Last updated: February 19, 2026

Fluocinonide, a potent topical corticosteroid, demonstrates stable market presence driven by established therapeutic applications and ongoing generic competition. The drug is primarily indicated for the relief of inflammatory and pruritic manifestations of corticosteroid-responsive dermatoses. Its market trajectory is characterized by consistent demand, patent expiries, and the introduction of bioequivalent generic formulations, impacting pricing and revenue streams for originators.

What is the current market size and projected growth for fluocinonide?

The global market for topical corticosteroids, including fluocinonide, is substantial. While specific fluocinonide market size figures are often aggregated within broader corticosteroid or dermatological drug categories, industry analysis indicates a steady demand. For instance, the global topical corticosteroids market was valued at approximately $3.5 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 4% to 5% through 2030, reaching an estimated $4.8 billion [1]. Fluocinonide, as a mid-to-high potency corticosteroid, occupies a significant segment within this market due to its efficacy in treating moderate to severe inflammatory skin conditions.

The growth drivers for fluocinonide are intrinsically linked to the increasing prevalence of dermatological disorders such as eczema, psoriasis, and dermatitis. Factors contributing to this rise include environmental changes, stress, and an aging global population, all of which are associated with a higher incidence of skin conditions requiring topical corticosteroid treatment [2].

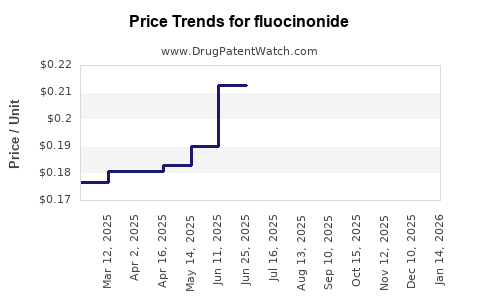

However, the market growth for fluocinonide is tempered by several factors. The primary constraint is the patent expiry of originator products, leading to widespread genericization. Generic fluocinonide formulations are available at significantly lower price points, increasing accessibility but reducing revenue for original manufacturers. Furthermore, ongoing research into alternative therapeutic modalities for dermatological conditions, including biologics and novel small molecules, presents a long-term competitive threat. Despite these challenges, the established safety profile, cost-effectiveness, and broad applicability of fluocinonide ensure its continued relevance and market share.

What is the patent landscape for fluocinonide and its implications?

The original patents covering the composition of matter and primary methods of use for fluocinonide have long since expired. The foundational patent for fluocinonide, US Patent 3,577,428, was filed in 1967 and granted in 1971 [3]. This early expiration means that the core intellectual property protection has been unavailable for decades.

Consequently, the fluocinonide market is dominated by generic manufacturers. The absence of strong patent protection on the active pharmaceutical ingredient (API) allows multiple companies to produce and market fluocinonide formulations. This competitive environment leads to price erosion, as generic versions vie for market share based on cost and availability.

While the core patents have expired, pharmaceutical companies may have sought and obtained patents for specific aspects of fluocinonide, such as:

- Novel Formulations: Patents might cover specific delivery systems, such as improved creams, ointments, gels, or foams that enhance skin penetration, reduce systemic absorption, or improve patient compliance. For example, a patent might claim a unique emulsification system or a controlled-release mechanism [4].

- Manufacturing Processes: Innovative or more efficient methods for synthesizing fluocinonide or preparing its formulations could be patented. These patents focus on the process itself rather than the molecule.

- New Indications or Combinations: While less common for older drugs, companies could potentially patent novel uses for fluocinonide in combination with other APIs for specific dermatological conditions, provided there is a demonstrated synergistic effect or unexpected benefit [5].

The implication of this patent landscape is a highly competitive generic market. Originator companies that once held market exclusivity have seen their revenue streams significantly diminished following patent expiries. For generic manufacturers, the barrier to entry is relatively low, leading to a crowded marketplace. The financial trajectory for new fluocinonide-specific patents is therefore limited, primarily focusing on incremental improvements or niche applications rather than broad market dominance. Investment in developing entirely new fluocinonide-based drugs is unlikely given the availability of off-patent formulations. The focus for companies in this space is on cost-effective manufacturing, efficient supply chain management, and market penetration through competitive pricing strategies.

Who are the key players and what is their market share in the fluocinonide market?

The fluocinonide market is characterized by a fragmented landscape with numerous generic manufacturers and distributors. The absence of active originator patent protection means that market share is not concentrated around a single entity but rather distributed among several companies that specialize in generic dermatological products.

Key players in the broader topical corticosteroid market that also manufacture or distribute fluocinonide include:

- Teva Pharmaceutical Industries Ltd.: A leading global generic pharmaceutical company with a broad portfolio of dermatological products.

- Sun Pharmaceutical Industries Ltd.: Another major player in the generic space, with significant presence in dermatology.

- Mylan N.V. (now Viatris): A well-established generic and specialty pharmaceuticals company that has historically offered fluocinonide formulations.

- Bausch Health Companies Inc.: Known for its dermatology division, offering various topical treatments.

- Perrigo Company plc: A significant provider of over-the-counter (OTC) and generic prescription products.

Beyond these large multinational corporations, numerous smaller and regional generic manufacturers also contribute to the fluocinonide supply chain. These companies often compete intensely on price and distribution reach.

Determining precise market share for fluocinonide specifically is challenging as it is often reported within broader therapeutic classes like "corticosteroids" or "dermatology generics." However, analysis of prescription data and market reports indicates that companies with strong generic portfolios and extensive distribution networks tend to hold larger shares. For example, data from IQVIA or other market intelligence firms would show that Teva and Sun Pharma consistently rank among the top suppliers of generic topical corticosteroids in major markets like the United States and Europe [6].

The market share dynamics are subject to change based on:

- Manufacturing Costs and Efficiency: Companies with superior cost structures can offer more competitive pricing, thereby gaining market share.

- Regulatory Approvals andANDA Filings: The speed at which companies can secure Abbreviated New Drug Application (ANDA) approvals for generic fluocinonide can impact their market entry and initial share.

- Distribution Agreements and Payer Contracts: Securing favorable contracts with wholesalers, pharmacies, and insurance providers is critical for market access and volume.

- Product Quality and Reliability: Consistent product quality and a reliable supply chain are essential for maintaining customer loyalty and market position.

The financial trajectory for these players in the fluocinonide segment is largely dictated by volume sales rather than premium pricing. Profitability is achieved through economies of scale and efficient operations.

What are the key therapeutic indications and formulations of fluocinonide?

Fluocinonide is a synthetic corticosteroid that functions as an anti-inflammatory, antipruritic, and vasoconstrictive agent. Its primary therapeutic indications are for the relief of inflammatory and pruritic manifestations of corticosteroid-responsive dermatoses. These conditions include, but are not limited to:

- Eczema (Dermatitis): Various forms, including atopic dermatitis, contact dermatitis, and nummular dermatitis.

- Psoriasis: Certain localized forms of plaque psoriasis.

- Seborrheic Dermatitis: Particularly when inflammation is prominent.

- Lichen Planus: Inflammatory condition affecting skin and mucous membranes.

- Discoid Lupus Erythematosus: A chronic autoimmune skin condition.

- Allergic Reactions: Severe cases of allergic contact dermatitis.

- Insect Bites: To reduce inflammation and itching.

Fluocinonide is available in various topical formulations to cater to different skin types, lesion locations, and patient preferences. The potency of fluocinonide is classified as Class II or III (super high to high potency) depending on the specific formulation and concentration, indicating its strength for treating moderate to severe skin conditions [7]. Common formulations include:

- Ointments: Typically contain a higher oil content (e.g., petrolatum-based), making them occlusive and effective for dry, thickened, or scaly skin lesions. They provide good penetration and hydration. Standard concentrations are usually 0.05% w/w. Examples include Fluocinonide Ointment USP 0.05%.

- Creams: Water-based emulsions with a balance of oil and water. They are less greasy than ointments and are suitable for weeping or oozing lesions, as well as for application to less dry skin areas. Standard concentrations are usually 0.05% w/w. Examples include Fluocinonide Cream USP 0.05%.

- Gels: Water-based, non-greasy formulations that dry quickly and are preferred for hairy areas (e.g., scalp) or for patients who find ointments or creams too heavy. They can also provide a cooling sensation. Standard concentrations are usually 0.05% w/w. Examples include Fluocinonide Gel USP 0.05%.

- Solutions: Typically alcohol-based, these are also suitable for application to hairy areas and can be effective for scalp conditions like psoriasis or seborrheic dermatitis. Standard concentrations are usually 0.05% w/w. Examples include Fluocinonide Solution USP 0.05%.

The choice of formulation is critical for therapeutic efficacy and patient adherence. For example, a physician might prescribe an ointment for chronic, dry eczema on the arms, while a gel or solution might be preferred for acute, inflamed dermatitis on the scalp.

The financial trajectory for these formulations is primarily driven by demand from dermatologists and primary care physicians prescribing them. Generic versions of these formulations are widely available and compete on price. The overall demand is stable, reflecting the persistent need for effective topical anti-inflammatory treatments for common dermatological conditions. The development of novel fluocinonide formulations, if any, would likely focus on enhanced delivery, improved cosmetic profiles, or combination therapies, potentially commanding a higher price point but facing scrutiny regarding cost-effectiveness against established generics.

What is the global regulatory environment impacting fluocinonide?

The global regulatory environment for fluocinonide is governed by national and regional health authorities. Given that fluocinonide is a well-established pharmaceutical ingredient, its regulation primarily focuses on:

- Generic Drug Approval: In countries like the United States, the Food and Drug Administration (FDA) reviews Abbreviated New Drug Applications (ANDAs) for generic fluocinonide. Manufacturers must demonstrate bioequivalence to an approved reference listed drug (RLD), meaning the generic product performs comparably to the innovator product in terms of rate and extent of absorption [8]. The FDA also ensures that generic drug manufacturing facilities adhere to Good Manufacturing Practices (GMP).

- Labeling and Prescribing Information: Regulatory bodies mandate that labeling and prescribing information (package inserts) for fluocinonide products accurately reflect its indications, contraindications, warnings, precautions, adverse reactions, and dosage. This information is crucial for safe and effective use.

- Post-Market Surveillance: Authorities monitor the safety and efficacy of fluocinonide products after they enter the market. This includes tracking adverse event reports, investigating product quality issues, and potentially issuing recalls if safety concerns arise.

- International Harmonization: Efforts towards international harmonization of pharmaceutical regulations, such as through the International Council for Harmonisation of Technical Requirements for Pharmaceuticals for Human Use (ICH), influence regulatory standards globally. This means that manufacturing, quality control, and documentation requirements are often aligned across major regulatory agencies like the FDA, European Medicines Agency (EMA), and Pharmaceuticals and Medical Devices Agency (PMDA) in Japan [9].

Specific Regulatory Considerations:

- European Union: In the EU, fluocinonide products require marketing authorization from either the EMA or national competent authorities. The process for generic applications in the EU is similar to that in the US, requiring demonstration of pharmaceutical equivalence and bioequivalence [10].

- Other Regions: Regulatory requirements in countries like Canada, Australia, Brazil, and India vary but generally follow similar principles of demonstrating safety, efficacy, and quality for generic drug approval.

The financial trajectory of fluocinonide manufacturers is influenced by the cost and time associated with navigating these regulatory pathways. The rigorous approval process for ANDAs and marketing authorizations represents a significant investment. However, once approved, the established nature of fluocinonide means that regulatory hurdles are generally predictable, and the market is largely mature. The absence of new patent protection means that competition is primarily driven by manufacturing efficiency and speed to market for generic approvals, rather than by obtaining new regulatory exclusivities for the API itself. Any new intellectual property, such as for novel formulations, would require its own regulatory review and approval process.

What is the competitive landscape and potential threats to fluocinonide?

The competitive landscape for fluocinonide is characterized by intense rivalry among generic manufacturers and a growing array of alternative treatments for dermatological conditions.

Key Competitive Dynamics:

- Generic Erosion: The primary competitive force is the widespread availability of low-cost generic fluocinonide. This has led to significant price compression, limiting profitability for any single manufacturer. Market share is gained and maintained through volume, cost efficiency, and distribution strength.

- Other Topical Corticosteroids: Fluocinonide competes with a vast array of other topical corticosteroids of varying potencies, including hydrocortisone (low potency), triamcinolone acetonide (medium potency), and clobetasol propionate (super high potency). Prescribers select these based on the severity and location of the skin condition, creating a direct competitive overlap.

- Non-Steroidal Anti-Inflammatory Agents: Topical calcineurin inhibitors (e.g., tacrolimus, pimecrolimus) and phosphodiesterase-4 (PDE4) inhibitors (e.g., crisaborole) offer alternative non-steroidal treatment options, particularly for patients who require long-term treatment or have contraindications to corticosteroids [11].

- Biologics and Systemic Therapies: For severe and refractory dermatological conditions like psoriasis and atopic dermatitis, advanced treatments such as monoclonal antibodies (e.g., adalimumab, secukinumab) and oral small molecule inhibitors (e.g., JAK inhibitors) are increasingly employed. While not direct competitors for mild to moderate cases treated by topical fluocinonide, they represent a shift in treatment paradigms for more severe disease, potentially reducing the incidence of severe cases requiring potent topical therapy.

- New Dermatological Treatments: Ongoing research and development in dermatology continuously introduce novel therapies, including new small molecules, gene therapies, and advanced topical formulations, which could displace older treatments.

Potential Threats:

- Increasingly Stringent Safety Monitoring: As regulatory bodies enhance pharmacovigilance, any identified long-term safety concerns associated with topical corticosteroids, even if theoretical or rare, could lead to more restrictive prescribing guidelines or warnings, impacting demand.

- Physician and Patient Preference Shifts: A growing preference among some physicians and patients for non-steroidal treatments due to concerns about the long-term side effects of corticosteroids (e.g., skin thinning, striae, hypothalamic-pituitary-adrenal axis suppression with extensive use) could lead to a gradual decline in fluocinonide prescription volume.

- Reimbursement Pressures: Payers and healthcare systems may increasingly favor lower-cost generic options or non-steroidal alternatives when deemed clinically appropriate, impacting the reimbursement landscape for fluocinonide.

- Advancements in Supportive Care: Improved patient education and lifestyle management strategies for dermatological conditions could reduce the reliance on pharmacological interventions for milder cases.

The financial trajectory for fluocinonide is therefore one of sustained, albeit modest, demand within its established niche, continually challenged by price competition and the evolution of therapeutic alternatives.

What is the financial trajectory of fluocinonide sales and profitability?

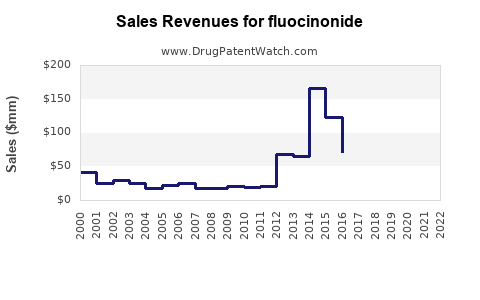

The financial trajectory of fluocinonide sales is characterized by a mature, stable revenue stream primarily driven by generic volume. The era of blockbuster sales associated with originator exclusivity is long past due to patent expiry.

Sales Trajectory:

- Stable Demand: Fluocinonide continues to be widely prescribed for its established efficacy in treating various inflammatory skin conditions. The prevalence of these conditions ensures a consistent demand for effective topical treatments.

- Price Erosion: The competitive generic market leads to significant price erosion. While the volume of prescriptions may remain stable or see incremental growth, the revenue generated per prescription has declined substantially over the years.

- Volume-Driven Revenue: The financial success for manufacturers and distributors of fluocinonide is almost entirely dependent on achieving high sales volumes. This necessitates efficient manufacturing, robust distribution networks, and aggressive pricing strategies.

- Limited Growth Potential: Significant growth in overall fluocinonide sales revenue is unlikely. Any increase in revenue will primarily stem from increased prescription volumes driven by dermatological condition prevalence or market penetration gains by specific generic manufacturers, rather than from price increases or market expansion into new, high-value indications.

Profitability:

- Low Margin, High Volume Model: Profitability for fluocinonide products operates on a low-margin, high-volume model. Gross profit margins per unit are typically modest.

- Manufacturing Efficiency is Key: Companies with highly efficient manufacturing processes, low overheads, and streamlined supply chains are best positioned to achieve profitability. Economies of scale are crucial for cost-competitiveness.

- Distribution and Payer Access: Securing favorable distribution agreements and favorable formulary placement with insurance providers is critical. This can ensure consistent access to a broad patient base, thereby driving necessary sales volumes.

- Generic Competition Impact: The constant pressure from competing generic manufacturers offering similar products at lower prices forces continuous cost optimization and price adjustments. This limits the profit potential for individual companies.

- R&D Investment Context: Investment in developing new fluocinonide-specific innovations is limited. Any R&D is likely focused on process improvements for cost reduction or perhaps novel formulations that may offer a slight competitive edge or be eligible for niche patent protection, but these are unlikely to lead to substantial profit windfalls compared to novel drug development.

Overall Financial Outlook:

The financial outlook for fluocinonide is one of continued steady, predictable revenue generation, rather than high growth or profitability. Companies involved in the fluocinonide market are likely to see this product as a consistent contributor to their overall portfolio, providing stable cash flow from established demand. The financial success hinges on operational excellence and market access in a highly competitive generic environment. Long-term profitability will depend on maintaining cost leadership and supply chain reliability.

Key Takeaways

- Fluocinonide's market is stable, driven by consistent demand for treating inflammatory dermatoses, with projected growth aligned with the broader topical corticosteroid market.

- Original patents for fluocinonide have expired, leading to a market dominated by generic manufacturers, characterized by price competition and limited originator profit potential.

- Key players are predominantly large generic pharmaceutical companies such as Teva, Sun Pharma, and Viatris, with market share determined by manufacturing efficiency and distribution reach.

- Fluocinonide is available in multiple formulations (ointments, creams, gels, solutions) at 0.05% concentration for treating conditions like eczema and psoriasis.

- The global regulatory environment focuses on generic drug approval, labeling, and post-market surveillance, with adherence to GMP standards being critical.

- Competitive threats include other topical corticosteroids, non-steroidal alternatives, advanced systemic therapies, and potential shifts in physician/patient preferences towards non-steroidal treatments.

- The financial trajectory for fluocinonide is one of stable, volume-driven revenue with modest profitability due to price erosion and intense generic competition, necessitating a low-margin, high-volume business model.

FAQs

-

Are there any new patents for fluocinonide being filed that could impact its market exclusivity?

While the original composition of matter patents have expired, new patents may be filed for novel formulations, improved delivery systems, manufacturing processes, or specific combination therapies involving fluocinonide. However, these are unlikely to grant broad market exclusivity comparable to early innovator patents.

-

What is the primary reason for the low pricing of fluocinonide products?

The primary reason for low pricing is the expiration of all foundational patents, allowing numerous generic manufacturers to produce and sell the drug, leading to intense price competition.

-

How does fluocinonide compare in potency to other common topical corticosteroids?

Fluocinonide is generally classified as a Class II or III (super high to high potency) corticosteroid, making it suitable for treating moderate to severe inflammatory skin conditions. This places it among the more potent topical steroids available.

-

What are the main long-term side effects associated with the use of fluocinonide?

Long-term side effects associated with potent topical corticosteroids like fluocinonide can include skin thinning (atrophy), striae (stretch marks), telangiectasias (spider veins), and potential hypothalamic-pituitary-adrenal (HPA) axis suppression if applied extensively over large body surface areas or under occlusion for prolonged periods.

-

Can fluocinonide be purchased over-the-counter (OTC) or is it strictly a prescription medication?

In most major markets, including the United States, fluocinonide is classified as a prescription-only medication. Lower potency corticosteroids like hydrocortisone are more commonly available OTC.

Citations

[1] Global Market Insights. (2023). Topical Corticosteroids Market Size, Share & Trends Analysis Report.

[2] Market Research Future. (2023). Dermatological Drugs Market.

[3] U.S. Patent and Trademark Office. (1971). U.S. Patent 3,577,428.

[4] Pharmaceutical Technology. (2022). Advancements in Topical Drug Delivery Systems.

[5] Journal of the American Academy of Dermatology. (2021). Combination Therapies in Dermatologic Treatment.

[6] IQVIA. (2023). Global Pharmaceutical Market Insights. (Data accessed through proprietary analytics platforms).

[7] U.S. Food & Drug Administration. (n.d.). Topical Corticosteroids: Potency Classification.

[8] U.S. Food & Drug Administration. (2020). Guidance for Industry: ANDAs — How to File.

[9] International Council for Harmonisation of Technical Requirements for Pharmaceuticals for Human Use. (n.d.). About ICH.

[10] European Medicines Agency. (n.d.). Generic medicines.

[11] Eczema Society of Canada. (2023). Treatment Options for Eczema.