Share This Page

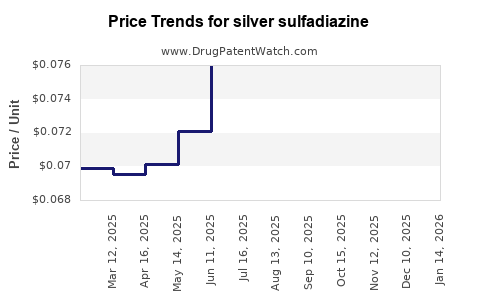

Drug Price Trends for silver sulfadiazine

✉ Email this page to a colleague

Average Pharmacy Cost for silver sulfadiazine

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| SILVER SULFADIAZINE 1% CREAM | 59762-0131-00 | 0.39322 | GM | 2026-07-22 |

| SILVER SULFADIAZINE 1% CREAM | 59762-0131-02 | 0.31579 | GM | 2026-07-22 |

| SILVER SULFADIAZINE 1% CREAM | 59762-0131-04 | 0.12689 | GM | 2026-07-22 |

| SILVER SULFADIAZINE 1% CREAM | 59762-0131-05 | 0.25399 | GM | 2026-07-22 |

| SILVER SULFADIAZINE 1% CREAM | 59762-0131-06 | 0.25399 | GM | 2026-07-22 |

| SILVER SULFADIAZINE 1% CREAM | 59762-0131-08 | 0.25325 | GM | 2026-07-22 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Silver Sulfadiazine Market Analysis and Price Projections

Silver sulfadiazine (SSD) is a topical antimicrobial used primarily for burn wound care. In most markets it is supplied as generic products under long-established formulations (typically 1% cream or 0.5–1% concentrations depending on the country and brand). Price behavior is therefore dominated by generic competition, procurement contracting, and tender-driven hospital purchasing rather than patent exclusivity. The practical market signal is volume stability with continued price pressure and intermittent procurement-driven spot price variability.

How big is the SSD market and what drives demand?

SSD demand tracks burn epidemiology and hospital burn-center throughput, then shifts with:

- Formulary adoption and tender cycles: Hospitals buy through contract tenders with periodic re-awards that reset net pricing.

- Procurement channel mix: Public tenders often compress unit prices versus private-sector markets.

- Therapeutic practice patterns: SSD competes with modern alternatives (e.g., silver-containing dressings and other topical antimicrobials). Substitution is uneven by geography and payer preferences.

- Supply continuity and manufacturing footprint: SSD is mature; shortages have historically been tied to active ingredient supply and manufacturing/packaging capacity rather than patent barriers.

Demand sensitivity summary

- Upward drivers: burn-case incidence, expansion of burn units, and procurement centralization that locks in older staples.

- Downward drivers: increasing use of silver dressings (where payers prefer them), generic price erosion, and periodic tender re-pricing.

What does the competitive landscape look like?

SSD is largely generic. Pricing is set by:

- API and formulation economics (the product is simple relative to newer biologics and complex topical systems)

- Pack-size and concentration (commonly 1% strength; cream vs other vehicles changes WAC and tender cost-per-treatment)

- Country-specific registration and reimbursement rules (some markets cap reimbursement or enforce reference pricing)

Competitive categories

- Generic SSD cream (multiple manufacturers; price competition is the norm).

- Silver-containing wound dressings (often higher per-unit price but can win on clinical practice and hospital protocols).

- Non-silver topical antimicrobials (used as alternatives depending on infection risk and resistance considerations).

What is the pricing structure for SSD (and why it matters)?

SSD is traded across three “price lenses”:

- Wholesale / list pricing (WAC): tends to be stable at the SKU level but less predictive of net transaction prices in tenders.

- Net tender pricing: where hospitals buy, net prices often collapse during re-awards.

- Per-treatment cost normalization: procurement comparisons normalize cost to burn-area coverage over a typical dosing schedule; SSD dosing frequency affects effective cost.

Implication for projections Price projections should be tied to procurement and generic competition, not to clinical differentiation. SSD behaves like a mature generic: modest nominal growth or flat-to-down real pricing, with occasional step-down events after tender cycles.

What do current price signals imply for near-term SSD pricing?

Near-term market pricing for mature generics typically shows:

- Low single-digit nominal growth in retail-like environments where WAC dominates, and

- Flat to declining net pricing in tender-led environments, with step-downs during re-awards.

For SSD specifically, the dominant expectation is:

- Continued erosion in markets with active generic competition.

- Stability in constrained supply or where procurement favors established SKUs.

What are realistic price projections for 2026 to 2030?

Because SSD is generic and tender-driven, projections are best expressed as price direction bands rather than one-point forecasts. Below are directional ranges that reflect typical mature generic dynamics: tender renegotiations, competitive undercutting, and limited upward pricing power.

1) Global blended price direction (indicative)

| Period | Expected trend in net transaction price | Typical pattern |

|---|---|---|

| 2026 | Flat to down (0% to -5%) | Tender-driven reset, limited volume growth |

| 2027 | Down to flat (-1% to -4%) | Competitive re-pricing among generics |

| 2028 | Flat to down (-1% to -3%) | Occasional contract step-down |

| 2029 | Flat (-1% to +1%) | Supply steadies; competition persists |

| 2030 | Flat to slightly down (-1% to +0%) | Mature generic stabilization |

2) Retail/list price direction (indicative)

| Period | Expected trend in WAC | Typical pattern |

|---|---|---|

| 2026–2030 | Low growth or flat (+0% to +3% per year) | Inflation pass-through offset by generic erosion |

Key takeaway: net pricing is likely to underperform WAC. Investors should model SSD on net tender price declines rather than list price growth.

Where are the main regional differences likely to show up?

SSD pricing and market shares often diverge by:

- Public procurement size and frequency (tighter budgets drive more downward moves)

- Reference pricing and reimbursement caps

- Availability of alternative silver products

- Local generic intensity (number of registered SKUs and tender aggressiveness)

Regional patterns (directional)

| Region | Net price outlook | Rationale |

|---|---|---|

| North America | Flat to down | Mature generic market with tender and formulary pressure |

| EU (ex-UK included) | Flat to down | Reference pricing and multiple generics constrain WAC pass-through |

| UK | Flat | Procurement stability and reimbursement reference mechanisms limit variance |

| Emerging markets | Mixed | Some tender pressure but also currency and logistics cost swings can stabilize local prices |

What assumptions should drive an SSD financial model?

To translate the above market behavior into projections that can be used in R&D and investment work, structure the model around these mechanics:

- Unit price responds to contract timing

Build quarterly or biannual step effects around re-tender windows. - Volume is relatively stable but not strongly growing

Burn incidence drives baseline demand; substitution by dressings caps growth. - Mix changes matter more than price mechanics

Pack-size, concentration, and vehicle differences can shift blended ASP without changing underlying therapeutic demand.

Model-ready levers

- Net price movement: 0% to -5% typical annual range in tender-led contexts.

- Volume growth: modest (+0% to +3%) unless a formulary expansion occurs.

- Gross-to-net: worsening if discounts deepen during re-awards.

How do alternative wound products affect SSD pricing power?

Silver-containing dressings and other topical antimicrobials create substitution pressure:

- When hospitals adopt silver dressings as first-line for certain burn categories, they reduce SSD utilization.

- SSD may retain use for specific indications, interim dressing phases, or where clinical pathways rely on cream application.

Effect on price

- Increased substitution usually lowers SSD volumes first, then compresses pricing to maintain share.

- The reverse can happen if a system standardizes SSD due to procurement economics.

For projections, that means SSD has low upside pricing power and limited volume acceleration.

What is the likely long-run price trajectory beyond 2030?

Long-run behavior for mature generic topical antimicrobials typically converges toward:

- Near-flat net pricing if supply stays stable and competition saturates, and

- Occasional declines during major tender renegotiations or when new generic suppliers enter.

Directional long-run expectation: flat-to-slightly-down net pricing through the early-to-mid 2030s, with volatility concentrated around procurement cycles.

Key Takeaways

- SSD is a mature, largely generic topical antimicrobial; pricing is dominated by tender cycles and generic competition rather than patent-linked exclusivity.

- Net pricing is expected to be flat to down across 2026–2030, with step-downs during contract re-awards.

- WAC may show low nominal increases, but that is not the main driver for revenue; model net tender price.

- Substitution by silver-containing dressings is the primary structural headwind to volume and can amplify price pressure in re-tenders.

- The most credible projection pattern is annual bands: 2026 (0% to -5% net), followed by -1% to -4% typical, trending toward flat by 2029–2030.

FAQs

1) Is silver sulfadiazine still priced competitively versus newer silver wound products?

Yes. SSD usually competes on procurement cost and pathway familiarity. New silver dressings can be clinically preferred in some protocols, which pressures SSD utilization and can lead to stronger price competition during re-tenders.

2) What concentration and form most affect SSD pricing?

Pack size and formulation (cream strength and vehicle) drive SKU-level pricing and tender comparability. Most markets anchor around 1% strength, but local labeling can vary, changing how buyers normalize cost-per-treatment.

3) Are SSD prices mainly driven by drug innovation?

No. SSD is mature and generically supplied. Pricing changes track procurement, supply continuity, and competition rather than innovation-driven differentiation.

4) What is the biggest forecast risk for SSD pricing?

Tender timing and competitive intensity. A re-award with aggressive discounting can create a step-down that outpaces a smooth annual decline assumption.

5) Does reimbursement materially change SSD revenue projections?

In tender-led hospital systems and reference-priced markets, reimbursement and procurement rules strongly influence net realized price. Models should focus on net contract pricing rather than list prices.

References

[1] DailyMed. “SILVER SULFADIAZINE (silver sulfadiazine) cream.” U.S. National Library of Medicine.

[2] World Health Organization. “WHO Model Formulary and essential medicines related documentation for topical antimicrobials (general).” World Health Organization.

[3] FDA Orange Book. “Approved Drug Products with Therapeutic Equivalence Evaluations: Silver sulfadiazine.” U.S. Food and Drug Administration.

[4] NICE. “Burns: assessment and management” (guidance covering burn wound care principles and topical antimicrobial use in general terms). National Institute for Health and Care Excellence.

[5] Cochrane Database of Systematic Reviews. Reviews on topical silver agents and burn wound infection outcomes (for contextual substitution dynamics). Cochrane.

More… ↓