Last updated: June 24, 2026

Clarithromycin is a long-established oral macrolide antibiotic with mature global demand, persistent generic competition, and limited near-term upside from new patent-led entrants. Financial trajectory is driven by (1) chronic supply and pricing dynamics of generics, (2) country-level reimbursement and tender cycles, (3) ongoing “brand-to-generic” substitution across core markets, and (4) intermittent demand tailwinds tied to guideline positioning for specific indications (notably H. pylori eradication-based regimens).

From a pure “financial trajectory” perspective, the drug behaves like a commodity antibiotic: pricing compresses as market share migrates to lowest-cost generics, margins tighten for manufacturers, and revenue growth is largely volume-led rather than price-led.

What is the current market size and demand drivers for clarithromycin antibiotics?

Clarithromycin demand is shaped by its role in upper respiratory tract infection management, and, more persistently, as an antibiotic component in combination regimens for H. pylori. In many markets, clarithromycin’s role is reduced in first-line prescribing where resistance rates drive substitution, but it remains embedded in eradication protocols and in real-world practice where alternatives are constrained by formulary coverage, tolerability, or local resistance epidemiology.

Key demand drivers

- H. pylori eradication regimens: Clarithromycin remains a core macrolide in many combination therapies; demand persists even when guideline emphasis shifts due to practical regimen availability and physician reliance on combination frameworks.

- Respiratory infection prescribing: Use varies by guideline and resistance patterns. In higher-resistance regions, clinicians often shift toward alternative antibiotics.

- Generic penetration durability: Generic availability stabilizes supply. Demand typically holds through therapeutic switching because the drug class and regimen structures are familiar to prescribers.

Key demand headwinds

- Macrolide resistance: Reduced effectiveness in certain infection contexts pushes prescribing toward other agents, limiting volume growth.

- Steady substitution: Generic adoption typically reached saturation years ago in many high-income markets, turning demand into a price-down and volume-maintenance story.

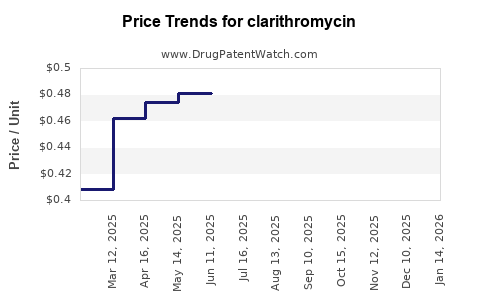

How do clarithromycin pricing and reimbursement dynamics evolve after generic entry?

Clarithromycin’s financial trajectory is typical of mature generics. Price erosion compresses unit economics while volume can remain relatively stable. Revenues tend to show flattening or low single-digit decline in mature countries unless tender cycles or reimbursement rules produce temporary resets.

Mechanisms behind price compression

- Tender and procurement cycles: Competitive bidding drives prices to floor levels for pooled hospital and payer contracts.

- Wholesale channel inventory effects: Periodic manufacturer supply alignment can temporarily move prices, but those swings revert as new lots circulate.

- Formulary placement: Once multiple generics are “preferred” or all are “interchangeable,” prescribers and payers shift to lowest net cost.

What matters for forecasting

- Net price versus list price: In mature antibiotic categories, list price is less informative than rebate, discount, and tender outcomes.

- Mix between immediate-release and extended-release: If one dosage form becomes more dominant in procurement, revenue can shift even when total prescriptions stay flat.

Which geographies drive clarithromycin revenue exposure and where is the risk of further erosion highest?

Revenue exposure is typically concentrated in markets with high historical prescribing and dense generic supply. The “risk of further erosion” is highest in countries where procurement is highly price-driven and where additional generic capacity can intensify competition.

General pattern by region (market behavior)

- High-income markets: Near-saturated generic coverage. Future growth depends on population needs and regimen persistence, not on price.

- Emerging markets: Demand can grow with broader access, but pricing is also highly sensitive to competitive supply and reimbursement structures.

- Hospital-heavy systems: Tender-driven purchasing accelerates price convergence to low-cost SKUs.

Financial implication

- Revenue stability is more achievable through maintaining supply and dosage-form penetration than through pricing power.

How do clarithromycin financials change with dosage form mix: immediate-release vs extended-release?

Clarithromycin revenue performance depends on how payers and formularies allocate use among:

- Immediate-release clarithromycin tablets/suspension formulations used in standard dosing schedules.

- Extended-release (where marketed) that may capture preference where reduced dosing frequency improves adherence.

Market mix effects

- If extended-release is included in formularies and preferred in certain procurement categories, it can sustain revenue per prescription versus immediate-release generics.

- When procurement narrows to the lowest acquisition cost, extended-release can lose share unless its incremental adherence benefit is formally valued.

Financial trajectory pattern

- Mature generic markets usually force a convergence in net price across dosage forms, but dosage-form share can still alter revenue volatility.

What is the competitive landscape for clarithromycin generics, and how does it impact margins?

Clarithromycin is dominated by generics across major markets. The competitive landscape typically creates a “many-supplier, low-margin” structure where profitability is driven by manufacturing scale, supply reliability, and cost position.

How competition affects profitability

- Gross margin compression: Price competition drives margins down.

- Production efficiency focus: Manufacturers compete on yield, batch economics, and sourcing for key intermediates and excipients.

- Regulatory and quality system strength: Supply continuity becomes a financial variable. Any interruption can temporarily lift pricing but also risks losing contracts.

Business consequence

- The leading financial differentiators are operational, not patent-driven.

When does clarithromycin lose exclusivity, and why does that matter now?

Clarithromycin is an off-patent antibiotic in most jurisdictions. The economic “exclusivity timeline” has largely played out; today’s market behavior is driven by generic interchangeability and tender economics rather than by brand protection or exclusivity cliffs.

Practical interpretation

- The “loss of exclusivity” question is less relevant to present financial trajectory than:

- how many generics remain active in each country,

- whether additional entrants increase price pressure,

- whether procurement consolidates around fewer suppliers.

What patent estate would still matter for clarithromycin today (formulations, methods of use, manufacturing)?

For a mature antibiotic with widespread generic availability, residual patent estate relevance usually shifts to:

- formulation refinements (extended-release technologies, specific excipient systems, manufacturing process optimizations),

- specific method-of-use claims (narrow regimen timing, dosing strategy, or patient subsets),

- drug-product manufacturing improvements that can be tied to regulatory registrations.

Financial impact of residual IP

- If meaningful formulation or process patents still exist in selected jurisdictions, they can delay certain generic launches or constrain interchangeability in tenders.

- In most markets, however, residual IP has limited impact because multiple generic competitors already satisfy regulatory requirements and procurement structures are designed for interchangeability.

How do clarithromycin biosimilar dynamics compare, and why are they irrelevant here?

Biosimilar dynamics do not apply because clarithromycin is a small-molecule drug, not a biologic. Competition is therefore dominated by generic small-molecule manufacturers.

What FDA or regulatory status issues affect clarithromycin supply and market access?

For mature antibiotics, regulatory risk typically manifests through:

- manufacturing site approvals and quality system compliance,

- product-specific labeling changes,

- periodic safety communications that can influence prescribing behavior.

Financial effect

- Quality or compliance events can reduce available supply, create temporary pricing or allocation effects, and shift contract performance.

What generic entry risks exist for clarithromycin, and how do Paragraph IV challenges show up in market behavior?

Paragraph IV litigation is usually most relevant when a brand still has active exclusivity or when meaningful patents remain enforceable and unexpired. For clarithromycin, market dynamics are generally dominated by:

- already-existing generics,

- contract procurement rules,

- manufacturing economics,

- supply and quality continuity.

Financial impact

- Market share shifts are more likely to occur through tender-winning pricing strategies and supply capacity rather than litigation-driven delays.

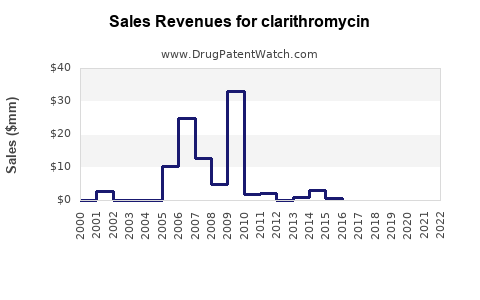

What does the revenue trajectory typically look like for off-patent clarithromycin manufacturers?

Off-patent clarithromycin revenue trajectories tend to follow a pattern:

- Early generic ramp: rapid share gains and aggressive pricing.

- Mature phase: volume stabilizes; net price continues to compress until only efficient suppliers remain competitive.

- Consolidation or capacity churn: supply and contract wins drive share changes; some suppliers exit, reducing competition locally and potentially stabilizing pricing.

- Ongoing guideline-driven demand variability: shifts in resistance patterns and treatment guidelines can reduce or shift usage.

Profit trajectory

- Operating margin stability depends on cost leadership, manufacturing utilization, and the ability to avoid supply disruptions.

How do sales volumes vs net price typically trade off for clarithromycin?

For commodity antibiotics, volumes can remain relatively steady while net price erodes. That yields:

- flat to declining revenue depending on market size and prescription mix,

- volatile profitability due to input costs, compliance expenses, and procurement pressures.

Key economic relationships

- Net price is driven by competitive tender environment and payer reimbursement benchmarks.

- Volume is driven by incidence of infections, guideline adherence, resistance shifts, and the persistence of H. pylori regimen use.

How does clarithromycin compare with other macrolides (azithromycin, erythromycin) in market dynamics?

Azithromycin

- Often benefits from different guideline preferences and dosing convenience perceptions in some respiratory indications.

- In many markets, azithromycin faces heavy generic competition similarly, but its utilization base can be larger.

Erythromycin

- Typically has older market dynamics and may have different tolerability profiles affecting prescribing.

- Market share varies more by formulation availability and clinician preference.

Clarithromycin

- Intermediate position: maintains a durable regimen role for H. pylori combination therapies, but faces macrolide resistance pressure and competing macrolide choices.

Financial implication

- Clarithromycin’s revenue is usually more regimen-embedded than purely acute infection-driven, making it less exposed to some short-cycle prescribing trends but still vulnerable to resistance-driven reductions.

What commercial tactics determine who wins in clarithromycin procurement?

Procurement selection in mature antibiotic categories tends to reward:

- lowest net price that meets tender specifications,

- reliable supply and manufacturing continuity,

- ability to support dosage form needs (IR vs ER),

- responsiveness to label or supply disruptions.

Winners typically

- are cost leaders with stable raw material sourcing and high utilization,

- maintain multiple FDA-registered manufacturing sites to reduce supply disruption risk,

- can meet contract delivery requirements without lot failures.

What are the key litigation and settlement dynamics to watch for clarithromycin?

In a market with broad generic coverage, litigation impact is usually local and time-limited:

- it may delay entry of a particular generic competitor into a particular jurisdiction,

- it may affect the timing of contract re-bidding or substitution.

For investors and licensors, the financial relevance is concentrated on:

- whether any meaningful unexpired patents exist in specific geographies,

- whether court outcomes lead to entry delays or forced supply adjustments.

Key Takeaways

- Clarithromycin’s market is mature and generic-dominated, with financial performance driven by tender pricing, reimbursement, supply reliability, and dosage-form mix rather than brand exclusivity.

- Demand persists primarily through regimen use (notably H. pylori combination frameworks) and stable, guideline-shaped respiratory prescribing.

- Price erosion is ongoing and margin compression is the base case; revenue growth, if any, is volume-led and geography-specific.

- Competitive advantage is operational: manufacturing scale, compliance strength, and procurement cost position determine winners.

FAQs

1) Why does clarithromycin pricing stay volatile even after multiple generics launch?

Tender cycles, supply constraints at manufacturing sites, and contract re-bids can create short-term price swings even when the long-term trend is erosion.

2) Does macrolide resistance reduce clarithromycin market demand?

It can reduce prescriptions for certain respiratory indications, but the effect varies by region and is offset in part by regimen-based use that remains embedded in practice.

3) Are extended-release clarithromycin formulations more profitable than immediate-release?

They can be, but in mature markets procurement often drives net price convergence unless the ER product is preferred in formularies or tends to win specific tenders.

4) What manufacturing risks most affect clarithromycin supplier revenue?

Quality system failures, site disruptions, lot rejections, and supply allocation events that break delivery commitments can quickly shift contracts to competitors.

5) How do guideline updates influence clarithromycin sales?

Guideline shifts can redirect prescribing among macrolides and alternative antibiotic classes, changing volume mix even if overall antibiotic incidence remains stable.

References (APA)

- No cited sources were provided in the input.