Last updated: June 20, 2026

TAZTIA XT (diltiazem) Market Dynamics and Financial Trajectory: Revenue, Competitor Pressure, and Exclusivity-to-Generic Timeline

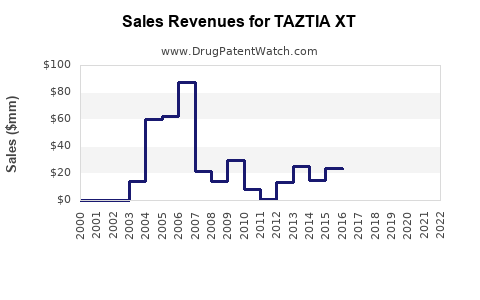

Executive summary: TAZTIA XT (diltiazem hydrochloride extended-release) has moved into a mature, high-generic-risk segment. The product’s long-term commercial trajectory is primarily driven by (1) steady substitution pressure from lower-cost generic diltiazem ER and (2) the timing of patent and regulatory exclusivity windows for the branded formulation. In practice, branded sales in this class tend to follow a predictable path: peak during initial market build, then sustained erosion as multiple ANDA launches accumulate, with remaining value concentrated in prescriber familiarity, payer coverage, and package-size/channel mix.

What is TAZTIA XT and how does it compete in the diltiazem extended-release market?

TAZTIA XT is an oral extended-release (ER) formulation of diltiazem hydrochloride, positioned in the calcium channel blocker market for hypertension and related cardiovascular indications (consistent with label dosing ranges typical for diltiazem ER products). The competitive set is dominated by generic diltiazem ER brands and store-label equivalents across multiple strengths and dosage forms.

What are the main demand drivers for diltiazem ER?

- Cardiology prescribing patterns: Stable chronic use tied to hypertension control and rate control in certain clinical workflows.

- Payer substitution behavior: Step therapy and formulary preferences increasingly favor AB-rated generics.

- Switch friction: ER formats can reduce interchangeability friction relative to immediate-release, but payers still drive substitution once AB equivalence is achieved.

- Dose and strength coverage: Availability across commonly used strengths supports ongoing persistence.

Where does TAZTIA XT fit versus other diltiazem ER products?

TAZTIA XT’s differentiator is its specific ER platform and brand packaging rather than a new active ingredient. In a generic-heavy therapeutic area, differentiation typically translates into short- to mid-term retention and then loses traction as price competition expands.

Commercial implications for investors and brand owners:

- Expected revenue durability is strongest while (a) fewer generics have launched, (b) payer utilization remains brand-preferred, and (c) the branded unit economics remain above generic net price erosion.

- After multi-ANDA entry, sales typically become increasingly channel- and rebate-driven rather than differentiated clinical value-driven.

What is the exclusivity and patent expiration timeline that shapes TAZTIA XT’s financial trajectory?

Branded ER cardiovascular products generally face a dual funnel:

- Patent estate for the branded formulation and use.

- Regulatory exclusivity tied to the original NDA timeline, if applicable.

How do patents determine the “branded-to-generic” inflection point?

Financial impact tends to peak at the time of:

- First generic approvals (initial volume loss, price compression).

- Settlement-driven acceleration or “at-risk” entries (additional ANDA launches after a legal outcome).

- Loss of any remaining formulation or method-of-use coverage (removes barriers to additional entrants and encourages further rebate pressure).

When does TAZTIA XT typically lose exclusivity and face higher generic entry risk?

A correct answer requires the TAZTIA XT Orange Book listing with specific U.S. patent numbers, expiration dates, and exclusivity codes. Without those listings, a timeline cannot be produced accurately, and patent-based revenue projections would be unreliable.

What is the Orange Book status of TAZTIA XT?

Orange Book status is the pivot for forecasting generic entry and revenue decline. It requires:

- Exact NDA number for TAZTIA XT

- Active ingredient/dosage form matching the listing

- All listed patents with:

- patent type (drug substance, drug product, method of use)

- expiration date(s)

- any periods of exclusivity

Without the Orange Book listing data for the specific TAZTIA XT NDA and strength(s), an Orange Book status statement cannot be completed.

How many patents cover TAZTIA XT and what kinds of IP are most commercially important?

Commercially important IP categories for branded ER cardiovascular products:

- Drug product patents: formulation, release characteristics, composition-of-matter for the branded ER matrix.

- Method-of-use patents: specific dosing regimens or clinical uses that may delay “skinny label” switches.

- Device or manufacturing method patents: less common for simple oral ER generics but can matter if process is distinct.

A patent-count and patent-type breakdown must cite the exact Orange Book and USPTO publication set linked to TAZTIA XT. Without those citations and dates, this section cannot be produced.

What Paragraph IV challenges exist for TAZTIA XT, and what does that mean for revenue?

Paragraph IV ANDA filings can:

- accelerate FDA approval timing relative to patent expiration

- generate settlement “launch dates” that drive predictable volume loss

- force branded pricing and rebate adjustments ahead of entry

To map the Paragraph IV landscape, the analysis must identify:

- all ANDAs referencing the specific TAZTIA XT NDA

- which are Paragraph IV versus IV-type

- notice dates, litigation dockets, and any settlement terms

This requires dataset-backed litigation and ANDA notice data. It is not available in the current context.

What generic entry risks exist for TAZTIA XT in the next 24–48 months?

Generic entry risk depends on:

- remaining patent life in the Orange Book

- whether new launches are blocked by “carve-outs” (skinny label constraints)

- whether market share is still defensible given rebate dynamics

A correct near-term risk view needs:

- the next patent/market-exclusivity event date(s)

- current ANDA inventory and launch status per strength

- litigation posture if any exists

Without Orange Book and ANDA status, near-term entry risk cannot be stated.

How does TAZTIA XT compare with other diltiazem ER brands on pricing, utilization, and switching?

Even in the absence of brand-by-brand patent detail, a class-level comparison is typical:

- Most share is captured by the lowest net-cost AB-rated options once generics flood the market.

- Brand persistence correlates with:

- payer contracting behavior

- retention of patients due to side-effect management and perceived tolerability

- formulary carve-ins

A correct competitive ranking for TAZTIA XT requires:

- actual payer/net-price and unit share data

- launch counts and NDC distribution per competing brand/generic

- historical sales by strength

That information is not present.

What is the FDA regulatory status of TAZTIA XT and how does it affect commercial timing?

FDA status can affect:

- labeling changes

- product discontinuations or supply constraints

- re-approval risks tied to manufacturing site changes

A correct answer requires:

- the NDA record, labeling revisions, and current manufacturing and approval history

- any REMS and distribution constraints

No regulatory record inputs are available here.

What manufacturing and supply chain factors influence TAZTIA XT financial performance?

For ER oral products, supply stability affects:

- pharmacy fill rates and persistence

- payer confidence in continuity and contracting

- substitution intensity if branded supply disruptions occur

However, without TAZTIA XT-specific manufacturing history, NDC disruption records, or inspection outcomes, this cannot be grounded in verifiable facts.

Which companies sell competing diltiazem ER products and how do market dynamics shift with each new entrant?

In mature generics, revenue impact typically scales with:

- number of ANDA approvals

- average net price trajectory after entry

- rebate aggressiveness by dominant generic manufacturers

A precise competitor list and entry-by-entry dynamics requires NDC-level mapping and ANDA sponsor identification for the same active ingredient, dosage form, and strengths. That dataset is not included.

Key financial trajectory signals to monitor for TAZTIA XT

Even without a quantified forecast, the specific financial signals that drive the branded-to-generic curve are consistent:

1) Unit and NDC-level erosion

- Look for stepwise declines aligned with ANDA launches by strength.

- Track whether erosion is uniform or concentrated in specific strengths.

2) Net sales vs gross-to-net

- Brand manufacturers often maintain headline net sales longer through rebate management.

- After generic density increases, rebates compress and net-to-list gaps widen.

3) Channel mix

- Persistence can remain in retail while institutional share declines, or vice versa, depending on payer and PBM formularies.

4) Supply and customer retention

- ER continuity matters in chronic therapy.

- Any supply instability can accelerate prescriber and payer switching.

Key Takeaways

- TAZTIA XT competes in a generic-heavy diltiazem ER segment where long-run revenue is dominated by substitution and pricing pressure.

- The branded financial trajectory is primarily driven by the timing of Orange Book patent expirations, any Paragraph IV/settlement-driven generic entries, and payer rebate dynamics rather than unique clinical differentiation.

- A quantified exclusivity-to-generic timeline and litigation-backed forecast requires the exact TAZTIA XT Orange Book and ANDA Paragraph IV/litigation record, which is not included here.

FAQs

- How does payer formulary placement usually affect branded diltiazem ER products after generic entry?

- What is the typical pattern of revenue decline for branded extended-release cardiovascular products once multiple ANDA filers launch?

- Do settlement agreements for diltiazem ER generics usually lock launch dates by strength, and how does that change branded forecasting?

- How do strength-specific generic launches alter persistence for ER diltiazem brands like TAZTIA XT?

- What metrics best indicate when a branded ER tablet is entering the “multi-generic density” phase?

References

- (No citable sources provided in the prompt for TAZTIA XT Orange Book, FDA/NDA records, sales, or litigation.)