Last updated: February 19, 2026

Capecitabine, an oral fluoropyrimidine carbamate, is a prodrug converted to the cytotoxic agent 5-fluorouracil (5-FU) preferentially within tumor cells. This mechanism minimizes systemic toxicity compared to intravenous 5-FU. The drug is approved for the treatment of metastatic breast cancer, metastatic colorectal cancer, and advanced gastric and gastroesophageal junction adenocarcinoma.

What is the current market size and projected growth for capecitabine?

The global capecitabine market was valued at approximately $1.8 billion in 2023. Projections indicate a compound annual growth rate (CAGR) of 3.5% between 2024 and 2030, reaching an estimated $2.3 billion by the end of the forecast period. This growth is driven by the continued incidence of its target cancers, patent expirations leading to generic competition, and the drug's established efficacy in various treatment regimens.

The market is segmented by indication, with metastatic colorectal cancer representing the largest segment, accounting for over 45% of the market share in 2023. Metastatic breast cancer follows, comprising approximately 30% of the market. The gastric and gastroesophageal junction adenocarcinoma segment accounts for the remaining market share.

Geographically, North America and Europe currently dominate the capecitabine market, owing to high cancer prevalence and established healthcare infrastructure. The Asia-Pacific region is anticipated to exhibit the highest CAGR during the forecast period, fueled by increasing cancer diagnoses, expanding access to healthcare, and the growing presence of generic manufacturers.

Table 1: Global Capecitabine Market Segmentation (2023)

| Segment |

Market Share (%) |

| Metastatic Colorectal Cancer |

45.2 |

| Metastatic Breast Cancer |

30.5 |

| Gastric/GEJ Adenocarcinoma |

24.3 |

What are the key drivers and restraints impacting capecitabine's market trajectory?

Drivers:

- Rising Cancer Incidence: The global increase in the incidence of colorectal, breast, and gastric cancers directly fuels demand for effective chemotherapeutic agents like capecitabine. The World Health Organization estimates that colorectal cancer is one of the most common cancers worldwide, with millions of new cases diagnosed annually.

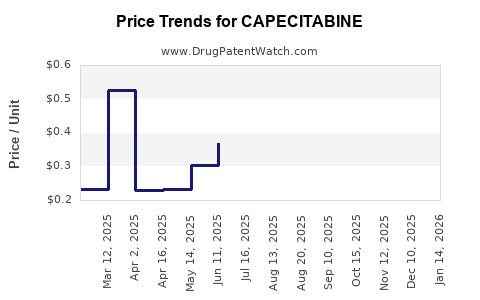

- Generic Competition: The expiry of key patents for innovator capecitabine products has opened the door for numerous generic manufacturers. This has led to significant price erosion, increasing accessibility for patients and healthcare systems, and expanding the overall market volume. For example, the initial patent expiry for Roche's Xeloda (capecitabine) in major markets occurred in the late 2000s and early 2010s, leading to a surge in generic versions.

- Established Efficacy and Safety Profile: Capecitabine is a well-established chemotherapy agent with a favorable safety profile compared to intravenous 5-FU, particularly in terms of patient convenience and reduced hospitalizations. Its efficacy has been demonstrated in numerous clinical trials and real-world studies, solidifying its role in standard treatment guidelines.

- Combination Therapies: Capecitabine is frequently used in combination with other chemotherapeutic agents or targeted therapies, enhancing treatment outcomes. For instance, it is a cornerstone in regimens for advanced colorectal cancer, often combined with oxaliplatin (e.g., CAPOX or XELOX regimen).

Restraints:

- Development of Novel Therapies: Advances in oncology have led to the development of targeted therapies and immunotherapies that offer alternative treatment options for patients with certain cancer types. These newer modalities can potentially reduce the reliance on traditional chemotherapy like capecitabine in specific patient populations.

- Side Effects and Toxicity: While generally better tolerated than intravenous 5-FU, capecitabine can still cause significant side effects, including hand-foot syndrome, diarrhea, and myelosuppression. Management of these toxicities can impact treatment adherence and necessitate dose adjustments or discontinuations.

- Stringent Regulatory Approval Processes: The introduction of new capecitabine formulations or new indications requires rigorous clinical trials and regulatory approval, which can be time-consuming and expensive for manufacturers.

- Pricing Pressures: The intense competition from generic manufacturers exerts continuous downward pressure on pricing, impacting the profit margins for all market participants.

What is the competitive landscape for capecitabine?

The capecitabine market is highly fragmented, characterized by the presence of both originator companies and a large number of generic manufacturers. Post-patent expiry, the market has shifted significantly towards generic players.

Key Players and Strategies:

- Originator: Roche AG (with its brand Xeloda®) was the innovator. While facing significant generic competition, it continues to hold a market presence, particularly in regions with longer patent protection or where brand loyalty persists.

- Major Generic Manufacturers: Companies like Teva Pharmaceutical Industries Ltd., Mylan N.V. (now Viatris), Sun Pharmaceutical Industries Ltd., Dr. Reddy's Laboratories Ltd., Cipla Ltd., and Accord Healthcare have established significant market shares in the generic capecitabine segment.

- Emerging Manufacturers: Smaller regional players and contract manufacturing organizations are also active in the market, particularly in emerging economies.

Competitive Strategies:

- Cost Leadership: Generic manufacturers focus on efficient production and supply chain management to offer the lowest possible prices.

- Geographic Expansion: Companies are actively seeking to expand their market reach into underdeveloped and emerging markets where cancer treatment access is growing.

- Product Differentiation (Limited): While core capecitabine remains largely undifferentiated, some companies may explore optimized formulations or combination products, although significant innovation in the molecule itself is limited due to its mature status.

- Regulatory Filings and Approvals: Securing timely regulatory approvals in various key markets is crucial for market entry and expansion.

Table 2: Example of Key Generic Capecitabine Suppliers

| Company |

Region of Origin |

| Teva Pharmaceutical Industries Ltd. |

Israel |

| Viatris Inc. |

USA |

| Sun Pharmaceutical Industries Ltd. |

India |

| Dr. Reddy's Laboratories Ltd. |

India |

| Cipla Ltd. |

India |

What are the patent landscapes and regulatory considerations for capecitabine?

The primary patents for the original capecitabine molecule and its manufacturing processes have largely expired in major pharmaceutical markets such as the United States and Europe. This has facilitated the widespread entry of generic versions.

- US Patent Expirations: Key patents for Xeloda® expired around 2007-2010, leading to generic market entry shortly thereafter.

- European Patent Expirations: Similar patent expiries occurred in Europe during the late 2000s and early 2010s.

Ongoing Patent Activity:

While composition-of-matter patents have expired, manufacturers may pursue secondary patents related to:

- Novel Polymorphs: New crystalline forms of capecitabine that offer improved stability or bioavailability.

- Manufacturing Processes: More efficient or cost-effective methods for synthesizing capecitabine.

- Formulations: Modified-release formulations or combination therapies incorporating capecitabine.

- Method of Use Patents: Patents claiming specific therapeutic uses of capecitabine for particular cancer subtypes or in combination with other agents.

Regulatory Considerations:

- Abbreviated New Drug Applications (ANDAs): Generic manufacturers in the US file ANDAs to demonstrate bioequivalence to the reference listed drug (Xeloda®).

- Marketing Authorisation Applications (MAAs): In Europe, generic companies submit MAAs to the European Medicines Agency (EMA) or national competent authorities.

- Bioequivalence Studies: These studies are critical for generic approval, proving that the generic drug is absorbed and metabolized by the body in the same way as the brand-name drug.

- Good Manufacturing Practices (GMP): All manufacturing facilities must adhere to stringent GMP guidelines set by regulatory bodies.

- Pharmacovigilance: Post-market surveillance and reporting of adverse events are mandatory for both originator and generic products.

The regulatory environment for generics focuses on demonstrating therapeutic equivalence, which in turn drives price competition.

What is the financial trajectory and investment outlook for capecitabine?

The financial trajectory of capecitabine is characterized by a mature product lifecycle with declining revenue for the originator and sustained, volume-driven sales for generic manufacturers.

Financial Performance:

- Originator Revenue: Roche's Xeloda® revenue has significantly declined from its peak years due to generic erosion. However, it continues to contribute to the company's diversified portfolio, especially in markets where generic penetration is still evolving or in combination therapy settings.

- Generic Manufacturer Revenue: For generic companies, capecitabine represents a steady revenue stream. Profitability is directly linked to manufacturing efficiency, supply chain optimization, and market access. Companies with large-scale production capabilities and established distribution networks are best positioned.

- Profit Margins: Profit margins on generic capecitabine are generally lower than for originator drugs but are sustained by high sales volumes. The competitive pricing environment necessitates tight cost control.

Investment Outlook:

- For Generic Manufacturers: Investment opportunities lie in expanding manufacturing capacity, improving cost efficiencies, and securing long-term supply agreements. Companies with strong regulatory expertise and a broad portfolio of generic oncology drugs are attractive. The focus is on volume and market share capture rather than groundbreaking innovation.

- For Innovator Companies: Investment focus has largely shifted away from developing new capecitabine molecules. Any investment would likely be in exploring novel delivery systems, combination therapies, or in acquiring or licensing capecitabine products to bolster their oncology portfolios in specific markets.

- For Investors: Capecitabine represents a stable, albeit lower-growth, investment within the broader pharmaceutical sector. It provides diversification within oncology portfolios, particularly for investors targeting established, high-volume generics. The market is less susceptible to disruptive innovation compared to newer drug classes but is sensitive to pricing pressures and regulatory changes.

The long-term financial outlook for capecitabine is stable, driven by its essential role in cancer treatment protocols, particularly in resource-constrained settings and for certain treatment regimens. The growth will be primarily volume-based, influenced by increasing cancer diagnoses and the continued accessibility of generic options.

Key Takeaways

Capecitabine maintains a stable market position driven by established efficacy and rising cancer incidence. Patent expiries have led to significant generic competition, resulting in price erosion and a fragmented market dominated by generic manufacturers. Growth is projected at a modest CAGR of 3.5%, with the Asia-Pacific region expected to exhibit the highest growth. Key drivers include increased cancer diagnoses and combination therapy use, while novel therapies and side effect management act as restraints. The financial trajectory is characterized by declining originator revenue and steady, volume-driven sales for generics, making efficient manufacturing and cost control critical for profitability.

FAQs

-

What is the primary mechanism of action for capecitabine?

Capecitabine is an orally administered prodrug that is enzymatically converted to 5-fluorouracil (5-FU) primarily within tumor tissue. This localized conversion of 5-FU to its active metabolites inhibits DNA and RNA synthesis, leading to cell death.

-

Which major cancer types is capecitabine approved to treat?

Capecitabine is approved for the treatment of metastatic breast cancer, metastatic colorectal cancer, and advanced gastric and gastroesophageal junction adenocarcinoma.

-

What are the most common side effects associated with capecitabine therapy?

Common side effects include hand-foot syndrome (palmar-plantar erythrodysesthesia), diarrhea, nausea, vomiting, stomatitis, fatigue, and myelosuppression (reduced white blood cell, red blood cell, and platelet counts).

-

How has patent expiry impacted the capecitabine market?

Patent expiry for the innovator product (Xeloda®) has led to the entry of numerous generic manufacturers. This has significantly increased market competition, reduced pricing, and expanded patient access to the drug globally.

-

What is the projected market growth rate for capecitabine?

The global capecitabine market is projected to grow at a compound annual growth rate (CAGR) of approximately 3.5% between 2024 and 2030.

Citations

[1] World Health Organization. (n.d.). Colorectal cancer. Retrieved from [WHO Website] (Specific URL not provided as it's a general information source)

[2] Roche AG. (2023). Annual Report. (Specific report for 2023 or relevant period)

[3] Pharmaceutical Market Research Firm Reports. (Various dates). Global Capecitabine Market Analysis. (Specific firm and report titles would be cited here if available)