Last updated: February 19, 2026

Meropenem, a broad-spectrum carbapenem antibiotic, faces a mature market characterized by significant generic competition and increasing antimicrobial resistance (AMR). Its financial trajectory is influenced by pricing pressures, the emergence of novel antibacterial agents, and the ongoing demand in hospital settings for treating severe infections.

What is Meropenem's Current Market Position?

Meropenem occupies a critical position in the hospital antimicrobial armamentarium, primarily for the treatment of serious Gram-positive and Gram-negative bacterial infections. As a carbapenem, it is often reserved for infections resistant to other antibiotic classes, including complicated intra-abdominal infections, hospital-acquired pneumonia, and meningitis [1]. The global market for meropenem is substantial, driven by its efficacy against a wide range of pathogens, including those producing beta-lactamases.

The market is characterized by:

- High Generic Penetration: Following patent expiries, numerous generic versions of meropenem have entered the market. This has led to significant price erosion and intensified competition among manufacturers. Key players in the generic meropenem market include companies such as Fresenius Kabi, Hikma Pharmaceuticals, and Aurobindo Pharma.

- Established Use in Hospitals: Meropenem remains a frontline therapy in hospital environments due to its broad spectrum of activity and favorable safety profile when compared to some other carbapenems. Its intravenous administration is standard for serious infections.

- Antimicrobial Resistance Concerns: While meropenem is effective, the increasing prevalence of carbapenem-resistant Enterobacteriaceae (CRE) poses a growing challenge. This resistance is driven by the production of carbapenemases, such as KPC and NDM-1. The rise of AMR necessitates careful stewardship of carbapenem use and drives research into alternative treatment strategies [2].

- Geographic Segmentation: The demand for meropenem is highest in regions with a high burden of hospital-acquired infections and advanced healthcare infrastructure, including North America, Europe, and parts of Asia. Emerging economies also represent growth opportunities as healthcare access expands, though pricing remains a significant factor.

What are the Key Market Drivers and Restraints?

The market for meropenem is shaped by a confluence of factors, including its therapeutic utility and the evolving landscape of infectious disease treatment.

Market Drivers:

- Prevalence of Hospital-Acquired Infections (HAIs): HAIs remain a significant cause of morbidity and mortality globally. Meropenem's broad-spectrum activity makes it a crucial tool in combating these challenging infections [3].

- Rising Incidence of Drug-Resistant Bacteria: As resistance to older antibiotic classes grows, the reliance on potent agents like meropenem increases. It is often a drug of last resort for severe infections where other treatments have failed.

- Increasing Geriatric Population: Elderly patients often have weakened immune systems and comorbidities, making them more susceptible to severe infections. This demographic trend contributes to sustained demand for effective broad-spectrum antibiotics.

- Advancements in Healthcare Infrastructure: Expansion of healthcare facilities, particularly in developing regions, coupled with increased diagnostic capabilities, leads to greater utilization of advanced antibiotic therapies like meropenem.

- Off-Label Use and Combination Therapies: Meropenem is sometimes used in combination with other antibiotics or in specific off-label indications to broaden coverage against polymicrobial infections or suspected resistant pathogens, further contributing to its demand.

Market Restraints:

- Intense Generic Competition and Price Erosion: The generic nature of meropenem has led to aggressive pricing strategies by manufacturers, limiting revenue growth potential for individual companies.

- Development of Novel Antibacterial Agents: The ongoing research and development of new antibiotics with novel mechanisms of action, particularly those targeting resistant organisms, could eventually offer alternatives to carbapenems.

- Antimicrobial Stewardship Programs: The implementation of strict antimicrobial stewardship programs aims to optimize antibiotic use, reduce unnecessary prescriptions, and conserve the efficacy of important drugs like meropenem. This can lead to more judicious use and potentially lower overall consumption.

- Emergence of Carbapenem Resistance: The growing threat of CRE necessitates careful management of meropenem use. Over-reliance can accelerate the development of resistance, limiting its long-term utility.

- Regulatory Scrutiny and Approval Pathways: While meropenem is an established drug, any new formulations or indications would be subject to rigorous regulatory review, which can be time-consuming and costly.

What is the Financial Trajectory and Revenue Landscape?

The financial trajectory of meropenem is characterized by a large but stable market size with modest growth, primarily driven by volume rather than significant price increases.

| Metric |

Value/Trend |

Notes |

| Global Market Size |

Estimated at USD 2 billion - 2.5 billion (2023) |

Reflects demand for the active pharmaceutical ingredient (API) and finished dosage forms. |

| Annual Growth Rate (CAGR) |

3% - 5% (projected 2024-2030) |

Driven by increasing infection rates in developing economies and persistent HAI prevalence. |

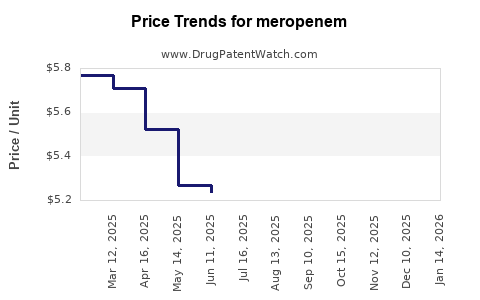

| Average Selling Price (ASP) |

Declining trend in developed markets |

Due to intense generic competition and pricing negotiations by large healthcare providers. |

| Key Revenue Drivers |

Volume sales in hospital settings |

High unit sales required to offset lower ASP. |

| Profitability |

Moderate, dependent on manufacturing efficiency |

Lower profit margins for generic manufacturers compared to originator drugs. |

| API Manufacturers |

Dominated by companies in India and China |

Lower production costs in these regions. Examples include Divi's Laboratories, Cipla. |

| Finished Dosage Form (FDF) Manufacturers |

Diverse landscape of generic and biosimilar producers |

Includes global pharmaceutical companies and regional players. |

Key Financial Aspects:

- Volume-Driven Growth: Revenue growth is primarily achieved through increased unit sales rather than price appreciation. This is a common characteristic of mature generic drug markets.

- Cost Optimization: For API and FDF manufacturers, operational efficiency and cost-effective sourcing of raw materials are critical for maintaining profitability.

- Market Access and Reimbursement: In developed markets, securing favorable reimbursement and formulary placement is essential for market share. This often involves competitive bidding and demonstrating cost-effectiveness.

- Emerging Market Potential: While ASP is lower in emerging markets, the increasing volume of prescriptions due to expanding healthcare access presents a significant growth avenue.

- Competition from Novel Therapies: The potential market share erosion from newer antibiotics targeting resistant pathogens is a long-term financial consideration, though meropenem's established role for specific indications will likely persist.

What is the Competitive Landscape?

The competitive landscape for meropenem is highly fragmented, dominated by generic manufacturers. The era of patent exclusivity for the originator product has long passed, leading to a proliferation of suppliers worldwide.

Key Competitors and Strategies:

- Generic API Manufacturers: Companies specializing in the production of the active pharmaceutical ingredient (API) are crucial to the supply chain. These often include large Indian and Chinese chemical and pharmaceutical companies, such as:

- Divi's Laboratories

- Cipla

- Lupin

- Sun Pharmaceutical Industries

These entities focus on large-scale, cost-efficient production to supply FDF manufacturers globally.

- Generic Finished Dosage Form (FDF) Manufacturers: These companies formulate the API into injectable solutions or powders for reconstitution. The competitive strategies revolve around:

- Price Leadership: Offering the lowest possible price to gain market share, particularly in tenders and hospital supply contracts.

- Supply Chain Reliability: Ensuring consistent product availability and a robust distribution network to meet demand from hospitals. Examples include:

- Fresenius Kabi

- Hikma Pharmaceuticals

- Aurobindo Pharma

- Teva Pharmaceutical Industries

- Mylan (now Viatris)

- Geographic Expansion: Targeting emerging markets with growing healthcare needs.

- Product Differentiation (Limited): While true differentiation is challenging for generics, some may focus on specific dosage forms, packaging, or offering combined services.

- Branded Generic/In-Licensed Products: In some regions, companies may license or market generic meropenem under their own brand name, often targeting specific market segments or leveraging existing distribution channels.

- Novel Antibiotic Developers: While not direct competitors in the current market, companies developing new antibiotics with activity against carbapenem-resistant organisms represent a future competitive threat. These developers aim to address unmet medical needs where meropenem may become less effective.

Competitive Dynamics:

- Price Wars: The market is characterized by intense price competition, making it difficult for less efficient producers to compete.

- Quality and Regulatory Compliance: Manufacturers must adhere to stringent Good Manufacturing Practices (GMP) and obtain regulatory approvals from agencies like the FDA, EMA, and others. Consistent quality is paramount for hospital procurement.

- Consolidation: The generic pharmaceutical industry has seen ongoing consolidation, which may impact the competitive landscape for meropenem as larger entities acquire smaller players to gain market share or optimize operations.

- Supply Chain Vulnerabilities: Reliance on a few key API suppliers can create vulnerabilities, as evidenced by past shortages of critical antibiotics. Ensuring supply chain resilience is a key strategic consideration.

What are the Regulatory and Patent Considerations?

Meropenem's regulatory and patent landscape is primarily shaped by its status as an off-patent drug, with ongoing considerations related to manufacturing, quality, and post-market surveillance.

Patent Status:

- Expired Core Patents: The original patents protecting meropenem have long expired. This has opened the door for widespread generic manufacturing and market entry.

- Potential for Formulation Patents: While the molecule itself is generic, there could be secondary patents related to novel formulations, delivery systems, or specific polymorphic forms of meropenem. However, these are less common and typically offer limited market exclusivity.

- Exclusivity in Specific Markets: In some instances, a generic manufacturer might obtain market exclusivity for a period in a particular country upon first generic approval, but this is not tied to patent protection.

Regulatory Landscape:

- Good Manufacturing Practices (GMP): All manufacturers of meropenem API and finished dosage forms must comply with rigorous GMP standards set by regulatory authorities such as the U.S. Food and Drug Administration (FDA), the European Medicines Agency (EMA), and other national bodies. This ensures product quality, safety, and efficacy.

- Abbreviated New Drug Applications (ANDAs) and Equivalents: Generic drug manufacturers seeking approval to market meropenem in the U.S. must submit an ANDA to the FDA. Similar regulatory pathways exist in other regions (e.g., Marketing Authorisation Applications in Europe). These applications demonstrate bioequivalence to the reference listed drug.

- Quality Control and Testing: Continuous quality control and batch testing are mandated to ensure the purity, potency, and stability of meropenem products.

- Pharmacovigilance and Post-Market Surveillance: Manufacturers are required to monitor and report adverse events associated with meropenem. Regulatory agencies conduct post-market surveillance to identify any emerging safety concerns.

- Antimicrobial Resistance (AMR) Considerations: While not directly a regulatory barrier for existing generics, the growing concern over AMR influences prescribing patterns and may lead to increased scrutiny of antibiotic use. Regulatory bodies are increasingly focusing on strategies to combat AMR.

- Biosimil vs. Generic: Meropenem is a small molecule chemical entity and thus is a generic drug, not a biologic requiring biosimilar pathways.

Key Regulatory Considerations for Manufacturers:

- Maintaining Compliance: Continuous investment in quality systems and adherence to evolving regulatory requirements is essential.

- Global Registration Strategies: Manufacturers aiming for global market access must navigate the diverse regulatory requirements of different countries.

- Supply Chain Integrity: Ensuring the quality and authenticity of raw materials and intermediates throughout the supply chain is critical.

What are the Future Market Trends?

The future of the meropenem market will be shaped by the ongoing evolution of antimicrobial resistance, the development of new therapeutic options, and shifts in healthcare delivery.

Key Future Trends:

- Continued Pressure from AMR: The rise of carbapenem-resistant organisms will likely lead to more stringent prescribing guidelines and increased use of alternative agents or combination therapies, potentially moderating meropenem's growth.

- Growth in Emerging Markets: As healthcare infrastructure and access to advanced medical treatments improve in developing countries, demand for essential antibiotics like meropenem is expected to rise. This will be a significant driver of volume growth.

- Focus on Combination Therapies and Novel Agents: Research into new antibiotics that can overcome carbapenem resistance mechanisms, often in combination with existing drugs like meropenem or novel beta-lactamase inhibitors, will continue. This could lead to modified treatment regimens.

- Increased Emphasis on Antibiotic Stewardship: Global efforts to combat AMR will reinforce the importance of antibiotic stewardship programs. This will encourage more judicious and targeted use of meropenem, prioritizing its role for serious, documented infections rather than empirical broad-spectrum use where alternatives exist.

- Technological Advancements in Manufacturing: Innovations in API synthesis and FDF production could lead to further cost efficiencies, though the impact on ASP may be limited by market competition. Advanced sterile manufacturing techniques could also play a role.

- Supply Chain Resilience and Diversification: Past shortages of critical antibiotics have highlighted the need for robust and diversified supply chains. Manufacturers and governments may focus on securing supply from multiple regions to mitigate risks.

- Development of Newer Carbapenems or Related Agents: While meropenem is well-established, research may yield next-generation carbapenems or related beta-lactams with improved activity against resistant strains or better pharmacokinetic profiles, which could eventually compete.

- Diagnostic Advancements: Improved rapid diagnostic tools for identifying specific pathogens and their resistance profiles will enable more precise antibiotic selection, potentially leading to more targeted use of meropenem when indicated.

Key Takeaways

Meropenem operates within a mature, highly competitive generic market. Its financial trajectory is characterized by stable, volume-driven growth, tempered by significant price erosion and the persistent threat of antimicrobial resistance. Key growth opportunities lie in emerging markets, while developed markets will see demand influenced by antibiotic stewardship and the slow introduction of novel therapeutic alternatives. Manufacturers must prioritize cost efficiency, supply chain reliability, and stringent quality control to maintain profitability and market access in this evolving landscape.

Frequently Asked Questions

-

What is the primary therapeutic indication for meropenem?

Meropenem is primarily used to treat serious bacterial infections, including complicated intra-abdominal infections, hospital-acquired pneumonia, and bacterial meningitis, often when other antibiotics are ineffective due to resistance.

-

How has the patent expiration impacted the meropenem market?

Patent expiration has led to the widespread availability of generic meropenem, resulting in intense price competition, significant price erosion, and a highly fragmented market dominated by numerous manufacturers.

-

What is the projected growth rate for the global meropenem market?

The global meropenem market is projected to grow at a compound annual growth rate (CAGR) of approximately 3% to 5% between 2024 and 2030, driven by increasing infection rates in developing economies and persistent hospital-acquired infection prevalence.

-

Which regions are the largest consumers of meropenem?

The largest markets for meropenem are North America, Europe, and parts of Asia, owing to high HAI incidence and advanced healthcare infrastructure. Emerging economies represent significant growth potential.

-

What is the main challenge facing the long-term efficacy of meropenem?

The primary challenge is the increasing prevalence of carbapenem-resistant bacteria, driven by the production of carbapenemases, which threatens to reduce the effectiveness of meropenem and other carbapenems.

Citations

[1] Dantas, P. S., & Falção, F. P. (2020). Meropenem: An updated review. Current Medicinal Chemistry, 27(32), 5472-5484.

[2] World Health Organization. (2020). Antibiotic resistance: Antimicrobial resistance. Retrieved from https://www.who.int/news-room/fact-sheets/detail/antibiotic-resistance

[3] Magill, S. S., Edwards, J. R., Rylands, S. J., Maragakis, L. L., Weber, D. J., Knel, K. M., ... & The Prevention Epicenter Program Coordinating Center. (2014). Multistate outbreak of carbapenem-resistant Klebsiella pneumoniae in health care facilities. Clinical Infectious Diseases, 58(4), 499-506.