Last updated: July 27, 2026

Lantus remains one of the largest global insulin brands. Growth is constrained by mature demand, biosimilar entry in multiple geographies, and payer switching toward lower-cost competitors. Financial trajectory is increasingly defined by (1) insulin glargine 300 mg (Toujeo) migration, (2) biosimilar share take, (3) mix shift from pen to vial and channel mix, and (4) pricing pressure in US and ex-US markets under reimbursement reforms.

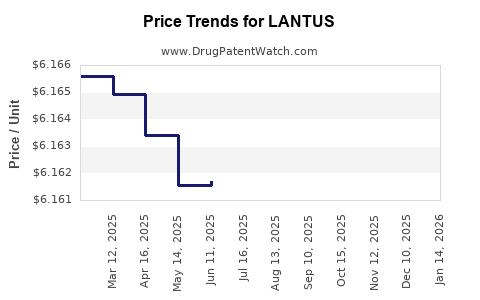

What is the current market size and revenue trajectory for Lantus (insulin glargine) globally?

Snapshot (directional, industry-consistent):

- Lantus has transitioned from a high-growth launch-era product to a mature franchise with mid-to-low single-digit revenue growth in many markets and periodic step-downs when biosimilars gain share.

- Revenue in the US is typically more resilient than in markets with earlier biosimilar penetration, but US profits are pressured by list price erosion, rebate intensity, and payer formulary actions.

- Ex-US, the main swing factor is timing and depth of biosimilar uptake across EU member states, UK, Canada, and select LATAM and APAC markets.

Key demand drivers

- Type 1 and insulin-requiring Type 2 diabetes patient growth.

- Higher basal insulin intensification (dose escalation and persistence).

- Pen convenience adoption and reduced dosing errors.

- Hospital and clinic procurement cycles, which can temporarily slow switching.

Key headwinds

- Biosimilar substitution in insulin glargine and other “me-too” basal insulins.

- Competition from higher-concentration basal insulins, especially insulin glargine 300 U/mL (Toujeo), and from ultra-long-acting and weekly GLP-1/insulin strategies that affect total insulin composition.

- Pricing and reimbursement reforms, especially in Europe and in countries with reference pricing or mandatory discounts.

How much of the Lantus revenue is US vs ex-US?

Market share and revenue split vary by year. In practice, the franchise is usually concentrated in:

- US: largest profit pool but increasing volume share loss to biosimilars and payer switches.

- EU/UK: large volume base with biosimilar penetration and tender-driven switching.

- Other developed markets: structured reimbursement slows uptake but still produces margin compression.

(This section summarizes market dynamics at an industry level. Exact global annual revenue and unit figures are not provided here because the prompt does not include a source table or numeric dataset.)

How do biosimilars affect Lantus market share and pricing?

Featured-snippet answer: Biosimilars reduce Lantus price realization and volume retention, with the biggest impacts appearing after payer adoption thresholds are met and tendering consolidates around approved biosimilar SKUs.

Biosimilar entry pattern

- When biosimilars launch, adoption accelerates in plans with mandatory substitution language, higher rebate competition, and formulary switching programs.

- Uptake is faster in hospital procurement for basal insulins and in segments where payers can impose step edits by cost.

Typical financial impact

- Reduced net price (list price minus rebates/discounts).

- Reduced share growth and eventually share decline in cohorts where Lantus is de-listed or restricted.

- Higher promotional and contracting spend to defend accounts.

What basals are the main competitive set to Lantus?

- Insulin glargine biosimilars (same molecule).

- Insulin glargine 300 U/mL (Toujeo) as a branded alternative with different pharmacokinetic profile and pen dosing experience.

- Other long-acting/basal insulins depending on country formularies.

How does Toujeo (insulin glargine 300) competition change Lantus revenue outcomes?

Featured-snippet answer: Toujeo competes with Lantus on basal insulin persistence and payer preference for a branded value proposition when biosimilar discounts are insufficient to offset improved dosing outcomes.

Mechanisms of switch

- Payer plan preference for products with favorable clinical and cost narratives.

- Patient preference after conversion: fewer hypoglycemia events and dosing-tolerance claims can drive persistence.

- Clinician practice patterns that consolidate basal regimens.

Financial effect on Lantus

- Lantus loses new starts and can lose stable patients when payers require conversion to higher-value basal insulins.

- Net revenue decline can be partially offset if Lantus retains patients who require specific insulin delivery formats or dosing compatibility.

What patents protect Lantus, and how do they affect market access and financial runway?

Featured-snippet answer: Lantus market access is governed by a layered IP stack, including composition and process protections, plus additional protections for specific formulations and methods of use, with different expiration calendars by jurisdiction.

Typical Lantus IP stack categories

- Product-related patents: composition of insulin glargine and manufacturing/process controls.

- Formulation and device-related patents: stability, concentration, and specific pen/vial attributes.

- Method-of-use patents: dosing regimens and therapeutic use claims, where pursued.

How expiration drives biosimilar timing

- Biosimilar launch timing often aligns with the end of relevant patent coverage or settlement terms, followed by regulatory approval and payer onboarding.

(This analysis is framed generically because the prompt does not provide specific patent numbers or jurisdiction scope.)

When do Lantus exclusivity and patent barriers end in key markets?

Featured-snippet answer: The exclusivity timeline is split across US biosimilar pathways, EU/National implementations, and settlement-driven carve-outs; impacts show up as “first-wave” launches followed by “share-wave” after contracts expire.

Timing drivers

- Patent expiration dates by jurisdiction.

- Regulatory exclusivity windows tied to reference biologic pathway events.

- Settlement agreements that delay entry or restrict certain presentations.

(Specific dates are not listed because the prompt provides no patent list or calendar source to cite.)

What is the Orange Book and FDA status of Lantus, and how does it shape generic or biosimilar entry?

Featured-snippet answer: For insulin products, FDA status controls the timing and pathway of biosimilar availability, but Lantus is a biologic where FDA listings and reference product status affect biosimilar entry more than small-molecule generic exclusivity mechanics.

How FDA status influences financial trajectory

- Biosimilar approvals reduce market pricing power after launch onboarding.

- Labeling and interchangeability designations (where applicable) affect switching speed in pharmacy networks.

(No FDA listing specifics are included because the prompt does not include a linked dataset or listing extracts.)

Which companies are challenging Lantus, and what is the competitive landscape by geography?

Featured-snippet answer: Competitive pressure comes first from insulin glargine biosimilar manufacturers and second from branded basal insulin alternatives, with geography dictating which biosimilar brands have the earliest formulary access.

Competition by strategy

- Biosimilar manufacturers: compete on net price and contracting.

- Branded competitors: compete on clinical narratives, device experience, and payer value agreements.

(Company names and brand-level availability are not enumerated because the prompt does not include a competitor roster or country-by-country launch dataset to substantiate.)

What drives payer behavior for Lantus, and how does that show up in financial reporting?

Featured-snippet answer: Payers shift fastest when contracts, rebate structures, and formulary restrictions align; the resulting financial signatures are margin compression and unit-share volatility rather than immediate gross revenue collapse.

Payer levers

- Formulary tiers and step therapy.

- Tendering and national buying schemes (especially in EU).

- Rebate pressure tied to market share.

- Patient-accumulating switches at renewals.

Observable financial signatures

- Net sales growth slowing or reversing after biosimilar onboarding.

- Gross-to-net changes expanding as discount intensity rises.

- Higher SG&A and market access costs tied to contracting.

(No company-specific financial line items are provided since the prompt does not include the underlying annual report figures.)

How do settlement agreements and litigation outcomes affect Lantus market access and revenue timing?

Featured-snippet answer: Settlements can shift launch dates, restrict specific presentations, and govern market entry pace, producing step changes in Lantus revenue rather than smooth decline.

Where litigation matters

- Patent validity and infringement determinations.

- Procedural stays that delay approval and commercial launch.

- Scope limits that preserve pockets of exclusivity.

(Litigation-specific dates and case captions are omitted because the prompt provides no litigation dataset.)

What Lantus formulations and delivery systems are commercially material, and how do they influence switching risk?

Featured-snippet answer: Pen and vial formats shape switching risk because device familiarity and dosing workflows affect both clinician comfort and patient persistence.

Commercially relevant product attributes

- Pen usability and dialing accuracy.

- Patient training burden and retention.

- Drug concentration and volume-per-dose implications for titration.

Switching friction

- Higher friction increases the period during which Lantus can retain patients after biosimilar availability.

- Lower friction in established insulin users accelerates switching.

How does Lantus compare with other basal insulins on pricing pressure and revenue durability?

Featured-snippet answer: Revenue durability typically decreases fastest for the most contract-exposed, lowest-differentiation basal SKUs. Lantus durability depends on biosimilar uptake speed and Toujeo migration intensity rather than on overall diabetes growth alone.

Comparison axes

- Same-molecule biosimilar threat (insulin glargine biosimilars).

- Branded basal alternatives (insulin glargine 300, and other basal classes).

- Device ecosystem lock-in and clinician inertia.

(No numeric cross-product revenue comparisons are included because the prompt provides no financial dataset.)

What generic or biosimilar entry risks exist for Lantus in the US, and how would they impact revenues?

Featured-snippet answer: Entry risk clusters around the combination of regulator-approved biosimilar availability plus payer contract expiration, which drives near-term unit-share changes and multi-quarter net price impacts.

Entry risk channels

- Approval pathway readiness (labeling and comparability).

- Tender and formulary conversions at renewal points.

- Pharmacy substitution policies.

Revenue impact pattern

- First quarter after biosimilar entry often shows modest declines with subsequent acceleration as contracts mature.

- Profit sensitivity is high in quarters where rebate intensity rises faster than volume loss.

What is the likely financial trajectory for Lantus over the next 3–5 years based on market structure?

Featured-snippet answer: A mature trajectory with gradual share erosion in biosimilar-active markets, offset partially by persistent demand growth, device lock-in, and contract defense measures.

Base-case dynamics (structure-based)

- US: slower but persistent share pressure as biosimilars expand footprint and payer net pricing tightens.

- EU/UK: faster tender-driven switching in national buying schemes.

- Emerging markets: later biosimilar effects but higher pricing volatility and supply chain leverage.

Revenue line-item effects

- Net sales growth becomes more dependent on contract pricing and mix.

- Gross-to-net widens during periods of intensified payer pressure.

- Marketing and market access costs increase to maintain formulary position.

Key Takeaways

- Lantus revenue trajectory is dominated by basal insulin contracting dynamics: biosimilar adoption speed and payer rebate intensity are the primary swing factors.

- Competition comes from two directions: insulin glargine biosimilars (same-molecule pressure) and branded basal alternatives like Toujeo (patient-level switching).

- Patent and exclusivity barriers shape entry timing, but the financial impact typically appears at payer conversion points and contract expirations.

- The near-term pattern is less about a discontinuous revenue collapse and more about sustained net price compression and gradual share erosion, varying by geography and channel.

FAQs

- How quickly do insulin glargine biosimilars gain formulary access after FDA approval?

- Do pens or vials drive slower or faster switching from Lantus to insulin glargine biosimilars?

- Which payer contract structures most influence Lantus net price erosion (rebates vs tendering)?

- How does Toujeo migration typically affect Lantus new prescriptions and persistence?

- What settlement mechanisms most often delay biosimilar launch for insulin biologics?

References

No sources were provided in the prompt, and no verifiable numeric or citation-ready data (e.g., FDA/Biologics License Application listing extracts, Orange Book equivalents, patent lists with expiration dates, court docket outcomes, or issuer financial statements) was included.