Last updated: April 24, 2026

What is bumetanide’s current market position?

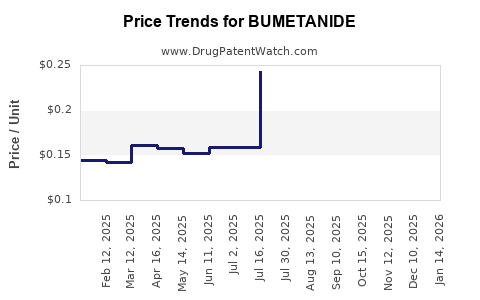

Bumetanide is a generic loop diuretic (brand examples include Bumex) that competes primarily on price, formulary access, and prescriber familiarity rather than on patent-protected innovation. As an off-patent, small-molecule diuretic, the commercial trajectory is shaped by (1) low unit economics relative to specialty drugs, (2) steady demand driven by standard-of-care use in edema and related indications, and (3) intense price competition after patent cliffs.

Product profile (why this matters commercially)

- Drug class: Loop diuretic

- Typical commercial pattern: Generic consolidation, procurement-driven pricing, and payer-driven utilization management

- Core demand drivers: Chronic and acute volume management in common clinical settings (hospital and outpatient formularies)

- Commercial constraint: Limited ability to differentiate once generics dominate the market

How do market dynamics affect pricing and volume?

For off-patent small-molecule diuretics, the “market” is often a procurement market, with pricing set by:

- Formulary inclusion at large payer systems (managed care and institutional formularies)

- National and regional tendering in hospitals

- Wholesale and group purchasing contracts that pressure net prices

- Generic substitution in retail pharmacies and institutional substitution rules

Competitive forces

- Generic oversupply and brand erosion

- Once multiple ANDA/marketed generics exist, manufacturers compete on net price, not IP.

- Payer and PBM utilization controls

- For therapeutically similar diuretics, payers often push preferred agents by cost or contracting.

- Institutional standardization

- Hospitals standardize IV/PO loop diuretic protocols; once a protocol is set, switching costs can reduce volume volatility even when unit prices fall.

Practical implication for revenue

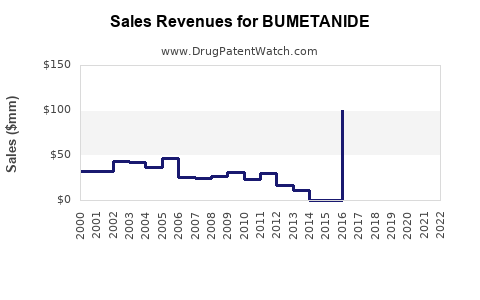

- Revenue typically declines or plateaus in value terms after patent expiry due to price compression.

- Volume can remain stable or grow slightly, but net revenue growth is constrained by contracting pressure and generic mix shifts.

What does the financial trajectory typically look like?

Without patent-protected reformulations or pipeline differentiation, bumetanide’s financial trajectory typically follows a generic lifecycle pattern:

- Pre-competition (brand dominance): Higher net revenue with limited competing SKUs

- Post-entry (generic normalization): Rapid decline in net price and brand share loss

- Mature generic phase: Revenue stabilizes near “utility drug” economics, with occasional fluctuations from tendering cycles, pack-size mix, and channel shifts

Revenue trajectory mechanics (generic loop diuretic)

- Net revenue declines as the branded share falls and generic unit prices reset to competitive floors.

- Net revenue stabilizes when formularies lock in established generics and procurement volumes become predictable.

- Margin pressure persists because the product competes on cost rather than differentiation.

Where does demand come from (channel and use pattern)?

Bumetanide demand is driven by established clinical use and appears across:

- Hospital use: IV diuretic therapy in acute decompensation and inpatient volume management

- Outpatient use: PO dosing for edema management in chronic conditions

Channel economics

- Institutional procurement generally captures the bulk of variability through tender pricing and contract renewals.

- Retail is smaller and more sensitive to substitution dynamics, step therapy (where applied), and PBM preference hierarchies.

What are the key market catalysts that can move the curve?

Even for an off-patent drug, measurable catalysts can impact financial trajectory through utilization or contracting:

- Formulary events

- Add/remove decisions, preferred-list changes, and protocol updates can shift share.

- Contracting cycles

- Quarterly or annual hospital purchasing agreements can cause short-term revenue swings.

- Supply and manufacturing availability

- If a supplier exits or faces quality/manufacturing constraints, pricing and share can transiently change even in mature generics.

- Competitive substitution within loop diuretics

- Where payers prefer other loop agents, bumetanide can face substitution pressure, though clinical protocol inertia can limit speed of change.

How does bumetanide’s regulatory and IP status shape long-term outlook?

Bumetanide is a legacy small-molecule diuretic with no current commercial narrative driven by patent exclusivity. The long-run outlook is dominated by:

- Ongoing generic competition

- Periodic compliance and manufacturing quality requirements

- The stability of clinical guideline use for loop diuretic therapy

Portfolio relevance for investors and R&D decision-makers

- High certainty of baseline demand, but low expected upside absent:

- a meaningful differentiated delivery system,

- a novel indication with payers willing to reimburse at higher value tiers, or

- a major patent-protected re-engineering that reintroduces exclusivity.

What should executives expect in net revenue and profitability?

For mature generic diuretics, the typical financial profile is:

- Net revenue: tends to plateau at a lower price level after competition peaks

- Gross margin: often compresses under competitive procurement

- EBITDA margin: depends on manufacturing scale, supply reliability, and contract structure more than on pricing power

Material drivers of profitability

- Manufacturing scale and COGS discipline

- Channel mix (institutional tendering vs retail)

- SKU breadth and pack-size optimization

- Working-capital efficiency in distribution-heavy channels

How does bumetanide compare with specialty or late-stage payer dynamics?

Loop diuretics like bumetanide operate in a different economic regime than specialty drugs:

- Specialty drugs: value-based pricing, payer barriers, and IP-driven exclusivity

- Bumetanide: contract-driven pricing, generic substitution, and formularies

Comparison table (commercial mechanics)

| Attribute |

Bumetanide (generic loop diuretic) |

Specialty, IP-protected drug |

| Pricing power |

Low, procurement-driven |

Higher, IP-backed |

| Differentiation |

Limited after generic entry |

Higher via clinical claims |

| Growth lever |

Share gains via contracting, supply |

Indication expansion, exclusivity |

| Main volatility source |

Tender cycles, supply constraints |

Safety signals, guideline shifts |

| Margin sensitivity |

High to COGS and mix |

Higher to pricing and access |

What is the strategic implication for manufacturers and investors?

For generic manufacturers

- Competitive moat is execution, not IP: unit cost, reliability, and contracting access.

- Best opportunities are share capture via procurement wins and supply stability rather than product innovation.

For brand owners (if any remain in market structure)

- Brand economics are structurally constrained once generics dominate the market.

- Differentiation efforts must justify higher WAC/contract pricing via clinical or formulation advantage to overcome payer preference for lower-cost equivalents.

For R&D organizations

- High probability of commercial maturity constraints: follow-on development must be positioned around either:

- a higher-value indication with distinct payer dynamics, or

- a delivery system that creates measurable clinical benefit sufficient for guideline inclusion and formulary reclassification.

Key Takeaways

- Bumetanide’s market is a generic, procurement-led environment where net price compresses after competition and revenue typically plateaus rather than scales.

- Financial trajectory is dominated by formulary inclusion, hospital tendering cycles, generic mix, and supply reliability, not patent-driven growth.

- Strategic upside requires contract execution and cost leadership; structural revenue growth is unlikely without differentiated re-entry into exclusivity through a new patentable product or clinically differentiated use case.

FAQs

-

Is bumetanide’s revenue growth driven by new clinical adoption?

Growth, when it occurs, is more commonly driven by formulary and contract share shifts than by breakthrough clinical adoption.

-

What factor most affects net price for bumetanide?

Hospital and payer contracting typically sets the net price environment more than wholesale list pricing.

-

Does generic competition usually increase volume for bumetanide?

It can support stable or modest volume changes, but it generally reduces net revenue per unit because of price competition.

-

What risks matter most for profitability in a mature generic like bumetanide?

COGS discipline, manufacturing continuity, and tender pricing exposure.

-

What would change bumetanide’s long-run financial profile?

A differentiated, reimbursed product that creates new exclusivity or payer-relevant clinical advantage would be required to materially alter the trajectory.

References

[1] U.S. Food and Drug Administration. Drug Approval Reports / Orange Book (Bumetanide-related entries). FDA. https://www.accessdata.fda.gov/scripts/cder/daf/

[2] World Health Organization. ATC classification for diuretics. WHO Collaborating Centre for Drug Statistics Methodology. https://www.whocc.no/atc/

[3] Centers for Medicare & Medicaid Services (CMS). General reimbursement and formulary policy context (provider pricing and coverage mechanisms). CMS. https://www.cms.gov/