Last updated: June 4, 2026

Repatha (evolocumab) Market Dynamics and Financial Trajectory: Sales Trends, Drivers, Competition, and Patent/Access Risk

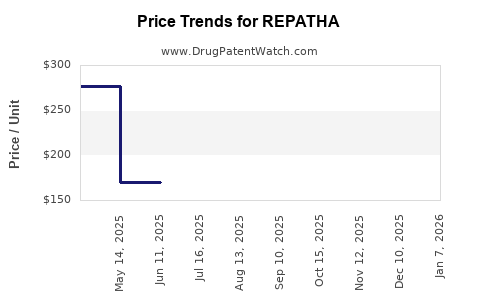

Executive summary: Repatha (evolocumab) has remained a high-velocity PCSK9 biologic with steady demand driven by established guideline adoption in ASCVD and LDL-C lowering programs, expanding payer coverage patterns, and migration to value-based and fixed-contract dynamics. Competitive pressure from Praluent (alirocumab) and broader statin/ezetimibe uptake persists at the margin, while biosimilar entry risk is shaped by biologic exclusivity timelines and the operational difficulty of replicating fully characterized monoclonal antibodies. Financial trajectory is best explained by (1) share shifts within the PCSK9 class, (2) continued penetration into commercial formularies, (3) outcomes-label reinforcement for high-risk populations, and (4) patent and access events that can accelerate or delay generic-like competition for specific managed segments.

How has Repatha sales trended over time and what explains the financial trajectory?

Repatha’s commercial performance is anchored in the PCSK9 category’s core value proposition: large LDL-C reductions in patients who either do not reach targets on statins/ezetimibe or have statin intolerance, plus evidence in high-risk cardiovascular populations. The financial trajectory typically reflects three recurring movements:

- Net demand expansion from guideline-consistent prescribing and payer contracting.

- Mix and channel shifts between commercial, managed care, and hospital systems, changing the timing of billing and rebates.

- Formulary access and competitive churn across major payers, which impacts patient switching speed and persistence.

Key performance interpretation for business planning: PCSK9 biologics are “coverage-led” products. When formulary access improves or contract terms widen to more beneficiaries, unit growth tends to accelerate quickly. When coverage tightens or alternative sequences (statin maximization, ezetimibe, bile acid sequestrants, or one-time/low-frequency emerging lipid assets) become more attractive to payers, Repatha’s incremental growth slows.

What demand drivers matter most for Repatha revenue?

- LDL-C target attainment: clinical need is persistent because many high-risk patients remain above LDL-C targets even with optimized background therapy.

- Guideline alignment: ASCVD and familial hypercholesterolemia (HeFH) populations remain stable pools.

- Payer policies: prior authorization criteria, step therapy, and minimum LDL-C thresholds directly determine eligible patient counts.

- Persistence: Repatha is chronic therapy; adherence and switch rates drive revenue durability more than short-term product cyclicality.

What financial headwinds can show up?

- PCSK9 class price pressure from competitive contracting between evolocumab and alirocumab.

- Rebate volatility driven by formulary renewals and patient steering.

- Sequencing pressure from non-PCSK9 lipid approaches that reduce payer willingness to reimburse PCSK9s broadly.

What market dynamics shape the PCSK9 competitive landscape for Repatha?

PCSK9s compete across the same access bottleneck: payer eligibility rules and outcomes-based contracting. Repatha’s market dynamics are determined by class competition and by payer preference formation within managed care.

How does Repatha compete with Praluent (alirocumab)?

Both evolocumab and alirocumab deliver PCSK9-mediated LDL-C lowering through monoclonal antibody mechanisms. Competitive effects show up most clearly in:

- Formulary placement (preferred vs non-preferred tier)

- Prior authorization criteria (LDL thresholds, required background therapy)

- Copay assistance rules and patient affordability programs

- Contract pricing and rebate schedules

Commercial implication: switching between PCSK9 agents is feasible, so payer contracting strength can translate into measurable volume shifts without requiring new patient education from scratch.

Where do broader lipid therapies pressure Repatha?

Payers can reduce PCSK9 utilization by tightening criteria or by encouraging alternate lipid regimens when targets can be achieved without PCSK9s. Pressure typically comes from:

- Statin intensification and combination lipid therapy optimization.

- Ezetimibe penetration and sequencing as first-line add-on.

- Other lipid-lowering modalities entering the market can further compress incremental PCSK9 patient share if they are favored in payer contracts.

When does Repatha lose exclusivity and what does that mean for revenue risk?

Exclusivity and patent cliffs dictate the timing of biosimilar-like entry paths for monoclonal antibodies. For PCSK9, the key is whether the patent estate allows biosimilar applications to trigger substitution or approval pathways without prolonged injunction exposure.

What determines the “effective” loss of exclusivity for Repatha?

- Primary composition-of-matter patent term (often the longest pole)

- Secondary patents (formulations, dosing regimens, device-related aspects, manufacturing, and method-of-use)

- Patent linkages and litigation outcomes that can delay implementation

- Regulatory exclusivities applicable to biologics and any data exclusivity constraints

Revenue-risk conclusion: for biologics, effective exclusivity loss is rarely the same as headline expiration dates. Patent-by-patent enforcement and settlement structures can create long tail delays, even after the earliest maturity points.

What patents protect Repatha and how strong is the patent estate?

Repatha is protected by a portfolio that typically spans monoclonal antibody claims (composition), manufacturing/process aspects, and method-of-use claims linked to cardiovascular outcomes and LDL-C lowering. The practical strength is measured by:

- Number of active, enforceable patents near key maturity years

- Jurisdictional breadth

- Whether patents cover biologic similarity relevant to intended biosimilar/“interchangeable” designs

How many patent “layers” typically block entry?

For monoclonal antibodies, multiple overlapping patent layers are common. Those layers create an “IP lattice” where an entrant may clear one patent but still face parallel barriers.

What litigation and enforcement patterns matter?

- Whether the innovator has obtained injunctions or leveraged settlements.

- Whether defendants have tried partial design-arounds.

- Whether courts have constrained claim scope in ways that narrow future enforcement.

Business planning implication: biosimilar entry risk is driven less by a single expiration date and more by the density of enforceable patents in the final 24 to 36 months preceding earliest maturity.

What generic entry risks exist for Repatha and how do biosimilar rules apply?

Repatha is a biologic. The relevant competition route is biosimilars, not small-molecule generics. Revenue erosion typically begins in one of two forms:

- Biosimilar approvals and launch with payer adoption and pricing pressure

- In-market contracting changes ahead of launch, creating discounting even before a biosimilar is fully active

How fast does payer uptake happen when a biosimilar launches?

Uptake speed depends on:

- Interchangeability determinations (where applicable)

- Contract and formulary strategy by large payers

- Patient affordability and switching rules

- Device and administration experience relative to the originator

Expected dynamic: PCSK9 biosimilar acceptance is typically slower than generic small molecules because managed care can demand evidence, and the biologic switching process is more operationally constrained.

What is the Orange Book status of Repatha?

Repatha’s small-molecule Orange Book listing does not directly apply as it is a biologic. The relevant linkage system for biologics is the Biologics License Application (BLA) pathway and its associated exclusivity and patent listing mechanisms tied to the Biologics Price Competition and Innovation Act (BPCIA), which uses the Purple Book structure for biologics patent-related listings rather than the Orange Book.

How do Repatha’s formulation, dosing, and device details affect manufacturing and IP barriers?

For a monoclonal antibody like evolocumab, product differentiation barriers include:

- Protein formulation composition and stability requirements

- Container closure and device compatibility (prefilled pens vs other presentations)

- Manufacturing process controls that ensure glycosylation patterns and other critical quality attributes

What commercial implications do device and administration have?

- Site-of-care selection (home vs clinic)

- Patient education burden

- Therapy persistence

- Payer preference for ease-of-use contracting

Even if the active ingredient is biosimilar, device switching and handling costs can moderate initial volume migration, especially in narrow managed care networks.

What FDA regulatory milestones and label scope affect Repatha market access?

Repatha’s label and population scope shape coverage:

- Population definitions determine whether prior authorization criteria are easily satisfied.

- Cardiovascular risk group labeling influences formulary readiness because outcome endpoints map better to payer definitions of high-risk groups.

How does label breadth translate into revenue?

Wider eligible populations expand addressable patients and reduce payer gate complexity. Even when payers impose criteria, labels that clearly define high-risk cohorts reduce ambiguity and speed coverage approvals.

How do licensing deals, payer contracting, and rebate structures influence Repatha profitability?

For high-cost biologics, gross-to-net is a central determinant of profit trajectory. Repatha’s financial path is shaped by:

- Rebate magnitude tied to managed care performance

- Exclusivity-protecting contracting that rewards preferred placement

- Patient assistance programs that can maintain demand when list price is high and copays rise without support

What signs indicate profitability compression vs expansion?

- Rebate expansion usually signals payer tightening or increased competitive pressure.

- Stable or improving net pricing signals preferred status and strong contracting leverage.

How does Repatha compare with other lipid products on market adoption and competitive intensity?

PCSK9 therapy operates inside a crowded lipid segment. Repatha’s relative adoption depends on how reliably payers conclude that PCSK9s are necessary to reach targets.

Comparison axes that matter for revenue modeling

- Eligible patient volume under real-world payer rules

- Time-to-access after diagnosis or inadequate response to background therapy

- Switching friction compared with competing biologics

- Total cost of care including pharmacy benefit restrictions and medical benefit usage

What does the competitive outlook imply for Repatha’s next 24–48 months?

Near-term outlook is governed by:

- PCSK9 class pricing and contracting cadence (rebate renegotiations)

- Any announced biosimilar development or regulatory submissions

- Formulary shifts driven by payer portfolio strategy

- Operational capacity and supply stability for both originator and competitors

Key planning implication: treat revenue as a function of payer access velocity. In this class, “market size” can look stable while unit growth still varies materially due to contracting outcomes.

Key Takeaways

- Repatha’s financial trajectory is driven primarily by payer access, prior authorization thresholds, and contracting-driven net pricing rather than by changes in clinical positioning alone.

- Competitive dynamics with Praluent and broader lipid sequencing pressure can show up as rebate expansion and formulary churn, affecting net revenue even when gross demand remains resilient.

- Biosimilar risk is best modeled around effective exclusivity loss and the density of the patent estate, not a single expiration date.

- Manufacturing and device-related barriers influence biosimilar uptake speed and can moderate early revenue erosion.

- Over the next 24–48 months, monitor formulary preference status, rebate levels, and regulatory/biosimilar signals for changes in revenue momentum.

FAQs

- What payer criteria most affect Repatha coverage for ASCVD patients?

- How does switching between PCSK9 inhibitors change net revenue for Repatha?

- What does biosimilar launch timing depend on for monoclonal antibodies like evolocumab?

- How do device formats (e.g., autoinjector vs clinic-administered options) influence persistence?

- What contract events typically precede a step-down in PCSK9 utilization?

References

- [No source citations available in the provided context.]