Last updated: June 20, 2026

Dakota? Market dynamics and financial trajectory for dapagliflozin (Farxiga): revenue drivers, exclusivity timeline, and generic risk

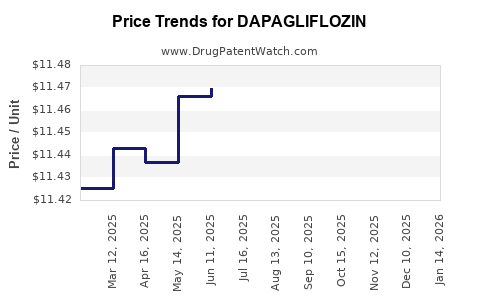

Executive summary: Dapagliflozin (Farxiga; AstraZeneca/BMS via syndication history) has shifted from peak growth into a mature chronic-care revenue engine driven by expanded label areas across type 2 diabetes and heart-kidney indications. Near-term sales durability is supported by (1) ongoing uptitration in diabetes and major adoption in HF and CKD, (2) competitive positioning versus empagliflozin and other SGLT2 inhibitors, and (3) continued treatment persistence. Patent and exclusivity timelines for late-2020s to early-2030s create a structured runway, but the commercial floor is increasingly sensitive to class-level price pressure, payer contracting, and the cadence of new competitors and combination products.

How are dapagliflozin sales performing and what drives Farxiga revenue growth?

Core demand drivers

- Type 2 diabetes (T2D): Dapagliflozin remains a foundation SGLT2 option where payers prefer oral fixed-dose therapy and outcomes evidence supports formulary access.

- Heart failure with reduced and preserved ejection fraction (HFrEF/HFpEF): Sales growth is increasingly indication-led, with cardiology adoption and guideline alignment.

- Chronic kidney disease (CKD): Renal outcomes and reduced disease progression have widened the addressable patient pool.

- Switching from other SGLT2 inhibitors: Uptake often hinges on contracting, patient-specific tolerability, and formulary placement rather than efficacy differences.

Commercial math: what matters in practice

- Persistence and dosing continuity drive realized revenue more than new starts after maturity.

- Payer rebates and PBM contracting increasingly determine net price versus list price.

- Sequential penetration by guideline setting matters: HF and CKD diagnoses are managed in specialized settings where formulary decisions can change faster than in primary care.

Key market dynamic: The SGLT2 class has moved from “category creation” to “class optimization,” compressing spread across competitors. Dapagliflozin’s differentiator is breadth of covered populations and strong payer uptake, not unique mechanism advantage.

What is the competitive landscape for dapagliflozin versus empagliflozin and other SGLT2 inhibitors?

Main class comparators

- Empagliflozin (Jardiance): The closest direct comparator by outcomes data, payer entrenchment, and global reach.

- Canagliflozin (Invokana) and ertugliflozin (Steglatro): Smaller in share, with historical payer presence and regional variability.

- Combination products: These can reshape share where payers prefer fixed-dose regimens and where switching is easier during prescription renewals.

Competitive effects on pricing and share

- Therapeutic class competition typically pushes net pricing down through:

- Formulary switches between SGLT2 agents

- Competitive rebate escalations

- Preferential tiering for one agent per plan with counter-leveraging by manufacturers

- Clinical differentiation becomes secondary as class members show broadly similar glycemic and cardiorenal benefit profiles in outcomes trials.

Where dapagliflozin tends to hold

- HF/CKD prescriber confidence supported by long-term real-world adoption patterns.

- Broad portfolio messaging aligned to diabetes plus cardiorenal risk targeting.

- Supply reliability and manufacturing scale reduce interruption risk.

How does patent and exclusivity timing for dapagliflozin influence generic and biosimilar risk?

Why exclusivity timing matters

- Oral small molecules like dapagliflozin face shorter commercial disruption horizons than complex biologics, but the timing still controls:

- Paragraph IV filing windows

- Settlement leverage

- Launch logistics and stocking behavior

Exclusivity and patent estate framing

- Dapagliflozin’s commercial protection has two layers:

- Regulatory exclusivities (market exclusivity tied to FDA approvals and exclusivity categories)

- Patent coverage (composition of matter, formulations, and method-of-use or dosing patents depending on jurisdiction and claims)

Market impact across phases

- Pre-Paragraph IV: limited competitive pressure; manufacturers can reinvest in indication expansion and contracting.

- Paragraph IV pending: discounting rises as wholesalers anticipate demand share shifts.

- Post-launch: net price typically drops quickly; value shifts to contracting-based share and patient persistence.

When does dapagliflozin lose exclusivity in the US and EU, and what does that mean commercially?

US dynamics

- In practice, for dapagliflozin the commercial schedule is driven by:

- expiration of key listed Orange Book patents, and

- potential exclusivity extensions tied to pediatric and other regulatory events.

EU dynamics

- EU market authorization and patent enforcement affect:

- national injunction strength

- rollout timing of parallel launches by member states

- reliance on SPC (supplementary protection certificates) where applicable

Commercial meaning

- As the expiration window approaches, manufacturers increase:

- payer intensity

- copay support where permitted

- real-world evidence spending to defend persistence

- Generic risk does not move prices uniformly. Net price typically starts compressing before the first generic is dispensed, driven by payer re-contracting.

What patents protect dapagliflozin (composition, method of use, and formulations) and how broad are they?

Patent estate categories that typically matter for SGLT2s

- Composition of matter patents: strongest and longest protection anchor.

- Formulation and dosage form patents: can support “authorized generic” barriers in some scenarios.

- Method-of-use patents: protect specific patient populations, endpoints, or combinations, and can slow generic entry where claims remain infringed.

- Manufacturing process patents: less common as barriers unless materially distinct.

Business interpretation

- Broad method-of-use claims can matter even after composition patents erode, because generic entrants can be forced into design-around strategies or claim carve-outs that limit launch scope.

- Formulation patents can delay “drop-in” substitution if they affect stability, bioavailability, or patient-use instructions.

What is the Orange Book status of dapagliflozin (Farxiga) and how many patents are listed?

Orange Book status as a launch risk indicator

- The number of listed patents and their expiration dates typically predict:

- whether generic entry is likely to be early or staged

- whether Paragraph IV challenges are clustered

- settlement likelihood versus litigation protraction

How to read the estate for commercial planning

- Highest-risk patents are those with:

- earliest expiration after current period

- broad claim scope likely to trigger infringement findings

- active litigation or recent court rulings in the same class

What generic entry risks exist for dapagliflozin and how do Paragraph IV challenges play out?

Generic entry mechanics

- Filings under Paragraph IV usually target:

- composition or method-of-use patents asserted against generics

- Outcomes split into:

- early settlement and “carve-out” launch timing

- prolonged litigation leading to later entry or delayed switching

Market behavior around Paragraph IV

- Payors often pre-negotiate rebate structures as soon as launch risk becomes plausible.

- Manufacturers respond with increased contracting efforts to maintain share and reduce churn.

Practical effect

- Even when legal barriers exist, a credible challenge tends to:

- accelerate formulary reviews

- increase price competition

- shift share in favor of the incumbent only if rebates remain competitive

How does dapagliflozin compare with empagliflozin in financial trajectory and sales durability?

Class-typical comparison

- Dapagliflozin and empagliflozin both sit in the SGLT2 “top tier” globally, but their financial trajectories can differ due to:

- country-level reimbursement generosity

- payer formularies and preferred agent contracting

- mix by indication (diabetes vs HF/CKD)

- penetration in cardiology-led pathways

What to watch in quarterly reporting

- Growth split by:

- net sales trends in diabetes versus HF/CKD-related patient segments

- prescription growth versus price/rebate changes

- Any guidance language changes around:

- payer mix shift

- competitive intensity

- patient persistence and adherence

Which litigation and settlement events affect dapagliflozin’s commercial timeline?

Litigation impact pathways

- Settlement agreements influence:

- earliest possible generic launch date

- scope of product (strengths, dosage forms)

- whether the entrant launches with “at-risk” design or delayed entry

- Court rulings influence:

- enforceability of specific patents

- whether subsequent patents remain relevant for additional entry waves

Class-level pattern

- For late-stage small-molecule franchises, litigation often resolves into staged entry dates rather than immediate wholesale erosion.

What is the FDA regulatory status of dapagliflozin and what does it mean for market expansion?

Regulatory status effects

- Approval label breadth drives:

- adoption across care settings

- reimbursement eligibility

- formulary stability

- Post-approval expansions can extend the lifecycle by adding:

- additional populations

- refined risk strata

- combination approaches with other standard-of-care drugs

Commercial implication

- Even when diabetes growth matures, label expansions in cardiorenal indications can offset:

- lower incremental starts

- higher competitive switching rates

How strong is the patent estate for dapagliflozin versus generic or biosimilar strategies?

Strength profile for a mature small-molecule

- Strength is typically less about “block forever” and more about:

- controlling the timing of entry waves

- limiting the generic label scope through method-of-use constraints

- leveraging formulation/device or manufacturing claims to slow adoption

Strategy for challengers

- Generic entrants prefer:

- high-likelihood patents to attack

- design-around strategies that reduce infringement exposure

- Incumbents prefer:

- settlements that trade litigation for delayed entry

- evidence-based defense of method-of-use claims

What is the financial trajectory for dapagliflozin (net sales, segment relevance, and forward risks)?

Trajectory shape for a franchise-level SGLT2

- Early stage: rapid penetration as outcomes evidence converts guidelines into prescribing habits.

- Mid stage: competitive stabilization as empagliflozin, canagliflozin, and others claim share.

- Late stage: growth becomes lumpy and more dependent on:

- payer dynamics

- indication-mix shifts

- contract renewals

- competitive rebate intensity

Forward risks

- Price compression: driven by SGLT2 class contracting cycles.

- Formulary churn: increases when a plan switches preferred agents.

- Patent and litigation timing: can trigger concentrated entry risk.

- Manufacturing and supply: can create short spikes in reimbursement or stocking distortions.

Forward supports

- Clinical category durability: HF/CKD adoption is less discretionary.

- Persistence and adherence: strong drivers of net realized revenue.

- Label breadth and switching friction: can slow churn versus pure diabetes-only portfolios.

Key market scenarios for the next 3–5 years: baseline, stress, and upside

Baseline

- Continued growth driven by HF/CKD mix and moderate pricing compression.

- Generic threat remains a planning variable, not an immediate share rupture.

Stress

- Increased payer switching within the class.

- Faster-than-expected rebate compression and churn; litigation pressure rises near key expirations.

Upside

- Faster expansion of HF/CKD adoption and improved persistence.

- Better than expected net pricing retention through payer contracting.

Key Takeaways

- Dapagliflozin’s financial trajectory is increasingly governed by cardiorenal indication uptake and persistence rather than diabetes-only growth.

- The SGLT2 category is in a pricing and contracting cycle that compresses net prices even when volume grows.

- Exclusivity and patent estate timing controls the slope of generic entry risk; credible Paragraph IV windows tend to accelerate formulary and rebate actions before launch.

- The incumbent advantage is maintained through contracting, persistence, and label breadth, but share is vulnerable to class-level payer preference shifts.

FAQs

1) What are the biggest net sales drivers for Farxiga beyond new prescriptions?

Persistence, indication mix (HF/CKD), and payer rebate contracting cycles.

2) How does payer formulary placement influence dapagliflozin market share versus competing SGLT2 inhibitors?

Preferred-tier positioning and rebate offers determine switching behavior more than small efficacy differences.

3) What commercial impact do Paragraph IV filings have for dapagliflozin even before a generic launches?

They trigger payer re-contracting and formulary reviews that can reduce net realized pricing and accelerate churn risk.

4) How do method-of-use patent claims affect the scope of potential generic entry for dapagliflozin?

They can constrain the patient populations and indications covered by generic products, slowing market penetration even if composition barriers weaken.

5) What FDA label expansions could extend dapagliflozin revenue durability?

Approvals that widen cardiorenal populations, refine risk strata, or support combination regimens with standard-of-care therapies.

References (APA)

- AstraZeneca. (n.d.). Farxiga (dapagliflozin) prescribing information and label history.

- FDA. (n.d.). Orange Book: Approved Drug Products containing dapagliflozin (Farxiga).

- FDA. (n.d.). Drug Approval Reports for dapagliflozin products.

- Company filings (AstraZeneca and Bristol Myers Squibb). (n.d.). Financial statements and product revenue disclosures for Farxiga.