Last updated: June 19, 2026

BENICAR HCT market dynamics and financial trajectory: sales drivers, channel trends, pricing pressure, and exclusivity/IP impact

Executive summary: BENICAR HCT (olmesartan medoxomil + hydrochlorothiazide) is a long-established brand in the ARB plus diuretic hypertension segment. Market dynamics are dominated by (1) broad generic penetration, (2) sustained payor-driven formulary preference for lower-cost equivalents, and (3) residual brand price support in select plans. Financial trajectory is shaped by channel destocking cycles, rebate intensity, and competitive substitution within ARB/HCTZ combinations, with the brand now functioning primarily as an at-the-trade and formulary-management product rather than a growth engine.

How has BENICAR HCT performed financially over time, and what drives the trajectory?

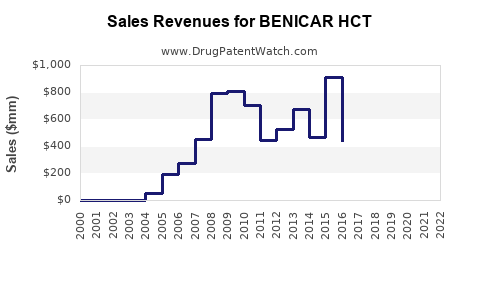

Short answer: BENICAR HCT’s financial trajectory has generally transitioned from branded growth to mature, then declining share and net sales as generics expanded. The remaining financial base is maintained through contracting leverage, rebate programs, and persistence of branded supply in certain formularies.

Key market forces shaping net sales

1) Generic substitution and pricing resets

- BENICAR HCT is a fixed-dose combination of olmesartan medoxomil and hydrochlorothiazide, both of which are widely available as generics or generic components.

- As combination generics take share, branded net pricing typically compresses through:

- lower gross-to-net due to higher rebates,

- tighter payer utilization management,

- increased pharmacy-level substitution.

2) Rebate intensity and formulary competition

- ARBs with diuretic backbones face multi-ARB competition and therapeutic substitution within “ARB + HCTZ” classes.

- Payer and PBM contracting tends to favor the lowest net-cost product on formulary, shifting demand away from brands with limited exclusivity.

3) Persistence vs switch behavior

- Switching costs are lower for oral antihypertensives than for many other therapy areas.

- Clinicians frequently switch patients between therapeutically equivalent ARB-based combinations when a lower-cost option becomes preferred on formulary.

What matters in BENICAR HCT P&L dynamics

- Gross-to-net trend: rising rebates and fee pressure are typical as generics gain traction.

- Volume trend: reduced growth and eventual volume erosion are expected when combination generics enter and expand.

- Mix trend: remaining brand demand often concentrates in:

- specific dose strengths,

- specific payer segments,

- patients already stabilized on the brand.

What does the competitive landscape look like for olmesartan medoxomil plus hydrochlorothiazide?

Short answer: Competition is largely structural: multiple ARBs plus thiazide combinations, plus generics for BENICAR HCT’s fixed-dose format. The brand’s economic position depends on payer contract status, not product differentiation.

Direct competitor set by therapeutic category

ARB/thiazide fixed-dose combinations

- Includes combinations from major manufacturers with established positions across PBM formularies.

- Competitive pressure also comes from:

- generic ARB + HCTZ combinations

- step-therapy preferences that restrict higher-cost combinations.

Single-entity substitution

- Many prescribers can substitute a separate ARB plus a generic thiazide (less dependent on fixed-dose combination availability).

- This increases competitive threat when payors steer toward the lowest net-cost regimen.

Channel and contract dynamics

- Community pharmacy filling behavior responds to:

- plan-specific preferred codes,

- pharmacy benefit changes,

- cash pay vs insured dynamics for selected patients.

- Institutional accounts can influence early uptake of preferred generics, but long-tail community usage usually dominates.

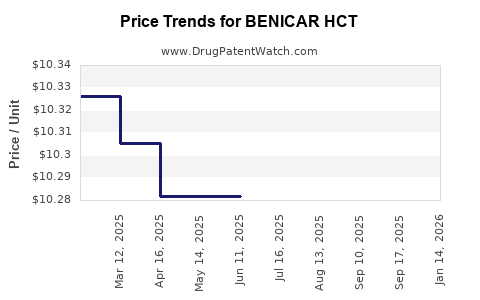

What role do pricing and rebates play in BENICAR HCT’s financial results?

Short answer: BENICAR HCT’s net sales are sensitive to rebate and contracting behavior as generics erode gross sales. With the brand in a post-exclusivity environment, gross price becomes a less reliable predictor than gross-to-net and plan adherence.

Typical levers in branded hypertension during generic pressure

- Rebate escalators tied to formulary tier placement.

- Market-share commitments that reduce net-cost for payors.

- Patient support programs (where applicable) that can reduce abandonment risk, but do not prevent substitution where benefit design strongly favors generics.

- Copay and administrative fees shifting financial burden from patient to manufacturer via contracted mechanisms.

Financial implication

- Brand net sales can remain relatively stable for periods even as underlying list prices fall or as volume declines, if rebates are managed and if the brand retains preferred status in certain plans.

- Once a larger share of plans move the brand off-preferred tiers, net sales typically step down.

What patents protect BENICAR HCT, and how does that shape the market?

Short answer: BENICAR HCT’s protective moat has narrowed with time as patents covering olmesartan medoxomil and specific combination-related claims have expired or become invalid for exclusion purposes. The resulting market is dominated by generic fixed-dose products and component-based substitution.

Patent estate structure relevant to market exclusivity

For fixed-dose ARB/thiazide products, IP protection typically splits into:

- Active ingredient/process patents (olmesartan medoxomil)

- Formulation patents (fixed-dose compositions, stability/solid-state approaches)

- Method-of-use patents (indications, dosing regimens, patient subsets)

- Combination-specific claims (if any remain)

How IP translates into commercial dynamics

- When exclusivity ends or when patents are no longer enforceable, entry of:

- ANDAs for combination generics,

- or product-by-product labeling alternatives,

accelerates substitution.

- Even if some patents remain, practical market impact is determined by:

- whether challengers obtained timely approvals,

- whether litigation resulted in launch design-arounds or settlements.

When does BENICAR HCT lose exclusivity, and what does that mean for generic launch timing?

Short answer: In most long-running ARB fixed-dose brands, exclusivity loss precedes sustained generic erosion. Generic launches generally occur at or shortly after the earliest legally permitted entry dates, with additional waves as later patents expire or are cleared.

How “loss of exclusivity” affects the curve

- Initial decline: begins when first generic entry reaches meaningful pharmacy adoption.

- Acceleration: happens when additional strengths/dose forms get approved and when payer formularies shift.

- Maturity: occurs when multiple competitors reduce net pricing through aggressive contracting.

What patent litigation affects BENICAR HCT and generic entry risks?

Short answer: Generic ARB/thiazide combinations typically face patent challenges that can delay entry for some time, but long-term outcomes usually produce broad market competition once patent barriers fall.

Litigation and settlement mechanisms that move markets

- Paragraph IV challenges: if filed, can trigger litigation that delays approval or modifies launch timing through settlements.

- Settlement agreements: can:

- delay launch until a defined date,

- limit product launch scope by strength or NDC,

- require brand concession or reverse payment structures.

Practical commercial impact

- Even with litigation, payors often prepare “switch-to-generic” protocols during pending cases.

- Once generics are approved and established, substitution becomes hard to reverse.

What is the Orange Book status of BENICAR HCT, and how many listed patents matter commercially?

Short answer: Orange Book status governs regulatory eligibility for generic substitution and the legal basis for Paragraph IV challenges. Commercially relevant patents are those that are:

- still listed for the marketed formulation/strengths,

- enforceable and not effectively eliminated by earlier expirations or litigation outcomes,

- linked to the specific NDA product and dosage form.

How to interpret Orange Book listings for a fixed-dose combination

- Patent lists can include multiple families and claim types.

- Not all listed patents stop generic entry. Key commercial impacts come from:

- patents that are blocking for a generic applicant’s proposed product,

- patents that are resolved through settlement or final judgments.

What formulations are protected for BENICAR HCT, and where are design-around opportunities?

Short answer: For fixed-dose antihypertensive products, formulation protection tends to be narrow and harder to monetize once generics match strength, release behavior, and bioequivalence. Design-around opportunities become more common as combination generics scale.

Formulation risk areas for challengers

- Stability and manufacturability: fixed-dose combinations can create formulation-specific constraints, though many are overcome by development and BE studies.

- Bioequivalence pathways: once BE is demonstrated, design differences in inactive ingredients often do not impede approval.

- Solid-state specifics: can be a patent hook, but many such patents expire quickly relative to the overall product lifecycle.

Biosimilar or biologics risk: is BENICAR HCT exposed to biosimilar dynamics?

Short answer: No. BENICAR HCT is a small-molecule oral antihypertensive. Biosimilar dynamics do not apply.

What “replacement” looks like instead

- Generic substitution, not biosimilar competition.

- Therapeutic switch among ARBs and ARB combinations with diuretics.

How does BENICAR HCT compare with other ARB/thiazide combination brands on market positioning?

Short answer: In the ARB/thiazide category, differentiation is limited once generics enter. Brand position typically correlates with:

- formulary access,

- net price competitiveness,

- patient adherence and persistence due to prescriber familiarity.

Competitive comparison criteria that drive outcomes

- Preferred tier status on major PBM formularies

- Contracted rebate levels

- Dose coverage and NDC availability

- Pharmacy channel adoption and substitution rules

- Persistence among patients titrated to stable doses

What generic entry risks exist for BENICAR HCT, and how could they affect revenues?

Short answer: Generic entry risk is already structurally realized in most markets for long-standing combination antihypertensives. Remaining revenue exposure is primarily tied to:

- additional generic approvals for remaining strengths,

- payer formulary tier changes,

- accelerated substitution following further contract resets.

Revenue exposure triggers

- New generic introductions across additional NDCs.

- Payer contract renegotiations that reclassify the brand to non-preferred tiers.

- Broader “class-wide” preferred status for selected ARB/HCTZ competitors.

What manufacturing and IP barriers slow down generic penetration for combination drugs?

Short answer: The primary barriers are regulatory BE and formulation/manufacturing controls, not complex IP constraints at this stage. Practical barriers include maintaining consistent quality and demonstrating equivalence for fixed-dose combinations.

Practical friction points

- Process scale-up stability for the combination matrix.

- Analytical equivalence across strengths.

- Supply chain robustness to sustain multiple NDCs across markets.

What is the commercial outlook for BENICAR HCT?

Short answer: The near-to-mid term outlook is dominated by continued pricing compression and gradual share erosion as generic availability and payer preferences consolidate around lower-cost options. Brand performance is likely to stabilize only where it retains preferred access and where remaining non-substitutable segments (inertia) persist.

Where brand value can persist

- Plans that keep the brand in preferred or mid tiers due to negotiated economics.

- Patients stable on the brand with prescriber preference and lower switch rates.

- Residual demand in strengths where generic penetration is incomplete or contracting favors branded supply.

Key Takeaways

- BENICAR HCT’s market is dominated by generic competition in the fixed-dose ARB plus thiazide space; the brand’s financial trajectory reflects pricing and rebate pressure more than product growth.

- Competitive outcomes are driven by PBM formulary placement, net pricing, and substitution dynamics, with limited clinical differentiation once generics are established.

- IP effects manifest through Orange Book status and litigation/settlement outcomes, but long-term market structure increasingly favors generic penetration.

- Commercial upside is constrained; remaining brand value is tied to contract status and patient persistence in select payer segments.

- Biosimilar risk is not applicable; competitive replacement is via generics and therapeutic switching within ARB combinations.

FAQs

1) Is BENICAR HCT still a “brand vs generic” play in major US formularies?

It behaves as a mature brand under heavy generic substitution pressure, with value tied to contracting and tier placement rather than exclusivity-driven demand.

2) How does pharmacy substitution typically impact BENICAR HCT demand?

Substitution accelerates once generics become preferred and widely available at lower net cost, reducing branded fills unless constrained by plan design or prescriber restrictions.

3) What does “net sales” sensitivity imply for BENICAR HCT under pricing pressure?

Net sales track gross-to-net changes: rebate escalation and contracting shifts can offset some volume decline until formulary access changes trigger larger drops.

4) Do method-of-use or formulation patents meaningfully protect BENICAR HCT after generic entry?

Protection usually narrows over time; when core fixed-dose equivalence is achieved and BE is established, practical enforcement leverage declines versus payer substitution mechanics.

5) What competitive strategy most affects BENICAR HCT revenue exposure going forward?

Payer contract strategy and dose-NDC coverage by generics, which influence switching speed and the ability to displace branded preferred access.

References (APA)

- FDA. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/ (accessed via Orange Book search functions)

- FDA. ANDA Basics. U.S. Food and Drug Administration. https://www.fda.gov/ (accessed via FDA ANDA resources)