Share This Page

EDEX Drug Patent Profile

✉ Email this page to a colleague

When do Edex patents expire, and what generic alternatives are available?

Edex is a drug marketed by Endo Operations and is included in one NDA.

The generic ingredient in EDEX is alprostadil. There are seven drug master file entries for this compound. Three suppliers are listed for this compound. Additional details are available on the alprostadil profile page.

DrugPatentWatch® Litigation and Generic Entry Outlook for Edex

A generic version of EDEX was approved as alprostadil by HIKMA on January 20th, 1998.

AI Deep Research

Questions you can ask:

- What is the 5 year forecast for EDEX?

- What are the global sales for EDEX?

- What is Average Wholesale Price for EDEX?

Summary for EDEX

| US Patents: | 0 |

| Applicants: | 1 |

| NDAs: | 1 |

| Finished Product Suppliers / Packagers: | 1 |

| Raw Ingredient (Bulk) Api Vendors: | 85 |

| Patent Applications: | 3,992 |

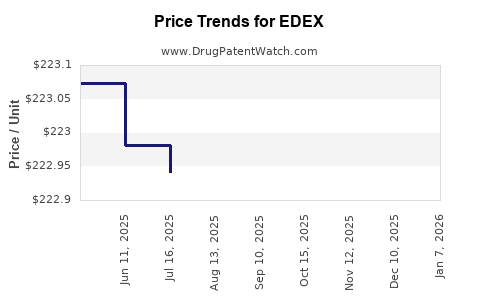

| Drug Prices: | Drug price information for EDEX |

| What excipients (inactive ingredients) are in EDEX? | EDEX excipients list |

| DailyMed Link: | EDEX at DailyMed |

Pharmacology for EDEX

| Drug Class | Prostaglandin Analog Prostaglandin E1 Agonist |

| Mechanism of Action | Prostaglandin Receptor Agonists |

| Physiological Effect | Genitourinary Arterial Vasodilation Venous Vasodilation |

US Patents and Regulatory Information for EDEX

| Applicant | Tradename | Generic Name | Dosage | NDA | Approval Date | TE | Type | RLD | RS | Patent No. | Patent Expiration | Product | Substance | Delist Req. | Exclusivity Expiration |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Endo Operations | EDEX | alprostadil | INJECTABLE;INJECTION | 020649-001 | Jun 12, 1997 | DISCN | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | ||||

| Endo Operations | EDEX | alprostadil | INJECTABLE;INJECTION | 020649-007 | Jul 30, 1998 | RX | Yes | Yes | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | ||||

| Endo Operations | EDEX | alprostadil | INJECTABLE;INJECTION | 020649-003 | Jun 12, 1997 | AP | RX | Yes | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Endo Operations | EDEX | alprostadil | INJECTABLE;INJECTION | 020649-002 | Jun 12, 1997 | AP | RX | Yes | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Endo Operations | EDEX | alprostadil | INJECTABLE;INJECTION | 020649-005 | Jul 30, 1998 | RX | Yes | Yes | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | ||||

| Endo Operations | EDEX | alprostadil | INJECTABLE;INJECTION | 020649-004 | Jun 12, 1997 | AP | RX | Yes | Yes | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| >Applicant | >Tradename | >Generic Name | >Dosage | >NDA | >Approval Date | >TE | >Type | >RLD | >RS | >Patent No. | >Patent Expiration | >Product | >Substance | >Delist Req. | >Exclusivity Expiration |

EDEX Market Dynamics and Financial Trajectory: Alprostadil Injection, Competition, Patents, and Generic Risk

EDEX is a mature U.S. intracavernosal alprostadil product for erectile dysfunction. Its commercial position is supported by physician familiarity, a proprietary dual-chamber delivery system, and use in patients who cannot take or do not respond adequately to oral PDE5 inhibitors. Its financial trajectory is structurally pressured by long-established competition from Caverject, generic or compounded alprostadil, oral erectile-dysfunction drugs, telehealth prescribing, and limited growth in the overall injectable market.

Standalone EDEX revenue is not publicly disclosed. Endo Pharmaceuticals, the U.S. commercial organization associated with EDEX, reports at the company level and does not separately identify EDEX sales in its public financial disclosures. The product should therefore be analyzed as a mature, niche cash-flow asset rather than as a separately measurable growth franchise.

What is EDEX and how does the drug compete?

EDEX is alprostadil for intracavernosal injection. It is supplied in 10, 20, and 40 microgram strengths and uses a dual-chamber syringe that mixes alprostadil with its diluent immediately before administration. The product is indicated for erectile dysfunction of neurogenic, vasculogenic, psychogenic, or mixed etiology. [1]

| Attribute | EDEX |

|---|---|

| Active ingredient | Alprostadil |

| Drug class | Prostaglandin E1 vasodilator |

| Route | Intracavernosal injection |

| U.S. dosage strengths | 10, 20, and 40 mcg |

| U.S. regulatory status | FDA-approved prescription drug |

| Principal indication | Erectile dysfunction |

| Primary commercial differentiator | Dual-chamber reconstitution and prefilled delivery format |

| Primary competitors | Caverject, Caverject Impulse, compounded alprostadil, compounded bimix and trimix |

| Main therapeutic substitutes | Sildenafil, tadalafil, vardenafil, avanafil, vacuum devices, penile implants |

| Biosimilar exposure | None; EDEX is a chemically synthesized small molecule |

EDEX acts locally and generally produces an erection without sexual stimulation. That mechanism gives it value in patients with severe vascular or neurologic disease, after pelvic surgery, or with inadequate response to oral therapy. Its principal commercial weakness is administration: patients must learn self-injection, tolerate a needle, and manage storage and reconstitution.

How large is the EDEX market?

The addressable erectile-dysfunction market is large, but the injectable segment is narrow. Oral PDE5 inhibitors account for most prescription treatment because of convenience, familiarity, and low-cost generic availability. Intracavernosal therapy is typically used after oral therapy fails, is contraindicated, or is rejected by the patient.

Public companies do not generally disclose EDEX-specific revenue, unit volume, or market share. Available corporate reporting supports a qualitative assessment:

| Market factor | Effect on EDEX |

|---|---|

| Large erectile-dysfunction patient population | Expands the potential treatment pool |

| Generic sildenafil and tadalafil | Reduces escalation into injectable therapy |

| Oral-drug intolerance or treatment failure | Creates demand for EDEX |

| Physician training in injection therapy | Supports prescribing continuity |

| Patient reluctance to inject | Limits conversion and persistence |

| Compounding pharmacies | Creates price competition |

| Telehealth platforms | Expands diagnosis and oral prescribing more than branded injection sales |

| Urology and sexual-medicine clinics | Provide the strongest specialist channel |

| Product shortages or supply disruptions | Can shift demand between EDEX, Caverject, and compounded products |

The commercial market is therefore defensive rather than expansionary. EDEX can retain a high-value niche even while total prescriptions decline, but price increases are constrained by alternative injectable products and compounding.

What is the financial trajectory for EDEX?

EDEX’s standalone financial trajectory is not reported. The product is best modeled as a mature branded prescription asset with declining or flat volume, offset in part by pricing, channel management, and recurring use among established patients.

Revenue drivers

EDEX revenue depends on five variables:

- The number of patients receiving intracavernosal therapy.

- The share of those patients using branded EDEX rather than Caverject or compounded formulations.

- Net price after wholesaler, payer, and pharmacy concessions.

- Refill persistence among existing users.

- Product availability and reimbursement.

The strongest recurring revenue comes from existing patients who have already completed titration and are comfortable with the delivery system. New-patient growth is more difficult because physicians often begin with generic oral therapy.

Revenue pressures

The primary financial pressures are:

- Generic oral PDE5 therapy with very low acquisition cost.

- Compounded alprostadil, bimix, and trimix preparations.

- Competition from Caverject and Caverject Impulse.

- Payer restrictions and prior authorization.

- Patient discontinuation caused by pain, bruising, fear of needles, or inconvenience.

- Limited ability to expand the erectile-dysfunction indication.

- Absence of meaningful exclusivity protection for a product approved decades ago.

Endo’s broader financial history also affects the commercial interpretation. The company underwent significant debt restructuring and Chapter 11 proceedings, which increased pressure to prioritize products with reliable cash generation and manageable manufacturing requirements. EDEX’s value in that setting is more likely to come from incremental cash flow and portfolio continuity than from high growth. [2]

When did EDEX receive FDA approval and when does exclusivity end?

EDEX is a legacy FDA-approved product. The FDA approved EDEX under NDA 020379 in the 1990s. Its regulatory exclusivity has expired, and the product does not have the commercial profile of a recently approved medicine with remaining new-drug or orphan exclusivity. [1,3]

| Regulatory element | EDEX status |

|---|---|

| FDA application | NDA 020379 |

| Approval era | 1990s |

| New chemical entity exclusivity | Expired |

| Orphan-drug exclusivity | Not applicable |

| Pediatric exclusivity | No current commercially relevant protection identified |

| Market exclusivity today | Primarily brand recognition, delivery design, manufacturing capability, and customer retention |

For a mature product such as EDEX, the relevant commercial protection is not regulatory exclusivity. It is the combination of device familiarity, manufacturing know-how, physician preference, payer access, and patient persistence.

What patents protect EDEX?

EDEX’s original composition-of-matter and product-development protections are no longer commercially decisive. Alprostadil is an established small molecule, and the product’s original approval dates place any early drug patents well beyond normal U.S. patent terms.

The remaining protection, if any, would be concentrated in:

- Delivery-system design.

- Dual-chamber cartridge architecture.

- Syringe or needle configuration.

- Packaging and stability.

- Manufacturing processes.

- Specific formulation or reconstitution parameters.

The FDA Orange Book should be used to determine whether any patent is currently listed against NDA 020379. Orange Book-listed patents, if present, would be more relevant to an ANDA applicant than expired historical patents. The commercial impact of any such patent depends on its expiration date, claim scope, pediatric extensions, and whether the claim covers the drug, the container-closure system, or only a specific device configuration. [3]

How strong is the EDEX patent estate?

The EDEX patent estate is likely weak as a barrier to a chemically equivalent alprostadil product. It may be stronger against an exact copy of the dual-chamber delivery configuration if an unexpired device or combination-product patent remains enforceable.

| Protection category | Strategic strength |

|---|---|

| Alprostadil active ingredient | Very weak; established molecule |

| Original formulation claims | Weak if expired |

| Dual-chamber delivery system | Potentially moderate against exact device replication |

| Manufacturing know-how | Moderate operational barrier, not a complete legal barrier |

| Brand and physician familiarity | Moderate commercial barrier |

| Regulatory exclusivity | None of material current value |

| Biosimilar exclusivity | Not applicable |

A competitor could avoid a device patent by using a different presentation, cartridge, syringe, or reconstitution format. That makes formulation and delivery patents less capable of blocking the entire market than composition-of-matter patents.

Are there Paragraph IV challenges against EDEX?

A Paragraph IV challenge would be relevant only if an applicant filed an ANDA asserting that an Orange Book-listed patent for EDEX was invalid, unenforceable, or not infringed. No major, publicly prominent EDEX Paragraph IV litigation is identified in the standard commercial record through the available regulatory and litigation history.

The more likely competitive pathway is a product that avoids an active device claim, a non-AB-rated generic or alternative presentation, or a pharmacy-compounded formulation. The absence of high-profile Paragraph IV litigation does not mean the product lacks competition. It indicates that the commercial contest may be occurring through formulation, device design, compounding, and prescribing channels rather than through a headline patent case.

Which companies compete with EDEX?

Caverject and Caverject Impulse

Caverject is the closest branded competitor because it also delivers intracavernosal alprostadil. Caverject Impulse uses a different delivery presentation intended to simplify administration. Competition between Caverject and EDEX is determined by:

- Device convenience.

- Availability through specialty pharmacies.

- Contracting and reimbursement.

- Patient training.

- Physician familiarity.

- Product reliability.

Neither brand has the growth profile associated with a newly launched specialty drug. The products compete for retention within a shrinking or stagnant injectable segment.

Compounded alprostadil, bimix, and trimix

Compounding pharmacies are a major commercial constraint. Compounded alprostadil may be offered alone, while bimix and trimix combine alprostadil with other vasoactive agents. These preparations can offer lower prices or customized dosing, but they are not equivalent to an FDA-approved branded product in regulatory status, manufacturing controls, or labeling.

The competitive effect is strongest among cash-paying patients and patients whose insurance does not cover branded injectable therapy.

Oral PDE5 inhibitors

Sildenafil, tadalafil, vardenafil, and avanafil remain the primary substitutes. Their low generic prices and oral route keep EDEX in a second-line position for many patients. Tadalafil’s longer duration and daily dosing options also reduce the need for an injectable rescue product in some patients.

What is the FDA and Orange Book status of EDEX?

EDEX remains an FDA-approved prescription product. Its regulatory identity is tied to NDA 020379 and the alprostadil intracavernosal indication. FDA labeling covers dosing, reconstitution, injection technique, contraindications, priapism risk, penile fibrosis, and patient training. [1]

The Orange Book is the controlling source for current patent and therapeutic-equivalence information. It should be reviewed for:

- Active patents listed against NDA 020379.

- Any patent-use codes.

- Approved generic or therapeutically equivalent products.

- Drug-device or presentation-specific entries.

- Patent delisting or expiration updates.

EDEX’s product format may complicate direct substitution. A competing alprostadil product can be clinically similar without being therapeutically equivalent to the exact EDEX presentation. That distinction affects pharmacy substitution, payer policy, and the timing of generic erosion.

What formulation and manufacturing barriers protect EDEX?

The active ingredient is not the principal barrier. The more relevant barriers are technical and operational.

Formulation

EDEX uses a dry alprostadil formulation and a separate diluent that are combined before injection. Stability during storage, reconstitution behavior, dose uniformity, container compatibility, and sterility are central development requirements.

A competitor must show that its formulation remains stable through the labeled shelf life and performs consistently after reconstitution. Injectable products also require tight control of particulate matter, sterility assurance, extractables and leachables, and container-closure integrity.

Manufacturing

Manufacturing barriers include:

- Sterile filling and aseptic processing.

- Specialized cartridge or syringe assembly.

- Device-component sourcing.

- Validated reconstitution performance.

- Low-volume production economics.

- Quality-control testing for a sterile combination product.

These factors can discourage entry even when patent protection is weak. They do not prevent entry by a well-capitalized generic or specialty manufacturer.

What litigation and settlement agreements affect EDEX?

No major active EDEX-specific patent litigation or settlement agreement is a central public market driver in the available record. The risk profile differs from that of a high-revenue medicine with multiple active composition, formulation, and method-of-use patents.

Any future case would likely concern:

- An ANDA applicant’s device or formulation design.

- Orange Book patent validity or infringement.

- Trade dress or trademark issues.

- Manufacturing and supply obligations.

- Product liability involving priapism, fibrosis, or injection technique.

The absence of a major settlement limits the ability to forecast a legally fixed generic-entry date. Market entry would instead depend on FDA approval, patent certification, manufacturing readiness, and payer acceptance.

What generic entry risks exist for EDEX?

EDEX faces three forms of competition:

| Entry type | Risk level | Likely effect |

|---|---|---|

| AB-rated generic with the same presentation | Moderate | Direct substitution and price erosion |

| Alternative FDA-approved alprostadil presentation | Moderate to high | Product switching without exact substitution |

| Compounded alprostadil or trimix | High in cash-pay channels | Price pressure and loss of volume |

The most disruptive scenario would be an FDA-approved product with a presentation that is easy for pharmacies and payers to substitute. A technically different but clinically comparable injectable could still capture share through specialty-pharmacy distribution and lower net pricing.

A gradual erosion scenario is more likely than an immediate collapse. Existing patients may remain loyal to a familiar device, while new patients are directed toward cheaper alternatives.

How does EDEX compare with oral erectile-dysfunction drugs?

| Factor | EDEX | Generic sildenafil or tadalafil |

|---|---|---|

| Administration | Intracavernosal injection | Oral tablet |

| Onset | Often rapid after injection | Depends on product and timing |

| Need for sexual stimulation | Generally not required | Generally required |

| Patient convenience | Low | High |

| Generic price pressure | Moderate to high | Very high |

| Use after PDE5 failure | Common | Not applicable |

| Need for physician training | High | Low |

| Commercial growth | Limited | Larger prescription base |

| Adherence barrier | Injection discomfort and technique | Side effects, timing, contraindications |

EDEX’s value is clinical differentiation, not convenience or cost. That supports a durable niche but limits its ability to expand beyond refractory or specialized patients.

What licensing deals and ownership issues affect EDEX?

EDEX has historically been associated with the Schwarz Pharma and UCB commercial lineage, while Endo has been associated with U.S. commercialization and labeling. Public disclosures do not establish a current standalone EDEX licensing stream or provide product-level royalty economics.

For valuation, the important questions are:

- Whether Endo owns the U.S. rights or licenses them.

- Whether manufacturing is internal or outsourced.

- Whether supply agreements contain minimum-volume or termination provisions.

- Whether international rights are held by different entities.

- Whether device patents and trademarks are owned separately from marketing rights.

Because these terms are not reported at product level, EDEX cannot be valued reliably from royalty income or geographic licensing data alone.

What is the commercial outlook and revenue exposure?

EDEX is likely to remain a small but defensible specialty product. Its near-term commercial outlook is:

- Stable to declining prescription volume.

- Continued pressure from compounded therapy.

- Limited ability to raise price without increasing substitution.

- Persistent demand from patients who fail oral therapy.

- High sensitivity to supply continuity.

- Greater value as a portfolio cash-flow product than as a growth asset.

Endo’s company-level revenue cannot be attributed to EDEX without proprietary prescription or sales data. A financial model should therefore use scenario analysis rather than a single reported revenue estimate.

| Scenario | Volume trend | Price trend | Likely outcome |

|---|---|---|---|

| Base case | Low-single-digit decline | Flat to modest increase | Gradual revenue erosion |

| Downside | Mid-single-digit decline | Net price compression | Material decline from substitution |

| Upside | Stable volume | Improved coverage or supply reliability | Flat to modest growth |

| Disruption case | Sharp temporary decline | Uncertain | Share loss after shortage or channel failure |

Key Takeaways

- EDEX is a mature alprostadil injection product for erectile dysfunction.

- Its main commercial advantage is a familiar dual-chamber delivery system, not active-ingredient exclusivity.

- Standalone revenue, margin, and market share are not publicly disclosed.

- Generic oral PDE5 inhibitors and compounded alprostadil are the primary financial pressures.

- Caverject is the closest branded competitor.

- Biosimilar risk is irrelevant because EDEX is a small-molecule product.

- Original drug exclusivity and early composition patents have expired.

- Any remaining legal protection would likely focus on delivery-system, formulation, or manufacturing claims.

- The strongest generic-entry risk is an alternative FDA-approved alprostadil presentation that obtains favorable payer access.

- EDEX is more likely to generate mature portfolio cash flow than meaningful revenue growth.

FAQs

Is EDEX still available in the United States?

EDEX remains an FDA-approved prescription alprostadil product, subject to commercial supply and distribution conditions. Availability can vary by pharmacy, specialty distributor, and insurance channel.

Is EDEX cheaper than Caverject?

Pricing varies by payer, pharmacy, dose, and contracting arrangement. Neither product should be assumed to be consistently cheaper across all channels. Compounded alprostadil is often the main lower-price alternative.

Can a generic drug substitute automatically for EDEX?

Automatic substitution depends on FDA therapeutic-equivalence status and the exact product presentation. A clinically similar alprostadil product may not be automatically substitutable for EDEX.

Does EDEX have an orphan-drug or biologic exclusivity period?

No. EDEX is a small-molecule alprostadil product, not a biologic, and it does not have commercially relevant orphan-drug exclusivity.

What would most increase the value of EDEX?

The most material value drivers would be sustained product availability, improved payer coverage, reduced patient training friction, stronger specialty-pharmacy distribution, and protection of any proprietary delivery configuration that limits direct substitution.

References

-

Endo Pharmaceuticals Inc. (n.d.). EDEX (alprostadil for injection) prescribing information. U.S. Food and Drug Administration.

-

Endo International plc. (2022). Annual report and Form 10-K. U.S. Securities and Exchange Commission.

-

U.S. Food and Drug Administration. (n.d.). Approved drug products with therapeutic equivalence evaluations: Orange Book. FDA.

More… ↓