GLUCAGON Drug Patent Profile

✉ Email this page to a colleague

When do Glucagon patents expire, and when can generic versions of Glucagon launch?

Glucagon is a drug marketed by Amphastar Pharms Inc, Cipla, Lilly, Lupin, Mylan Labs Ltd, and Fresenius Kabi Usa. and is included in seven NDAs.

The generic ingredient in GLUCAGON is glucagon hydrochloride. There are twelve drug master file entries for this compound. Two suppliers are listed for this compound. Additional details are available on the glucagon hydrochloride profile page.

AI Deep Research

Questions you can ask:

- What is the 5 year forecast for GLUCAGON?

- What are the global sales for GLUCAGON?

- What is Average Wholesale Price for GLUCAGON?

Summary for GLUCAGON

| US Patents: | 0 |

| Applicants: | 6 |

| NDAs: | 7 |

| Finished Product Suppliers / Packagers: | 8 |

| Raw Ingredient (Bulk) Api Vendors: | 1 |

| Clinical Trials: | 946 |

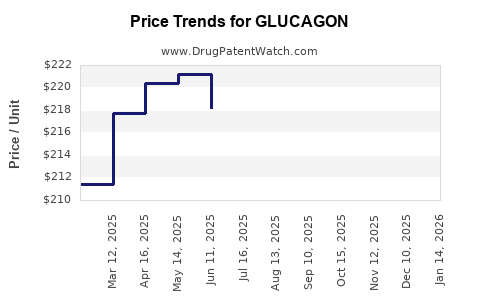

| Drug Prices: | Drug price information for GLUCAGON |

| What excipients (inactive ingredients) are in GLUCAGON? | GLUCAGON excipients list |

| DailyMed Link: | GLUCAGON at DailyMed |

Recent Clinical Trials for GLUCAGON

Identify potential brand extensions & 505(b)(2) entrants

| Sponsor | Phase |

|---|---|

| Rutgers, The State University of New Jersey | PHASE1 |

| The Metis Foundation | PHASE3 |

| University of Colorado, Denver | PHASE3 |

Pharmacology for GLUCAGON

Medical Subject Heading (MeSH) Categories for GLUCAGON

Anatomical Therapeutic Chemical (ATC) Classes for GLUCAGON

US Patents and Regulatory Information for GLUCAGON

GLUCAGON is protected by zero US patents and one FDA Regulatory Exclusivity.

| Applicant | Tradename | Generic Name | Dosage | NDA | Approval Date | TE | Type | RLD | RS | Patent No. | Patent Expiration | Product | Substance | Delist Req. | Exclusivity Expiration |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Amphastar Pharms Inc | GLUCAGON | glucagon | INJECTABLE;INJECTION | 208086-001 | Dec 28, 2020 | AP | RX | No | Yes | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Mylan Labs Ltd | GLUCAGON | glucagon | INJECTABLE;INJECTION | 204468-001 | Dec 12, 2024 | AP | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Lilly | GLUCAGON | glucagon | INJECTABLE;INJECTION | 020928-001 | Sep 11, 1998 | DISCN | Yes | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | ||||

| Fresenius Kabi Usa | GLUCAGON | glucagon hydrochloride | POWDER;INTRAMUSCULAR, INTRAVENOUS | 201849-001 | May 8, 2015 | RX | Yes | Yes | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | ||||

| Cipla | GLUCAGON | glucagon | INJECTABLE;INJECTION | 218813-001 | Sep 15, 2025 | AP | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Lilly | GLUCAGON | glucagon hydrochloride | INJECTABLE;INJECTION | 012122-001 | Approved Prior to Jan 1, 1982 | DISCN | Yes | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | ||||

| Lupin | GLUCAGON | glucagon | INJECTABLE;INJECTION | 214457-001 | Jul 22, 2025 | AP | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| >Applicant | >Tradename | >Generic Name | >Dosage | >NDA | >Approval Date | >TE | >Type | >RLD | >RS | >Patent No. | >Patent Expiration | >Product | >Substance | >Delist Req. | >Exclusivity Expiration |

EU/EMA Drug Approvals for GLUCAGON

| Company | Drugname | Inn | Product Number / Indication | Status | Generic | Biosimilar | Orphan | Marketing Authorisation | Marketing Refusal |

|---|---|---|---|---|---|---|---|---|---|

| Tetris Pharma B.V | Ogluo | glucagon | EMEA/H/C/005391Ogluo is indicated for the treatment of severe hypoglycaemia in adults, adolescents, and children aged 2 years and over with diabetes mellitus. | Authorised | no | no | no | 2021-02-11 | |

| Eli Lilly Nederland B.V. | Baqsimi | glucagon | EMEA/H/C/003848Baqsimi is indicated for the treatment of severe hypoglycaemia in adults, adolescents, and children aged 4 years and over with diabetes mellitus. | Authorised | no | no | no | 2019-12-16 | |

| >Company | >Drugname | >Inn | >Product Number / Indication | >Status | >Generic | >Biosimilar | >Orphan | >Marketing Authorisation | >Marketing Refusal |

Market Dynamics and Financial Trajectory for Glucagon

More… ↓