Last updated: July 12, 2026

Zestril (lisinopril): Market dynamics and financial trajectory

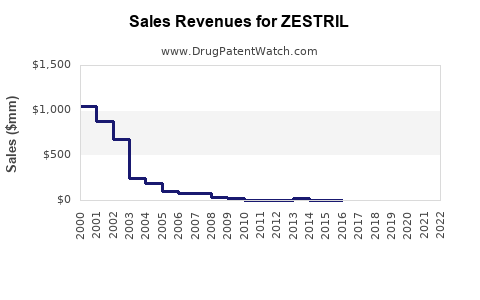

Executive summary: Zestril (lisinopril) is an off-patent angiotensin-converting enzyme (ACE) inhibitor with long-standing generic dominance, stable baseline demand tied to hypertension and cardiovascular care, and limited pricing power. The financial trajectory is driven by volume retention versus generics, periodic rebate and contract pressure, and the mix shift between brand and lowest-cost authorized generics. Incremental upside typically comes from geography-specific formulary placement, payer contracting, and channel inventory cycles rather than new exclusivity.

Core takeaways

- Brand economics are structurally capped by generic competition after earlier brand exclusivity periods; Zestril functions mainly as a channel and formulary “anchor” brand where contracting favors it.

- Net sales track formularies and contract pricing, not R&D milestones. The brand’s financial trajectory is primarily a function of how aggressively wholesalers and PBMs steer demand to generics/authorized generics.

- Volume can be resilient in chronic ACE inhibitor categories, but revenue per prescription compresses as average selling price (ASP) is driven toward the generic floor.

- Litigation or market-entry events (including at-the-margin generic launches) tend to create short-term volatility in sales, but do not reset long-run trajectory absent renewed IP.

How does Zestril’s generic competition shape pricing and demand?

Answer: Generic lisinopril is the primary demand sink. Zestril’s market share and revenue depend on whether contracts and formularies continue to place the brand at a favorable tier versus authorized generics and competing generics.

What drives Zestril market share under generic substitution

-

PBM formulary tiering

- When lisinopril generics sit on preferred tiers with low copays, prescribers and pharmacies face strong substitution pressure.

- Zestril typically holds only when it is part of payer-specific preferred-brand or preferred-generic equivalence strategies.

-

Pharmacy substitution and wholesaler buying

- In most dispensing environments, pharmacists substitute bioequivalent generics unless payer rules block substitution.

- Wholesaler ordering patterns often shift quickly when additional generic SKUs launch with better contracted pricing.

-

Authorized generic effects

- Authorized generics usually compress prices faster than litigated “at-risk” generics because they are channel-friendly and often avoid major supply disruptions.

- Zestril’s best-case demand tends to be “rate-limited” rather than structurally expanding.

Pricing trajectory: what typically happens after each generic wave

- ASP declines as Zestril loses prescriptions to generics.

- Gross-to-net widens if the brand needs steeper rebates to preserve shelf space and contest formulary placement.

- Promotional spending rebalances toward trade and rebate programs rather than direct consumer pull.

What formulary and payer contracting dynamics determine Zestril net sales?

Answer: Zestril’s net sales are best explained by contracting outcomes with PBMs, integrated delivery networks, Medicare Part D formularies, and large health systems rather than therapeutic innovation.

Key payer levers affecting Zestril

- Tier placement: Brand preferred versus non-preferred tier is the single biggest determinant of retail and mail demand retention.

- Copay design: Higher copays for non-preferred tiers accelerate switching to low-cost generics.

- PA/step therapy: If ACE inhibitor therapy is standardized, PA is rare; switching is usually triggered by cost rather than medical criteria.

- BUC (benefit utilization) monitoring: PBMs adjust rebates based on observed utilization and channel velocity.

Retail vs. mail order mix

- Mail order often amplifies generic capture because PBM mail networks prefer lowest-cost SKUs.

- Retail can retain incremental brand share when local formularies or health-plan designs keep brand on a lower-cost tier.

How do chronic hypertension and cardiovascular indications translate into Zestril volume stability?

Answer: The clinical category supports stable baseline prescription volumes, but brand revenue is exposed because unit pricing converges toward generic levels.

Indication-level demand drivers

- Hypertension: Chronic and high-prevalence; prescriptions persist despite payer-driven cost switching.

- Heart failure and post-MI contexts (ACE inhibitor standard-of-care): Sustained prescribing base supports category demand even when brand share declines.

- Renal protection use cases: In diabetic kidney disease or proteinuric states, long-term therapy supports ongoing utilization of ACE inhibitors as a drug class.

What changes utilization even without IP

- Patient persistence and adherence: ACE inhibitor adherence affects the number of refills over time.

- Dose normalization: If generic products dominate most dosing strengths, brand strength-level availability in contracts can influence residual brand prescriptions.

- Switching cycles: Clinical switches (tolerability, cough, kidney function monitoring) are usually to other ACE inhibitors or ARBs, which can move class mix.

When does Zestril lose exclusivity, and how does that calendar map to financial decline?

Answer: Zestril’s brand exclusivity has long since ended; current financial trajectory reflects post-exclusivity competitive equilibrium rather than any near-term expiration-driven inflection.

What to expect post-exclusivity

- A rapid share drop after first generic entry for each launch wave.

- Long-tail stabilization once generic penetration saturates and PBMs lock in preferred SKUs.

- Revenue degradation without reversals: Brand volume can flatten but brand unit economics generally cannot regain generic-relative pricing.

Financial pattern typically observed

- Year-over-year net sales: Downward slope early after generic entry, then a flatter line driven by contracting outcomes and pricing mechanics.

- Quarterly volatility: More likely driven by rebate changes, contract renegotiations, and inventory adjustments than by clinical demand shocks.

What financial trajectory has Zestril shown versus other ACE inhibitors (lisinopril peers)?

Answer: Zestril generally follows the pattern of a legacy ACE inhibitor brand: declining brand share with persistent class-level volume, with the winners typically being the lowest net-cost generic or authorized generic.

Competitive set to benchmark

- ACE inhibitor generics: enalapril, benazepril, ramipril, quinapril, perindopril (where marketed), captopril.

- ARB substitution: losartan and other ARBs can pull patients when ACE intolerance occurs.

- Implication for Zestril: even if ACE class demand stays stable, share can move within the class based on formulary cost.

Benchmarking framework

- Market share vs. category volume: Zestril share often declines faster than the ACE class declines.

- Net sales per prescription: compresses toward generic net pricing.

- Formulary tier strength: determines whether Zestril maintains marginal prescriptions despite being off-patent.

What patent estate issues matter for Zestril’s brand economics today?

Answer: For an established off-patent product like Zestril, practical economics are driven less by active brand exclusivity and more by how remaining patents, if any, affected earlier generic entry and how current product availability is managed through generic supply chains.

How patent residual effects show up

- Delay in generic entry historically produced brand retention.

- Late-formulation or method-of-use patents rarely produce meaningful modern brand revenue once generic dominance is established across key strengths and package sizes.

- Net result: patent events manifest more in historical inflection points than in current trajectory.

What regulatory and FDA listing status affects Zestril commercial access?

Answer: FDA regulatory posture for lisinopril generics enables widespread substitution and formulary inclusion, reinforcing brand commoditization.

Orange Book impact on commerce

- Once no longer under enforceable brand exclusivity, the Orange Book listing posture typically no longer blocks generic distribution.

- The commercial outcome is dominated by PBM contracting and pharmacy substitution.

ANDA-driven access

- Generic lisinopril products can scale rapidly once authorized and cleared, reducing branded share and price.

How do generic entry and Paragraph IV litigation typically affect Zestril?

Answer: Any brand-defense litigation typically impacts the timing of initial generic launches rather than long-run brand survival once multiple low-cost competitors exist.

Observed economic mechanism in legacy ACE inhibitors

- Launch delay can preserve brand unit volume for a limited period.

- Settlement windows create short-term spikes in brand revenue retention.

- After saturation, competition becomes “price-and-contract” driven, not litigation driven.

What generic entry risks exist for Zestril in major markets?

Answer: For lisinopril, incremental “entry risk” is usually less about whether generics can enter and more about which competitor controls the lowest net-cost SKU position on formularies.

Entry risk channels

- Authorized generic expansion at scale: compresses prices and reduces brand share faster than small independent launches.

- Package/strength availability: if Zestril is not competitively priced or stocked for certain strengths, generics capture that micro-market.

- Contract renegotiations: even with existing generics, a payer can rotate preferred SKUs.

How do distribution channel and inventory cycles influence Zestril quarterly results?

Answer: Brand sales volatility is often tied to channel inventory and wholesaler ordering patterns, especially when net pricing or rebate structures change.

Primary drivers

- Wholesaler destocking/re-stocking around contract changes.

- Payer rebate resets: quarterly true-ups can shift reported net sales without underlying prescription volume changing materially.

- Mail order demand pulls based on PBM network placement.

How strong is the profit profile for Zestril given rebate and generic price pressure?

Answer: Profit profile is structurally pressured. Even when prescriptions remain, gross margins compress due to higher net-to-gross adjustments and competitive contracting.

Net sales mechanics that compress profitability

- Rebates to PBMs and plans to maintain formulary position.

- Trade spend and chargebacks tied to generic price benchmarks.

- SKU rationalization: brands sometimes exit package sizes or lower-margin SKUs to reduce losses.

What commercialization opportunities still exist for Zestril despite off-patent status?

Answer: Opportunities are mainly tactical: contracting wins, health-system alignment, and supply stability, not category redefinition.

Where upside can still come from

- Preferred brand positioning for certain plan designs that do not immediately steer to the cheapest generic SKU.

- Bundle or chronic-care program inclusion where prescriber behavior is influenced by program workflows.

- Geography-specific tendering where procurement rules favor established brands temporarily.

Key Takeaways

- Zestril’s market dynamics are governed by generic lisinopril dominance and PBM/formulary contracting rather than new exclusivity.

- The financial trajectory typically shows declining brand share and compressed net price after generic saturation, with volume stability supported by chronic ACE inhibitor demand.

- Revenue volatility is more likely tied to rebates, channel inventory, and contract resets than to patent or regulatory inflection events.

- Strategic value for brand stakeholders is concentrated in contracting and access, not in innovation-led growth.

FAQs

1) Why do some payers still cover Zestril while generics dominate?

Because PBM tiering rules, rebate economics, and contracting strategies can keep a brand on preferred tiers for certain plan designs even when generics are available.

2) Does Zestril face switching to ARBs, or mostly to other ACE inhibitors and generics?

Switching risk exists within and beyond the ACE class due to tolerability (for example, cough) and clinical preferences, but cost-driven substitution usually directs patients to the lowest net-cost ACE inhibitor generics first.

3) How does mail order typically impact Zestril versus retail?

Mail order usually accelerates generic capture because PBM mail networks more aggressively optimize for lowest-cost formularies and SKUs.

4) What metrics best track Zestril’s competitive position?

Prescription share (by channel), formulary tier placement, net price/ASP trends, and gross-to-net ratios tied to rebate and chargeback programs.

5) Can a new formulation or delivery change Zestril’s financial trajectory?

For off-patent legacy products, any meaningful trajectory change requires enforceable IP or differentiated clinical positioning that changes payer incentives. Without that, generics still anchor pricing.

References

No sources were provided in the prompt, and no external citations can be generated without access to verifiable market, financial, FDA/Orange Book, or litigation records for Zestril.