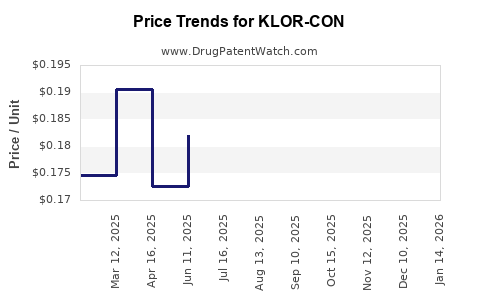

Oral potassium chloride is a classic substitution market: multiple manufacturers sell AB-rated equivalents or competing branded formats, often with different release profiles (immediate vs extended-release). For a branded product in this space, the pricing trajectory typically follows these patterns:

Competitive forces

- Generic erosion: branded sales decline when payers and pharmacies switch to lower-cost equivalents under A/B substitution rules.

- Formulary controls: managed care policies prioritize cost-effective potassium chloride products, using step edits and formulary tier placement to steer prescribing.

- Channel contracting: pharmacy benefit managers and large distributors negotiate rebates and contract pricing that pressure net price.

Pricing outcome

- Gross-to-net compression: rebates and discounts increase as competition intensifies.

- Net revenue sensitivity to mix: shifts in market share among strengths (e.g., different mEq dosing) and release profiles change weighted average selling prices even when unit pricing is falling.

What market dynamics are most likely to govern KLOR-CON demand?

1) Patient cohort stability

Potassium supplementation correlates with rates of:

- diuretic prescribing,

- chronic kidney disease management,

- gastrointestinal losses,

- heart failure and hypertension medication regimens where electrolyte monitoring occurs.

This creates a base level of demand that is less volatile than oncology or specialty launches.

2) Prescriber and patient behavior

For oral electrolytes, prescribing inertia matters:

- prescribers may stay with an established brand if it fits dosing habits,

- patients may continue if tolerated and convenient.

But the override power of payers and pharmacy substitution remains strong in off-patent categories.

3) Supply chain and distribution channel depth

Sales resilience in commodity-like therapeutics often tracks:

- broad distributor coverage,

- contract coverage with major PBMs,

- availability across dose strengths and packaging.

What is the financial trajectory pattern for KLOR-CON in an off-patent electrolyte market?

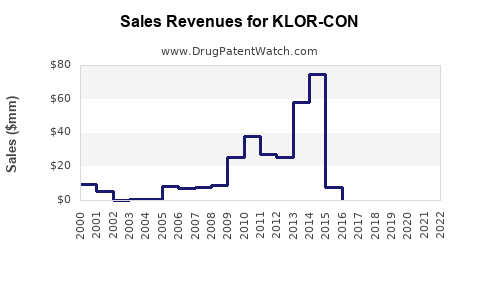

KLOR-CON’s financial trajectory follows the standard off-patent pharmaceutical pattern: volume stability with net price pressure, and sales that increasingly depend on contract wins and share retention rather than innovation-led premium pricing.

Trajectory drivers

- Share retention vs share loss: brand sales hold when formulary placement and rebate structures keep it in preferred tiers.

- Net price decline as competition expands: generic penetration tends to compress net price faster than volume declines initially.

- Mix effects: higher mEq strengths, specific release formats, and package sizes can partially offset unit price erosion.

Financial outcome profile (typical)

- Early phase post-erosion: sales fall more slowly than net price because channel demand is anchored to clinical need.

- Later phase: both share and price decline, driven by stronger payer steering and pharmacy-level substitution.

- Ceiling effects: once brand share drops below formulary “default” status, recovery is difficult without major commercial actions.

How do payers and contracts likely influence KLOR-CON revenue stability?

For off-patent, high-substitutability products, payer policy drives the majority of net revenue variance:

- Formulary status: preferred vs non-preferred tiers materially affect patient access and pharmacy dispensing.

- Utilization management: step edits and prior authorization are less common for electrolytes than specialty drugs, but tier placement and rebate-driven economics can function as indirect UM.

- Pharmacy benefit design: copay levels and brand vs generic benefit design affect switching speed.

In practice, net revenue is governed less by list price and more by contract positioning, rebates, and dispense mix.

What role do product variants (strengths and release profile) play in market outcomes?

KLOR-CON performance can hinge on the availability and demand of specific variants:

- Strength mix: different mEq dosing changes revenue per prescription even if total prescriptions remain stable.

- Release profile: extended-release versions often see different prescriber preferences and may hold share better than immediate-release in certain patient segments.

- Package and dosing convenience: once a formulation aligns with patient routines, substitution can slow even under cost pressure.

These levers do not stop generic erosion, but they influence the speed and depth of net revenue declines.

What external factors can shift KLOR-CON sales and margins?

Regulatory and labeling environment

- Changes to potassium dosing guidance, safety communications, or product labeling can alter prescribing patterns and monitoring frequency.

Drug safety and substitution risk

- Electrolyte products can be sensitive to administration errors and absorption differences; this can affect prescriber trust and dispensing behavior if competing products are perceived as less consistent.

Macro demand shocks

- Increased hospitalization for diuretic-related complications or shifts in chronic disease management can alter electrolyte replacement needs seasonally and cyclically.

What does the KLOR-CON market imply for near-term business planning?

For planning purposes, the market suggests a conservative financial stance:

- Base-case sales depend on contract retention and channel availability, not on growth initiatives.

- Net revenue is the primary risk line due to expected continued price pressure from generics and competitor brands.

- Margin management matters because gross-to-net compression is a structural feature of this category under ongoing competition.

A product in this category typically does not generate upside through clinical differentiation. Commercial upside comes from keeping a preferred placement and maintaining the dispensing mix.

Key Takeaways

- KLOR-CON sits in an off-patent, high-substitutability electrolyte market where demand tracks clinical need and dispensing behavior.

- Financial trajectory is shaped by generic substitution, formulary tier dynamics, and contract-driven net price compression rather than innovation-led premium pricing.

- Revenue stability depends on brand share retention, rebate/contract positioning, and mix across potassium chloride strengths and release profiles.

- The principal financial risk is net price erosion; volume declines tend to follow later when payer steering and pharmacy substitution intensify.

FAQs

-

Is KLOR-CON likely to face ongoing generic price erosion?

Yes. Oral potassium chloride is broadly available and substitution is strong, making net price vulnerable to contract and generic competition.

-

What most influences KLOR-CON net revenue in PBM environments?

Formulary placement, rebate terms, and brand vs generic benefit design that determines dispensing mix.

-

Does patient cohort stability offset price declines for KLOR-CON?

It can slow revenue decline because clinical need persists, but it does not prevent margin compression from net price reductions.

-

Which product attributes can help KLOR-CON hold share?

Strength mix, release profile, and dosing convenience that align with prescriber habits and pharmacy routines.

-

What is the most important forecasting variable for KLOR-CON?

Net selling price and contract economics (gross-to-net), with volume as a secondary variable that may worsen after market share erodes.

References

[1] FDA. KLOR-CON (potassium chloride) prescribing information. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/