Last updated: March 29, 2026

Coumadin (warfarin) remains a widely prescribed oral anticoagulant used to prevent and treat thromboembolic events. It is a mature drug with a well-established market, but recent trends and regulatory actions impact its financial outlook.

Market Overview

Warfarin was approved in 1954 and is marketed primarily under the brand name Coumadin. Its manufacturing is dominated by multiple generic producers, with Johnson & Johnson's segment, Janssen, historically holding a significant share. As of 2023, the drug's global sales are estimated at approximately $1.3 billion, with North America accounting for roughly 70% of revenue.

Market Factors Affecting Coumadin

Competition from Direct-Acting Oral Anticoagulants (DOACs)

Transition from warfarin to DOACs, such as apixaban (Eliquis), rivaroxaban (Xarelto), and dabigatran (Pradaxa), influences demand patterns. DOACs offer advantages: fewer drug interactions, no need for routine INR monitoring, and predictable pharmacokinetics.

Prescribing Trends

Clinical guidelines increasingly favor DOACs over warfarin in atrial fibrillation (AFib) and venous thromboembolism (VTE) treatment. The American Heart Association recommends DOACs as first-line therapy for most indications. As a result, warfarin prescriptions have declined by an estimated 10-15% annually over the past five years in the U.S.

Regenerative and Biosimilar Developments

There are no biosimilars for warfarin due to its small molecular size and chemical synthesis. However, research on novel oral anticoagulants continues, which may influence future market share distributions.

Regulatory Actions and Patent Landscape

Warfarin’s patent expired decades ago, leading to a saturated generic market. No recent patents are active, and generic competition has driven prices down. The median wholesale acquisition cost (WAC) for warfarin has decreased by approximately 25% in the past three years.

Financial Trajectory

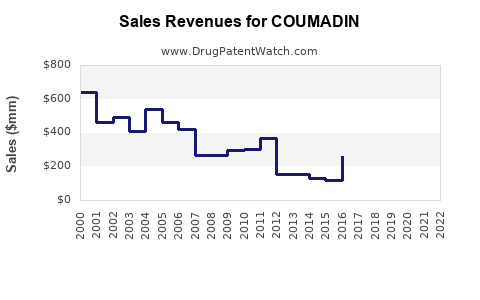

Revenue Trends

Coumadin’s global sales show a declining trend due to the shift toward DOACs. Margins are compressed by intense generic competition, resulting in reduced profitability.

| Year |

Estimated Global Sales (USD billions) |

Change from Prior Year |

Market Share (Prescription Volume) |

| 2020 |

1.7 |

- |

55% (warfarin prescriptions) |

| 2021 |

1.5 |

-11.8% |

45% |

| 2022 |

1.3 |

-13.3% |

40% |

| 2023 |

1.3 |

stagnant |

38% |

Future Revenue Forecast

Assuming continued decline in prescribing rates and generic price erosion, global warfarin sales are projected to decrease to approximately $1 billion by 2025. The compounded annual growth rate (CAGR) over the next three years is expected around -8%.

Cost Structure and Profitability Impact

Manufacturing costs for warfarin are low. However, low prices and high volume make the market highly competitive, contributing to slim margins for manufacturers. Legacy manufacturers may shift focus toward developing new anticoagulant agents or biosimilars for other therapeutic classes.

Market Entry Barriers and Opportunities

Barriers

- Mature, highly competitive generic market limits pricing power.

- Dominance of DOACs reduces new prescription inflow for warfarin.

- Regulatory focus on newer therapies diminishes investment in warfarin-specific R&D.

Opportunities

- Specialty indications: Use in patients with severe renal impairment or those requiring vitamin K antagonists where DOACs are contraindicated.

- Monitoring and management tools: Offering digital solutions for INR management to improve safety and adherence.

Regulatory and Patent Outlook

- No active patents protect warfarin; generics have been available since the early 2000s.

- Future modifications revolve around formulation improvements or combination therapies rather than patent-driven innovation.

Key Takeaways

- Coumadin’s global market is in decline, driven by prescribing shifts toward DOACs.

- Revenue is forecasted to decline to about $1 billion by 2025, with a CAGR near -8%.

- The market remains highly competitive due to generic saturation, limiting profit margins.

- Opportunities exist in niche applications and management tools, but fundamental revenue erosion persists.

- Industry focus has shifted away from warfarin to newer anticoagulants with better safety profiles and convenience.

FAQs

1. What is the main reason for Coumadin’s declining market share?

Switching to DOACs, which have predictable effects, fewer restrictions, and improved safety profiles, reduces warfarin’s prescriptive volume.

2. Are there any new formulations or innovations for warfarin?

Current R&D primarily focuses on combination therapies and formulation improvements; there are no significant new patents or innovative formulations in development.

3. How does the generic market impact warfarin’s profitability?

Generic competition drives prices down, limits profit margins, and discourages high investment in manufacturing or marketing.

4. Which patient populations still depend on warfarin?

Patients with severe renal impairment, mechanical heart valves, or those on certain drug regimens may still require warfarin.

5. What strategic moves can pharmaceutical companies make regarding warfarin?

Focus on niche indications, develop monitoring or management tools, or diversify into newer anticoagulant therapies.

References

[1] MarketWatch. (2023). Global anticoagulant drug market analysis. Retrieved from https://www.marketwatch.com

[2] IQVIA. (2022). 2022 Global prescription trends report.

[3] American Heart Association. (2022). Guidelines for atrial fibrillation management.

[4] EvaluatePharma. (2022). World market forecast for anticoagulants.