Last updated: May 25, 2026

Cyanocobalamin (vitamin B12, synthetic cobamides) is a commodity-like, off-patent pharmaceutical ingredient with broad therapeutic use in deficiency states and nutrition products. Financial trajectory is dominated by (1) baseline prevalence of B12 deficiency, (2) payer and reimbursement dynamics for oral vs injectable formats, (3) contract manufacturing scale and ingredient cost/availability, and (4) generic procurement cycles rather than patent exclusivity.

Below is the market structure and financial trajectory by product format and channel, with IP pressure mapped as generic entry risk.

What drives demand for cyanocobalamin (vitamin B12) and how do market dynamics shift by region?

Demand is anchored to B12 deficiency epidemiology and to use across nutraceutical plus prescription-adjacent segments. Market dynamics are less about novel mechanism and more about chronic patient volume, prescribing habits, and procurement in hospitals and pharmacies.

Which indications and patient segments pull cyanocobalamin volumes?

- Nutritional deficiency (dietary insufficiency, malabsorption risk)

- Pernicious anemia (supportive replacement; some patients rely on long-term injections depending on clinician practice)

- Malabsorption states (selected gastrointestinal disorders)

- Elderly populations and diets with limited animal products

- Supportive therapy where clinicians use B12 to address macrocytic anemia workups

- Nutrition and fortification used in broader health products (often marketed as vitamin B12 but manufactured as cyanocobalamin in many supply chains)

How do oral vs injectable formats change channel economics?

- Injectables: Higher unit cost, institutional procurement sensitivity, and product availability constraints can drive price moves.

- Oral (tablets, capsules, sublingual): More price-competitive, better alignment with self-administration, and subject to aggressive generic tendering.

Region-level drivers

- US/EU: Pricing discipline and generic tendering shape net realized prices. Hospital formularies can maintain injectable access even when oral prices fall.

- Emerging markets: Higher sensitivity to ingredient supply and logistics costs. Budget formularies and private-sector import channels often create pricing volatility when supply tightens.

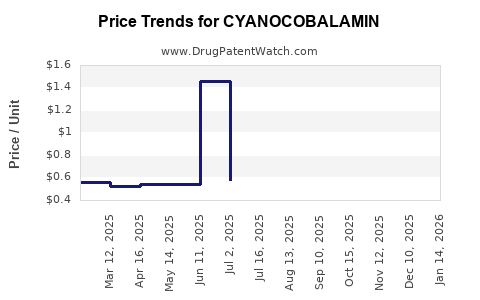

How does cyanocobalamin pricing evolve in the generic era, and what are the typical margin pressures?

Pricing follows generic commodity dynamics. Net margins compress through multiple generic SKUs, substitution, and ingredient-linked cost pass-through.

What creates price volatility?

- Ingredient supply: Cyanocobalamin is produced through cobalt-containing fermentation and purification supply chains. Disruptions at upstream sites affect contract pricing.

- FX and logistics: Import-heavy regions see price swings due to currency and shipping costs.

- Tender cycles: Larger buyers reprice on recurring schedules, driving sharp short-term drops and then stabilization.

How do buyers influence realized prices?

- US payers and PBMs influence oral vs injectable formulary placement.

- Hospital and clinic procurement teams favor lowest acquisition cost consistent with availability.

- Retail channel pricing is shaped by pharmacy-level competition and local generic share.

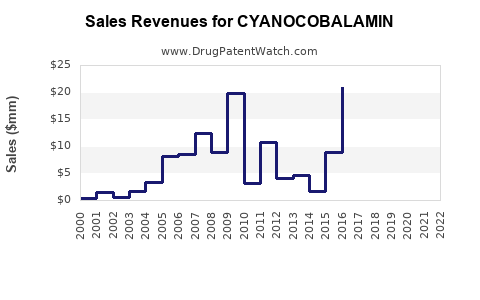

What are the key financial KPIs for cyanocobalamin (volume, revenue, ASP) and how do they typically trend?

Revenue tracks with utilization volume and reimbursement intensity more than with price. In most markets, the long-run ASP trend is down or flat; revenue growth comes from utilization stability and population aging, not from premium pricing.

Expected KPI behavior

- Volume: Stable-to-growth with aging and deficiency prevalence; occasional step-ups when clinical awareness rises or payer coverage expands.

- ASP: Downward bias over time due to generic competition and increased substitution.

- Gross margin: Pressured by:

- ingredient cost movement,

- manufacturing scale efficiencies required to compete,

- rebate and contracting for institutional buyers.

- Working capital: Ingredient stock management matters because commodity supply can change abruptly.

Which product forms win commercially: oral tablets vs injectables vs combination products?

Orals win on convenience and substitution; injectables remain sticky in hospital and specific clinical workflows. Combination products (vitamin mixes) compete on consumer demand and channel merchandising.

Oral cyanocobalamin

- Competitive advantage: patient self-administration, adherence potential, and lower admin cost.

- Commercial pattern: rapid generic share gains, tender pressure, and broad pharmacy availability.

Injectable cyanocobalamin

- Competitive advantage: clinician preference in acute deficiency, malabsorption, and uncertain absorption.

- Commercial pattern: fewer SKUs than oral in many formularies, but still generic-dominated; price depends heavily on procurement and supply continuity.

Combination products

- Competitive advantage: bundling with folate, iron, or multivitamins.

- Commercial pattern: pricing tied to consumer brand strategy when nutraceutical-style; but in prescription-equivalent dosing, competition is still largely generic.

What patents protect cyanocobalamin products and how weak is the IP estate versus vitamin B12 commodity supply?

For cyanocobalamin itself, the active ingredient is long-established; most commercial products are off-patent on the base molecule. As a result, the practical IP moat is typically formulation, device, packaging, and process rather than composition-of-matter.

Where IP can still matter commercially

- Formulation patents for specific release profiles (notably for oral)

- Manufacturing/process patents (yield, impurity profile, crystallization steps)

- Device and administration systems for injectables (autoinjectors, prefilled syringes) when present

- Method-of-use claims tied to dosing regimens, although these are less common for a commodity replacement vitamin

How IP impacts pricing and generics

- In most markets, even when there are minor patents around formulation/process, generics can often work around with bioequivalence-typical strategies or simpler alternatives, limiting long-term pricing power.

When does cyanocobalamin lose exclusivity, and what is the realistic generic launch timeline?

Exclusivity is not a typical driver for cyanocobalamin revenue in the way it is for novel branded drugs. The drug’s financial trajectory is instead shaped by generic replacement that already dominates most markets.

What this means for the “timeline” question

- Branded cyanocobalamin products, if any remain in certain markets, generally face:

- already expired ingredient coverage,

- ongoing competition from multiple labeled generics,

- replacement by therapeutic equivalents (oral vs injectable) depending on payer rules.

What is the Orange Book status of cyanocobalamin products, and how many generics are typically listed?

Orange Book status for cyanocobalamin is usually consistent with an off-patent active ingredient with multiple A-rated generics. Commercial impact comes from the number of listed products, packaging strengths, and whether any device or formulation patent is still active for particular dosage forms.

How to interpret Orange Book listings for cyanocobalamin

- Many entries show:

- broad generic competition across strengths,

- limited remaining exclusivity outside of niche patents,

- substitution driven primarily by price and availability.

What Paragraph IV challenges exist for cyanocobalamin, and do they affect price?

Paragraph IV litigation is generally not a major financial driver for cyanocobalamin because the active ingredient is mature and most claims that would be challenged are already expired or weak in commercial scope.

Price impact logic

- When generic entry happens, it tends to be gradual through contracting and substitution rather than a discrete Paragraph IV shock event.

Are there biosimilar risks for cyanocobalamin?

No. Cyanocobalamin is a small-molecule vitamin replacement and is not a biologic product. Biosimilar frameworks do not apply.

How does cyanocobalamin compare commercially with other B12 forms (hydroxocobalamin, methylcobalamin) in market dynamics?

Cyanocobalamin competes on price and availability; methylcobalamin competes on patient and clinician preference in some segments. Hydroxocobalamin has region-specific footprints depending on historical prescribing patterns.

Commercial comparison

- Cyanocobalamin: typically lower cost and broad generic access

- Methylcobalamin: sometimes marketed for active-form preference; pricing may be higher in retail

- Hydroxocobalamin: can have stronger positioning in certain prescribing markets, affecting injectable preference

Implication for revenue trajectory

If payers push cost minimization, cyanocobalamin usually gains share. If clinical practice shifts toward preferred active forms for certain deficiency profiles, cyanocobalamin growth can be partially offset.

Which companies dominate cyanocobalamin manufacturing and distribution, and what does that mean for supply risk?

Supply structure is characterized by high-capacity manufacturers and multiple labeled generics. Financial dynamics are shaped more by production scale and ingredient procurement than by brand power.

Supply risk pathways

- Upstream fermentation and purification constraints can cause short-term availability issues.

- Contract manufacturing capacity can swing with global demand for vitamins and nutrition supplements.

- Regulatory quality events at manufacturing sites can temporarily restrict supply.

How do reimbursement and procurement rules influence cyanocobalamin revenue more than clinical outcomes?

For commodity vitamins, payer logic is mostly economic. Reimbursement and formulary placement determine utilization indirectly by shifting patients toward the lowest-cost equivalent or the most covered route of administration.

Key levers

- Formulary tiering of oral vs injectable

- Pharmacy benefit design that favors generics

- Institutional preferred product lists for injectables

What regulatory pathways govern cyanocobalamin generics, and how does that affect launch speed?

Generics typically use Abbreviated New Drug Application pathways once the active ingredient and reference product structure are established in FDA submissions for that dosage form.

Launch speed considerations

- Oral solid dose generics can launch quickly when manufacturing and bioequivalence packages are ready.

- Injectable launches depend on:

- container closure system readiness,

- sterility assurance validation,

- fill-finish capacity and supply chain stability.

What generic entry risks exist for a branded cyanocobalamin product still on the market?

For branded legacy cyanocobalamin, the biggest risks are procurement-driven substitution and inventory-based switching, not major patent hold-up.

Risk factors that drive replacement

- Lower-cost oral equivalents gaining formulary position

- Multiple generics already on market reducing switching friction

- Tender announcements that force conversion to lowest-cost SKUs

What litigation affects cyanocobalamin, and does it create lasting barriers to competition?

Litigation is generally not a lasting barrier for commodity vitamins unless a specific formulation/device/process patent remains active and is tied tightly to the commercial product. Even then, workarounds and alternative dosage forms often reduce long-term impact.

Where disputes can still matter

- Patents on:

- specific oral release profiles,

- impurities and manufacturing specs,

- device packaging (prefill format),

- exclusivity tied to newly approved strengths or delivery formats.

How should investors and licensing teams underwrite the financial trajectory for cyanocobalamin?

Underwriting should treat the asset as a volume business with commodity-like price elasticity. Value creation is more likely from operational execution than from IP exclusivity.

Underwriting checklist

- Identify the most profitable dosage forms (oral vs injectable) in target channels

- Map contracting tender cycles and expected ASP drift

- Stress-test upstream ingredient supply disruptions

- Assume patent-driven barriers are limited except for narrow formulation/process patents on specific SKUs

Key Takeaways

- Cyanocobalamin is a mature, off-patent commodity vitamin where long-run revenue is driven by utilization volume and payer procurement economics, not premium pricing.

- Oral formats typically face stronger generic substitution and ASP compression; injectables can be more procurement-concentrated but still generic-dominated.

- IP moats, where present, are usually formulation/process or device-related and tend to be narrow, limiting long-term exclusion value.

- Biosimilar risk is not applicable; generic entry risk is primarily commercial and procurement-driven rather than Paragraph IV shock effects.

- Financial trajectory should be underwritten as a volume-stable, margin-pressured business with supply-chain execution as a key determinant of realized revenue and gross margin.

FAQs

1) Does cyanocobalamin compete mainly on price or on clinical preference versus methylcobalamin?

Mostly on price and formulary coverage; clinical preference can shift share toward methylcobalamin in certain clinician and patient segments.

2) Are cyanocobalamin injectables less prone to price erosion than tablets?

They can be less subject to retail substitution, but institutional procurement and generic tendering still drive downward ASP over time.

3) Can reformulation create a durable revenue bump for cyanocobalamin products?

Only if tied to a distinct dosage form or delivery system that payers adopt; otherwise reformulation tends to attract generic workarounds.

4) What supply-chain events most often move cyanocobalamin pricing?

Upstream ingredient availability and fill-finish capacity constraints, plus regional import/logistics disruptions.

5) How do tender cycles typically affect quarterly revenue for cyanocobalamin?

Revenue and realized pricing can jump or drop around contract award and conversion periods, with stabilization thereafter.

References

- FDA. “Drugs@FDA.” U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/

- FDA. “Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations.” U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/ob/

- FDA. “Abbreviated New Drug Applications (ANDAs).” U.S. Food and Drug Administration. https://www.fda.gov/drugs/abbreviated-new-drug-application-anda