Last updated: April 24, 2026

Brinzolamide, an ophthalmic carbonic anhydrase inhibitor, is a mature asset with stable demand driven by chronic glaucoma and ocular hypertension treatment patterns. The financial trajectory is characterized by (1) long-running generic penetration in most major markets, (2) price compression and channel pressure typical of off-patent ophthalmics, and (3) persistent unit volume supported by entrenched use and broad prescriber familiarity.

What market structure does brinzolamide face today?

Is demand driven by chronic disease management rather than episodic use?

Yes. Brinzolamide is used for long-term control of intraocular pressure (IOP) in:

- Open-angle glaucoma

- Ocular hypertension

This therapy pattern supports recurring prescriptions and reduces revenue volatility compared with acute-care drugs.

How competitive is the ophthalmic carbonic anhydrase inhibitor segment?

The segment is competitive, with multiple drug classes and multiple molecule options used in practice:

- Carbonic anhydrase inhibitors (including brinzolamide and dorzolamide)

- Beta blockers

- Alpha agonists

- Prostaglandin analogs

- Fixed combinations (common in glaucoma escalation pathways)

Within the molecule, competition is dominated by generic brinzolamide once patent coverage ended.

What does that imply for pricing power?

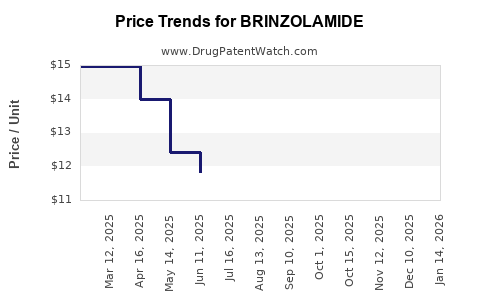

Pricing power is limited. In mature ophthalmics, generic entry typically:

- compresses net prices

- increases formulary depth

- shifts sales to lower-cost competitors

- forces manufacturers to compete on channel terms and rebates

How do patent and exclusivity dynamics affect revenue expectations?

Brinzolamide’s commercial outlook reflects an off-patent position in most markets, with generics supplying the majority of demand. Drugmaker revenue is therefore driven more by:

- inventory cycles and contract pricing

- distribution strength

- switching within class and between agents

- payer/formulary access

than by innovation-led premium pricing.

The practical result is a low-growth, margin-compressed revenue profile after generic saturation.

What is the financial trajectory profile for brinzolamide?

How does revenue typically behave post-generic entry?

The standard trajectory in mature ophthalmic products is:

- Peak-to-decline during the transition from branded to generic supply

- Stabilization at a lower price level as market share spreads across multiple generics

- Slow erosion as additional competitors enter or as prescribers shift to preferred options (including combination products)

For brinzolamide, the asset sits in the stabilization-to-erosion regime rather than a growth regime.

What are the main revenue drivers that still matter despite generic saturation?

Even with generic competition, revenue can remain steady when:

- the indication set stays unchanged (glaucoma and ocular hypertension)

- dosing schedules are maintained (topical ophthalmic, multiple daily dosing historically)

- clinicians keep carbonic anhydrase inhibitors in treatment algorithms

- patient switching stays limited due to tolerability and familiarity

What are the main headwinds?

Key headwinds include:

- generic price compression

- increased use of prostaglandin analogs and fixed combinations in first-line or escalation

- payer preference for lower-cost equivalents

- manufacturing and supply continuity risks common in sterile ophthalmic markets

How does formulary and payer behavior shape the income statement?

Does payer logic favor brinzolamide on cost-per-IOP control?

Payer behavior in glaucoma generally rewards therapies that deliver IOP reductions at the lowest net cost. In off-patent ophthalmics, that usually means:

- broad coverage for multiple generic carbonic anhydrase inhibitors

- tiering based on net price after rebates

- step edits that steer patients toward preferred agents

Brinzolamide can remain covered, but the payer economics reduce the margin pool.

How do channel terms affect realized margins?

For generic ophthalmics, margin is often determined by:

- distributor buying terms

- pharmacy benefit manager contracting

- rebate and allowance structures

As competition increases, gross-to-net conversion can worsen even if unit volumes remain stable.

What is the demand outlook and market growth rate?

Is the overall glaucoma therapy demand likely to grow?

Yes, the long-term driver is the prevalence of glaucoma and the need for chronic IOP management as populations age. That said, molecule-level performance depends on share allocation versus other drug classes, especially fixed combinations and better-tolerated regimens.

Will brinzolamide grow faster than the category?

Brinzolamide is unlikely to outgrow high-share classes like prostaglandin analogs and may track the category with limited upside, given:

- generic price caps

- competitive substitution between carbonic anhydrase inhibitors

- prescriber trend toward combination therapies

What product, formulation, and lifecycle factors can influence sales within brinzolamide?

Do formulation and dosing affect switching?

Yes. Brinzolamide’s commercial competitiveness depends on:

- bottle strength and dosing frequency relative to alternatives

- tolerability profile

- patient adherence impact from dosing schedule

- preservative system and local tolerability

Even within generics, these factors can influence pharmacy-level selection and clinician switching.

How does lifecycle management typically show up in mature generics?

Revenue maintenance often relies on:

- maintaining supply reliability

- incremental formulation improvements if allowed

- line extensions that preserve market share rather than expand total addressable demand

Which competitive sets most constrain brinzolamide?

What are the main within-class and class-shifting competitors?

Brinzolamide competes against:

- Dorzolamide (within carbonic anhydrase inhibitors)

- Prostaglandin analogs (often first-line)

- Beta blockers (common alternatives)

- Fixed combinations (commonly used to reduce regimen complexity)

Fixed combinations, in particular, can capture patients who might otherwise start or add brinzolamide.

How does the financial trajectory differ between branded and generic economics?

Branded economics

Branded products typically show:

- higher net price

- stronger gross margins pre-generic entry

- revenue decline once generics arrive

Generic economics

Generic supply tends to show:

- stable units but declining net realized price

- margin compression due to competitive bidding

- revenue dispersion across multiple manufacturers

For an off-patent molecule like brinzolamide, the dominant economic pattern is generic-like: volume continuity with margin erosion.

What does that mean for investing or R&D decisioning?

Is brinzolamide an R&D growth platform?

Not as a standalone platform. The molecule is mature, and incremental innovation faces:

- limited commercial premium versus established options

- rapid generic substitution risk

- payer and clinician preference for established regimens

Where can a new entrant still win?

Commercial upside typically comes from:

- differentiated formulation or delivery that improves tolerability or adherence

- combination product development that fits current prescribing workflows

- supply reliability and contracting execution

But the default financial trajectory for non-differentiated entrants remains price compression.

Key Takeaways

- Brinzolamide demand is supported by chronic glaucoma and ocular hypertension treatment patterns, but the market is mature and pricing power is constrained.

- The financial trajectory aligns with post-generic-entry dynamics: unit volume stability with revenue and margin pressure from price competition and formulary tiering.

- Competitive constraints come from both within-class agents (notably dorzolamide) and class-shifting options, especially prostaglandin analogs and fixed combinations.

- Sustainable profitability depends more on net pricing, contracting, and supply execution than on innovation-led premium economics.

FAQs

1) What drives brinzolamide demand?

Chronic management of IOP in open-angle glaucoma and ocular hypertension drives recurring prescriptions rather than episodic utilization.

2) Why is pricing typically pressured for brinzolamide?

Generic competition compresses net prices, while payer and channel contracting shifts economics from branded pricing to lowest-net-cost selection.

3) What competitors matter most to brinzolamide sales?

Within-class options include dorzolamide, and broader category pressure comes from prostaglandin analogs, beta blockers, and fixed combinations.

4) Does brinzolamide have upside from market growth?

Category demand from aging populations can support volume, but molecule-level growth is limited by share competition and price compression.

5) What determines realized margins for off-patent ophthalmics like brinzolamide?

Gross-to-net conversion, distributor and PBM contracting, supply continuity, and rebate or allowance structures.

References

[1] FDA. Azopt (brinzolamide) prescribing information. U.S. Food and Drug Administration.

[2] FDA. Trusopt (dorzolamide) prescribing information. U.S. Food and Drug Administration.

[3] FDA. Cosopt (dorzolamide/timolol) prescribing information. U.S. Food and Drug Administration.

[4] National Library of Medicine. Brinzolamide (drug information page). PubChem.