Last updated: April 25, 2026

FLAGYL (metronidazole) market dynamics and financial trajectory

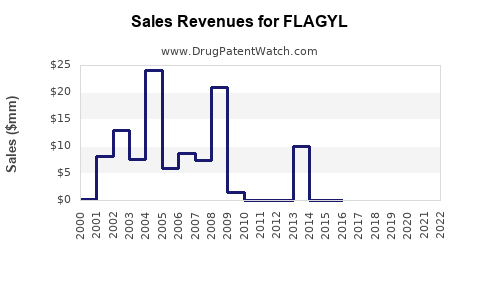

FLAGYL is metronidazole, an established antibacterial and antiprotozoal on the market for decades. Its market dynamics are dominated by long-run generic competition, distribution strength, and category mix (gastrointestinal, gynecologic, dental, and anaerobic infections). Financial trajectory is largely defined by generic price compression, periodic lifecycle moves (new formulations, route changes, and line extensions), and regional tender dynamics rather than innovative pipeline upswings.

What drives FLAGYL demand across indications?

FLAGYL is used in multiple clinical categories that behave differently in procurement and prescribing.

1) Indication mix and prescribing stability

Demand is anchored in indications with stable clinical use:

- Anaerobic bacterial infections and intra-abdominal infections (hospital and acute-care demand)

- Gynecologic infections (including bacterial vaginosis and related anaerobic etiologies)

- Dental indications and perioperative anaerobic coverage (often tied to prescribing habits and local protocols)

- Antiprotozoal uses (historically consistent demand; today more selective depending on local guidelines)

This mix supports steady baseline consumption. Volumes do not behave like specialty oncology products; they behave more like chronic, guideline-driven anti-infectives.

2) Formulation and route

FLAGYL’s market footprint is shaped by availability across routes:

- Oral formulations (tablet/capsule and generic equivalents dominate volume)

- Intravenous (IV) for hospital inpatient settings

- Vaginal formulations (important for gynecologic use in many markets)

Where hospitals require IV access and tender contracts, purchasing tends to concentrate among suppliers that can meet supply continuity and pricing targets.

3) Guideline persistence and resistance patterns

Metronidazole resistance in anaerobes is not absent but has not eliminated routine use. In practice, treatment protocols still rely on metronidazole for anaerobic coverage and targeted protozoal therapy, sustaining recurring prescribing even as competitors expand generics.

How do generics reshape FLAGYL pricing and revenue growth?

FLAGYL’s revenue potential has been capped by patent expiry and widespread generic availability. In this context, the market behaves like a commodity in many geographies.

Pricing dynamics

Generic entry typically drives:

- Unit price compression after first meaningful generic launches

- Buyer switching to lowest net cost during tender windows

- Ongoing erosion of branded net price where reimbursement is substitutable

Branded FLAGYL can retain relative value only where:

- Switching is limited by formulary status

- Patients are maintained on a specific product due to tolerability and switching inertia

- Hospitals face operational constraints (inventory planning, procurement contracts, and IV supply reliability)

Margin structure

For branded or legacy branded products, margins usually depend on:

- Brand premium retention in certain channels

- Mix shift toward formulations less fully penetrated by the lowest-cost suppliers

- Contract pricing dynamics with wholesalers and hospital groups

As generic penetration increases, financial performance tends to track volume more than pricing.

What is the category competition landscape?

FLAGYL competes on two levels: within the metronidazole molecule and across anaerobic infection alternatives.

1) Within-molecule competition (metronidazole generics)

- Competitors are primarily generic manufacturers.

- Switching is often governed by procurement cost and supply assurances.

2) Cross-class alternatives

In anaerobic infections, clinicians can use other agents depending on site of infection and local guidelines, including:

- Beta-lactam/beta-lactamase inhibitor combinations

- Carbapenems for severe cases

- Clindamycin or other anaerobe-active agents where appropriate

- Other nitroimidazoles in some settings

In practice, metronidazole remains a default option in many protocols, but substitution occurs when hospitals pursue formulary cost optimization.

How does supply and manufacturing footprint affect market stability?

Antiinfectives can experience supply disruptions due to API availability and manufacturing capacity constraints. For an established product, the main risk is not demand collapse, but supply continuity and contract execution.

Market outcomes typically show:

- Short-term price spikes and allocation during shortages

- Long-term normalization once manufacturing ramps and contracts refresh

- Channel rebalancing between wholesalers and direct hospital procurement

These dynamics usually do not change the long-run trajectory but can cause quarter-to-quarter swings.

What is FLAGYL’s financial trajectory versus the life-cycle of legacy branded drugs?

1) Typical pattern for legacy branded metronidazole

Given generic competition, the financial trajectory usually follows a mature-drug path:

- High branded sales early in lifecycle

- Gradual decline as generics capture share

- Stabilization at lower net revenue levels where brand persists in some channels

- Periodic sales movement driven by tender cycles and formulation mix

This pattern is consistent with most long-established small-molecule anti-infectives once patent protection lapses.

2) Channel and geography explain “flat vs declining”

Legacy drug revenue does not always fall smoothly. Instead:

- Certain countries can maintain higher branded penetration due to procurement and reimbursement constraints

- Hospital systems may lock into specific suppliers per contract cycle

- Wholesaler inventory turns and seasonal infection patterns can create temporary volume variations

Where does branded FLAGYL still command relative advantage?

Branded advantage in a generic market typically comes from operational and contractual factors rather than clinical differentiation.

Key levers:

- IV supply reliability during hospital tender periods

- Formulation availability where generic coverage is incomplete or less consistent

- Brand position in formularies and historical prescribing patterns

- Distribution agreements that keep branded stock readily available

In most mature markets, brand pricing is constrained to preserve access; branded products typically avoid pricing levels that accelerate substitution.

What would investors or R&D stakeholders look for in the next 3-5 years?

A realistic forward view for a mature metronidazole franchise focuses on risk management and incremental lifecycle actions.

1) Demand stability signals

Track:

- Maintainable tender volumes for IV and oral categories

- Stable guideline adherence for key indications

- Persistent use in gynecologic and anaerobic infection protocols

2) Competitive pressure signals

Track:

- Generic price erosion rates in core markets

- Shifts in formulary status (where net price favors specific suppliers)

- Any cross-class substitution trends (protocol updates)

3) Product lifecycle signals

Track:

- Introduction or strengthening of formulations that can support differentiated access

- Supply expansions that reduce allocation risk

- Contract wins with large hospital groups

Market dynamics by region: how procurement tends to shape outcomes

Regional behavior commonly falls into procurement archetypes:

1) Tender-driven markets

- Brand share erodes faster as procurement normalizes around lowest net cost

- Revenue becomes more sensitive to contract awards and procurement cycles

2) Reimbursement and formulary markets

- Branded products can maintain share longer if formularies restrict interchange

- Net revenue depends on reimbursement rules and prescribing inertia

3) Mixed markets

- Branded products decline but stabilize where institutional purchasing favors continuity

- Generic competition still compresses margins over time

FLAGYL’s financial trajectory in such markets usually reflects which archetype dominates.

Key implications for commercial planning

1) Forecasting approach

Forecasts should be built around:

- Indication-driven volume stability

- Tender-cycle effects for hospital segments

- Contract pricing adjustments and generic price indices

2) Competitive strategy

For any continued branded presence, the strategy is typically:

- Defend access in institutional channels

- Use supply reliability as the main differentiator

- Avoid pricing actions that trigger faster substitution

3) R&D strategy

R&D priorities for a mature molecule tend to focus on:

- Formulation optimization and route improvements

- Extending usability in hospital workflows

- Post-approval lifecycle value through manufacturing scale and stability improvements

Key Takeaways

- FLAGYL market dynamics are driven by stable, guideline-based anti-infective demand across anaerobic and gynecologic categories.

- Generic competition governs pricing and constrains branded revenue; financial trajectory follows a mature-drug decline pattern with tender-cycle and mix effects.

- Branded value is sustained mainly through formulary access, procurement contracts, and supply reliability, not clinical differentiation.

- Near-term financial performance is most sensitive to tender outcomes, generic price compression rates, and channel mix between oral and IV usage.

FAQs

1) Is FLAGYL’s market driven by innovation or by procurement cycles?

Procurement cycles and generic pricing dominate because the product is mature and widely substituted. Contract and tender timing are primary drivers of quarter-to-quarter changes.

2) What formulation segment tends to be most critical for revenue stability?

IV and hospital-facing channels tend to matter most for stability because institutional contracts reduce day-to-day switching, even under generic pressure.

3) Does metronidazole face high substitution risk from other drug classes?

Substitution exists in anaerobic infection treatment, but metronidazole remains protocol-relevant in many guidelines. Risk is mainly formulary and cost driven.

4) Why do branded products sometimes stabilize after years of decline?

Stabilization typically results from lingering formulary status, limited interchange policies in certain settings, and supplier continuity requirements in institutional procurement.

5) What commercial metrics best track FLAGYL’s trajectory?

Net price (after rebates and contract terms), tender award share, generic unit price indices, and channel mix between oral and IV supply.

References

[1] FDA. “Metronidazole (Flagyl).” US Food and Drug Administration (Drug Labeling). https://www.accessdata.fda.gov/ (accessed 2026-04-25).

[2] DailyMed. “FLAGYL (metronidazole) tablet/capsule/other formulations.” US National Library of Medicine. https://dailymed.nlm.nih.gov/ (accessed 2026-04-25).

[3] WHO. “Guidelines and evidence for antimicrobial use in anaerobic infections and related indications.” World Health Organization publications and antimicrobial guidance. https://www.who.int/ (accessed 2026-04-25).