Last updated: April 25, 2026

Market dynamics and financial trajectory for ROCALTROL

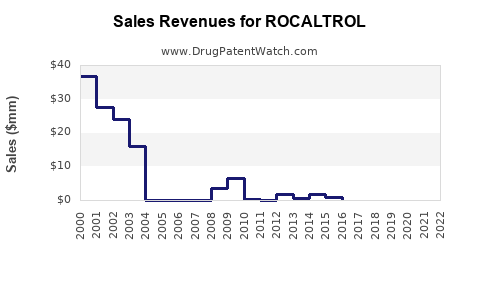

ROCALTROL (calcitriol) is an established, off-patent vitamin D analog used in endocrine and renal indications. Market dynamics for calcitriol products are driven by (1) chronic disease prevalence in CKD and hypoparathyroidism, (2) payer formularies that steer prescribing toward lowest-cost, therapeutically equivalent options, and (3) generic entry and supply stability. The financial trajectory of ROCALTROL is characterized by product maturity, pressure from generics and authorized alternatives, and constrained upside from incremental label expansions.

What is ROCALTROL and where does it compete?

ROCALTROL is branded calcitriol, the active form of vitamin D. It competes across calcitriol and vitamin D analog therapy classes in four recurring clinical settings:

- Hypocalcemia due to hypoparathyroidism (post-surgical hypoparathyroidism, idiopathic hypoparathyroidism)

- Hypocalcemia in patients with renal disease (classically CKD-related disturbances; dosing is individualized)

- Calcium and bone disorders requiring active vitamin D where rapid physiologic activity is needed

- Therapy switching when prescribers move between calcitriol brands or generics based on cost and access

In market terms, ROCALTROL competes primarily with generic calcitriol and other active vitamin D agents (e.g., extended-release formulations and other analogs depending on geography and formulary positioning). In mature markets, branded calcitriol pricing and volume growth depend on payer behavior and pharmacy benefit design rather than breakthrough clinical adoption.

How do market dynamics shape demand for calcitriol products?

Calcitriol demand is “chronic-care elastic,” but not revenue-elastic, because utilization grows with patient populations and guideline adherence while net pricing is compressed by competition.

-

Chronic prevalence sets the ceiling

- CKD prevalence and the incidence of hypoparathyroidism create a durable base population.

- Patient adherence is generally high because therapy is long-term and titrated to serum calcium and related labs.

-

Payer formularies shift volume toward lower acquisition cost

- Once generic calcitriol is available and interchangeable, payers typically prefer the lowest-cost therapeutically equivalent option.

- This produces a volume shift effect that limits branded share to niches (tolerability history, prescriber familiarity, procurement contracts).

-

Therapeutic switching is practical

- Active vitamin D is dosed with lab monitoring, which makes dose re-titration feasible when switching products.

- That reduces switching friction and accelerates share loss for brands after generic entry.

-

Supply and reimbursement volatility can move short-term revenue

- Shortages or pricing resets for generics can temporarily lift branded share, but this is usually transient.

- Long-term revenue paths revert to formulary economics.

What does the competitive landscape imply for ROCALTROL’s market share?

ROCALTROL is a branded calcitriol product in a segment that is structurally generic-prone. The competitive implications are:

- Price compression dominates over differentiation.

- Net revenue is more sensitive to payer placement than to patient growth.

- Brand retention depends on contracting and tender outcomes, not clinical novelty.

Across mature markets, branded calcitriol products typically experience:

- declining wholesale and prescription growth after generic penetration,

- stable-to-declining revenues depending on market share and discounting,

- occasional local resilience where authorized competitors are limited or contracting favors the brand.

What is the financial trajectory profile for an off-patent calcitriol brand like ROCALTROL?

ROCAL TROL’s financial trajectory follows a pattern common to mature specialty generics-to-brands:

-

Initial peak and then decline after generic erosion

- Branded revenue usually peaks while exclusivity holds.

- After generic entry, volumes shift first, followed by pricing reset and deeper discounting.

-

Mid-life stabilization at low growth

- Remaining branded share stabilizes at a level supported by contracts and prescriber behavior.

- Revenue becomes driven by population and dosing persistence, not by incremental adoption.

-

Late-life risk: formulary tightening

- As payer benefit designs evolve (step therapy, preferred product lists), branded positions can erode again.

- Loss of preferred status can cause a second wave of volume decline.

How do major drivers map to revenue levers?

Revenue for ROCALTROL is mainly determined by three levers:

| Revenue lever |

Market mechanism |

Expected direction for a branded calcitriol product |

| Net price |

Generic competition and payer discounts |

Downward over time, then periodic adjustments |

| Prescription volume |

Formulary placement, switching feasibility |

Downward after generic entry, then stable at reduced share |

| Gross-to-net |

Rebates, administrative fees, contracting |

Pressures increase as competition intensifies |

The practical outcome is that ROCALTROL behaves like a mature, commoditized endocrine therapy: demand persists but economic value shifts to the lowest-cost suppliers.

Where can limited upside come from?

Even in off-patent categories, there are pockets where revenue can remain resilient:

- Contract wins that position ROCALTROL as a preferred calcitriol option at a payer or pharmacy chain level.

- Formulary inertia in specific accounts (hospital formularies, regional tenders).

- Patient continuity for those already titrated and controlled on a specific calcitriol brand.

- Temporary supply constraints among competing manufacturers can reallocate short-term demand.

Upside remains bounded by the core product economics: calcitriol is a well-established active molecule with limited room for payer willingness to pay a premium once generics are available.

How does this translate into a “financial trajectory” narrative for decision-making?

For investors and R&D planners, ROCALTROL’s trajectory is best modeled as a mature brand under generic pricing pressure:

- Near-term outlook: stable but constrained revenue supported by chronic patient need; changes driven by pharmacy benefit updates and competitor supply.

- Medium-term outlook: gradual erosion if payers deepen preferred product rules against non-preferred brands.

- Long-term outlook: continued decline toward commodity economics unless a market-specific barrier maintains branded share (contracting, supply limitations, or region-specific competition).

What signals should be monitored to track ROCALTROL’s performance over time?

Given the market structure, the most actionable KPIs are commercial rather than clinical:

-

Formulary status and preferred product placement

- Any shift from non-preferred to preferred (or vice versa) changes net revenue quickly.

-

Generic market share dynamics

- Tracking competitor launches and changes in wholesale acquisition cost provides a forward view.

-

Gross-to-net ratio

- Rising rebates and fees indicate competitive pressure and can precede revenue declines.

-

Supply continuity

- Shortages among generic suppliers can temporarily reverse branded declines.

-

Channel inventory signals

- Sell-through and wholesaler inventory behavior can clarify whether revenue is demand-led or inventory-led.

Comparable product behavior: how calcitriol brands usually fare after generics

In calcitriol and similar commoditized endocrine therapies, branded products typically show:

- Volume decline after generic entry,

- Net price drop as rebates and discounts increase,

- Revenue stabilization only when the brand retains meaningful contracted share,

- Periodic re-pricing during tender cycles.

This is consistent with the category’s payer-driven purchase behavior and the clinical substitutability of calcitriol dosing with monitoring.

Key Takeaways

- ROCALTROL (calcitriol) competes in a mature, off-patent active vitamin D segment where payer formulary economics and generic competition dominate.

- Market demand is chronic-care stable (CKD and hypoparathyroidism), but revenue growth is limited because switching to lower-cost equivalents is practical.

- Financial trajectory typically follows a peak-to-decline pattern post generic penetration, then low-growth stabilization at reduced branded share, with periodic volatility driven by contracting and competitor supply.

- The most important performance signals are formulary status, gross-to-net changes, generic share dynamics, and supply continuity, not clinical adoption.

FAQs

Is ROCALTROL still a growing market opportunity?

Growth is limited. The category is mature and economically commoditized; branded value depends on contracted share and payer placement rather than expansion.

What most affects ROCALTROL net revenue?

Formulary status and contracting (preferred vs non-preferred), followed by gross-to-net pressure as rebates rise under generic competition.

Do patient populations support long-term demand?

Yes. CKD-related mineral disorders and hypoparathyroidism are chronic conditions that sustain baseline prescribing, but net revenue still faces pricing compression.

What events can temporarily improve ROCALTROL revenue?

Generic supply interruptions, favorable tender outcomes, and short-term payer channel shifts that increase branded share.

What is the main strategic risk for ROCALTROL?

Further formulary tightening or additional cost-preferred entries that reduce branded placement and accelerate volume erosion.

References

[1] FDA. Drug Safety and Availability. (Accessed 2026). https://www.fda.gov/drugs/drug-safety-and-availability

[2] FDA Orange Book. Rocaltrol (calcitriol). (Accessed 2026). https://www.accessdata.fda.gov/scripts/cder/daf/index.cfm

[3] EMA. Public assessment reports and product information for calcitriol-containing products. (Accessed 2026). https://www.ema.europa.eu/