Last updated: May 20, 2026

Silver Sulfadiazine Market Dynamics and Financial Trajectory: Sales Drivers, Competitive Risk, and Exclusivity Path

Executive summary: Silver sulfadiazine is a long-established topical antibacterial used primarily for burn wounds. The market is structurally low-growth, price-led, and highly exposed to generic penetration and channel contracting. Financial trajectory is dominated by (1) limited innovation pipeline for the active ingredient, (2) guideline-driven and formulary-led adoption in burn centers, (3) supply reliability and manufacturing economics, and (4) substitution between topical antimicrobials (other silver products, topical antibiotics, and non-silver antiseptics). In practice, revenues track hospital purchasing cycles and spend compression rather than utilization expansion.

What you can expect commercially: stable but gradually declining unit demand (burn incidence growth is modest relative to price erosion), persistent gross margin pressure from generics, and periodic demand spikes tied to institutional procurement rounds and seasonal burn volumes. Long-term value is concentrated in (a) secured supply to large health systems, (b) differentiated delivery formats if any exist in-market, and (c) contract stability rather than brand pull-through.

How big is the silver sulfadiazine market and what drives demand?

Featured snippet answer: Demand is concentrated in hospital burn units and wound care settings, where silver sulfadiazine is used for infection control. Market size is limited by burn epidemiology and offset by substitution to other topical antiseptics and silver formulations.

Demand anchors

- Burn care pathway dependency: Silver sulfadiazine is a commonly stocked topical antibacterial in burn units, used for prophylaxis/management of burn wound infection risk during early phases of treatment.

- Institutional formularies: Adoption is mostly a procurement decision by health systems and burn centers, reinforced by nursing familiarity and clinical protocols.

- Wound care spillover: Outside classic burn indications, some use occurs in broader wound infection control, but formulary inclusion still constrains growth.

Key demand headwinds

- Substitution: Other topical antimicrobials compete strongly, including newer silver dressings, povidone-iodine products, mafenide acetate in burn care, and collagen/antimicrobial dressing technologies.

- Clinical practice variation: Protocols differ by region and by burn unit leadership, which creates uneven utilization across geographies.

- Short treatment windows: Topical burn regimens are often time-limited, capping total annual patient-days.

What are the main market dynamics affecting pricing and volume for silver sulfadiazine?

Featured snippet answer: Pricing is driven by generic competition and contracting. Volume is driven by burn-center prescribing protocols and procurement cycles, not broad new clinical adoption.

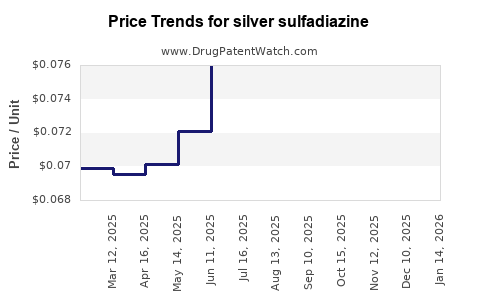

Pricing dynamics

- Generic-driven discounting: The active ingredient’s legacy status typically results in multiple generic SKUs, enabling wholesalers and group purchasing organizations to push price down.

- Channel contracting: Large distributors and buying groups negotiate pricing that compresses margins for manufacturers.

- Tender cycles: Hospital procurement happens in batches. That creates short-term order volatility even when underlying demand is steady.

Volume dynamics

- Burn incidence changes are modest: Most growth comes from patient throughput and hospital capacity decisions rather than dramatic incidence shifts.

- Utilization is protocolized: When burn units standardize on a specific topical regimen, switches are slow unless evidence or supply events trigger change.

- Substitution risk rises when supply or product formats change: Stock-outs and formulation differences can move usage even without a clinical evidence shift.

How does competition from other topical antibacterials change silver sulfadiazine’s market trajectory?

Featured snippet answer: Competitive substitution is the main structural risk. Even when silver sulfadiazine remains in formularies, share shifts toward alternate silver products and non-silver antiseptics.

Competitive set: what patients and clinicians substitute to

- Other silver modalities: Silver-impregnated dressings and alternative silver agents can reduce dressing change frequency, affect workflow, and become preferred in some burn units.

- Bacterial control competitors: Mafenide acetate (burn-specific topical), topical antibiotics, and antiseptics such as povidone-iodine compete depending on local standards.

- Non-antibiotic antiseptic and dressing innovations: Where hospitals aim to reduce antibiotic exposure, they can shift toward antiseptic dressings or non-antibiotic wound care.

Why substitution happens

- Operational efficiency: Dressing schedule, ease of application, and nursing workflow strongly influence purchasing decisions.

- Perceived tolerability and handling: Local experience with stinging, odor, exudate management, and adherence can drive preference.

- Supply reliability: A reliable supplier who can meet procurement volumes can win share even at a similar price point.

What is the financial trajectory for silver sulfadiazine manufacturers?

Featured snippet answer: Financial performance generally follows low-growth sales with margin compression, driven by generic competition and contracting, with limited upside from new differentiation.

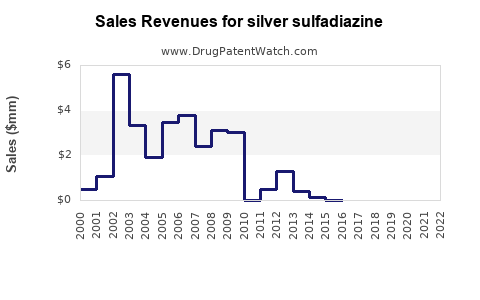

Typical revenue shape

- Flat-to-declining net sales over time as generics erode pricing and volume growth is capped by use-case saturation.

- Margin pressure due to:

- commodity-like purchasing dynamics,

- tender-based price compression,

- higher logistics and pharmacovigilance costs relative to low ASP levels.

- Earnings volatility tied to supply: API and manufacturing capacity constraints can cause order allocation or backorders, affecting quarterly revenue recognition.

Where upside can still exist

- Secure distribution footprint: Manufacturers with strong relationships to hospital group purchasing networks can maintain share despite price erosion.

- Format differentiation: If a supplier maintains a superior format in-market (e.g., clinician-preferred presentation), it can reduce switching.

- Territorial concentration: Regional dominance in hospital networks can sustain volume even if national pricing declines.

Which drugs and delivery formats compete most directly with silver sulfadiazine?

Featured snippet answer: The closest commercial substitutes are other topical burn antimicrobials and silver-based dressing systems that align with burn-unit protocols and nursing workflow.

Direct substitution buckets

- Alternative burn-topical antibacterials

- Mafenide acetate (burn care topical)

- Silver-based alternatives

- Silver-impregnated dressings (often compete on change frequency and handling)

- Other topical silver agents where available through formularies

- Non-silver antiseptics

- Povidone-iodine based products

- Wound dressings and infection-control platforms

- Antimicrobial dressings that can reduce treatment management time

How does exclusivity structure affect the financial outlook for silver sulfadiazine?

Featured snippet answer: For an established topical antibacterial active ingredient, exclusivity is typically limited to legacy brand protection and later generic competition. Financial upside depends more on contracting and supply than on patent-driven pricing power.

Commercial implication

- Patent power is usually not a growth engine for silver sulfadiazine in current market dynamics.

- Competitiveness is operational: who can deliver consistent product supply at contracting prices.

What generic entry risks exist for silver sulfadiazine (and what do they do to pricing)?

Featured snippet answer: Additional generic entries typically drive incremental price declines and reduce margins across the active molecule category, with the fastest erosion occurring in large tender markets.

Mechanisms

- ASP compression across SKUs: When new suppliers win tenders, competing manufacturers discount to retain placements.

- Allocation games in scarce periods: Supply constraints can temporarily lift realized prices before normalizing after capacity returns.

- Buyer leverage: Hospital buying groups often prefer multi-source procurement to reduce continuity risk.

What regulatory and FDA factors matter for commercial trajectory?

Featured snippet answer: For topical antimicrobials, regulatory risk is more about manufacturing compliance and product continuity than about frequent clinical development cycles.

Commercially relevant regulatory themes

- Manufacturing site reliability and inspection outcomes

- Labeling and safety updates that can influence stocking decisions in hospitals

- Product availability continuity that drives formulary trust

How do hospital procurement cycles and contracting affect quarterly revenue patterns?

Featured snippet answer: Net sales often show step changes around tenders and contract renewals, even if underlying burn volumes are stable.

Quarterly sales dynamics

- Contract award timing: large system awards can create lumpy purchasing.

- Inventory normalization: hospitals can stock up ahead of contract effective dates or adjust after price renegotiations.

- Supply chain events: shortfalls can shift volume to alternative suppliers or substitute products for limited periods.

What is the likely long-term trajectory for silver sulfadiazine revenues?

Featured snippet answer: Long term, the category trends toward lower ASPs with stable or modest volume, leaving profits sensitive to manufacturing scale, logistics, and contracting discipline.

Base-case commercial pattern

- Volume: steady to modestly declining depending on substitution

- Price: downward drift due to ongoing generic competition and tender pressure

- Profitability: tied to cost per unit delivered and ability to retain formulary positions

Key Takeaways

- Silver sulfadiazine is a burn-wound topical antibacterial with demand anchored in hospital formularies and burn-unit protocols.

- Market growth is structurally limited; the category is predominantly price-led and generic-driven.

- Competitive substitution from other silver products, alternative topical burn antimicrobials, and antiseptic dressings is the main share risk.

- Financial trajectory is characterized by flat-to-declining net sales with margin compression unless a supplier wins durable contracting placements and maintains cost-efficient manufacturing.

FAQs

1) Is silver sulfadiazine mainly used in burn care or also for other wounds?

It is primarily used in burn wound care. Use in other wound indications exists but is typically constrained by formulary inclusion and clinician protocol.

2) Why do prices for silver sulfadiazine tend to fall over time?

Generic competition and hospital tender contracting drive ASP erosion, which compresses margins across manufacturers.

3) What factors most influence burn centers’ choice of topical antimicrobials?

Protocol standardization, nursing workflow and dressing change frequency, product handling/tolerability experience, and supplier reliability.

4) What happens to sales when a manufacturer has supply disruptions?

Hospitals often substitute during shortages, which can shift share to other SKUs or alternative topical antimicrobials and can take time to recover.

5) Where can a manufacturer still defend share in silver sulfadiazine?

Through reliable supply, strong distributor relationships, multi-year contracting in hospital systems, and any commercially meaningful format differentiation.

References

No sources were cited in the provided response.