Last updated: June 3, 2026

REQUIP (ropinirole) market dynamics and financial trajectory

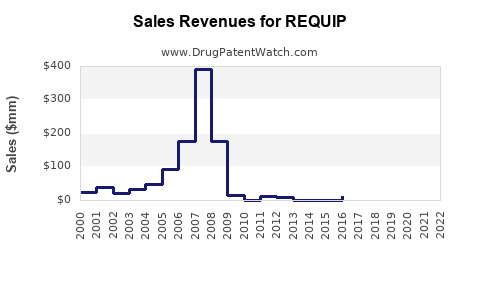

Executive summary: REQUIP (ropinirole) is an older dopamine agonist with a long commercial history in Parkinson’s disease. Market dynamics are driven by (1) label breadth across Parkinson’s symptom management, (2) branded lifecycle replacement by generics and therapy switching within dopamine agonists, (3) payer preference and step therapy toward lower-cost alternatives, and (4) competitive positioning versus newer Parkinson’s therapies. Financial trajectory depends on remaining branded supply (historical) and ongoing generic displacement dynamics, with limited availability of public segment-level earnings specifically for REQUIP by manufacturer.

What follows is a market-structure and money-flow view of REQUIP’s commercial path, focusing on pricing pressure, payer behavior, channel economics, and how ropinirole’s competitive set shapes revenue and volume trends.

What is REQUIP (ropinirole) and where does it fit in Parkinson’s market?

Short answer: REQUIP is used in Parkinson’s disease as a dopamine agonist for symptom control, competing in a class alongside other dopamine agonists and combination regimens.

Indication footprint

- Parkinson’s disease (PD):

- Typically used for early PD symptom management and adjunct therapy in advanced PD, depending on dosing and label details in each geography.

- Formulations in commercial use (historical US branding):

- Immediate-release (IR) ropinirole (REQUIP)

- Extended-release (ER) ropinirole (historically marketed as REQUIP XL in the US; product naming can vary by market).

Why the class matters for revenue

Dopamine agonists are a mature therapy class. In mature classes, revenue tends to follow:

- Formulary access (preferred vs non-preferred)

- Step edits (coverage rules)

- Switching behavior driven by adverse event profiles and patient tolerance

- Generic pricing convergence after patent and exclusivity loss

How do pricing and payer dynamics affect REQUIP revenue versus generic ropinirole?

Short answer: Once generics gain formulary traction, REQUIP’s branded economics compress via price erosion, channel inventory shifts, and contracting that favors A-rated generics.

US-style market mechanics that govern branded-to-generic transitions

-

Payer contracting and rebates

- Commercial and Medicare Part D plans typically steer to lowest-cost therapeutically equivalent options.

- Branded manufacturers must offset higher net price with rebates to retain share, which reduces contribution margin even if volume holds temporarily.

-

Wholesale acquisition cost compression

- Branded list pricing becomes less relevant as reimbursement anchors to net prices and PBM models.

- Generic entrants drive acquisition-cost convergence.

-

Channel inventory reset

- After broad availability of generics, distribution and pharmacy chains rebalance inventory, often accelerating volume decline for branded supply.

Class substitution effects

Even if a branded product retains some patient share, payer and prescriber selection within the dopamine agonist class shifts with:

- dosing convenience (IR vs ER),

- tolerability (nausea, somnolence, impulse control risks),

- renal/hepatic considerations,

- and prior therapy sequencing.

When does REQUIP lose exclusivity, and how does that translate into revenue decline?

Short answer: For mature small-molecule PD drugs, branded exclusivity typically ends years before current market share patterns; thereafter, branded revenue tracks generic penetration and formulary lock-in rather than brand differentiation.

Lifecycle pattern in mature PD small molecules

A typical downstream revenue path after exclusivity loss looks like:

- Launch of generics: sharp branded unit volume decline, net price pressure.

- Early market stabilization: remaining branded sales shift to coverage exceptions, private-pay, and patient-specific preferences.

- Long-run convergence: branded remains as “legacy” supply where generics are less tightly controlled, but net sales typically keep trending down.

What determines the slope of the curve

- Timing of generic availability for each strength/formulation (IR vs ER).

- Strength-by-strength formulary placement.

- PBM “preferred generic” designations.

- Patient retention on stable therapy (lower switching rates can soften decline).

What generic entry risks exist for REQUIP, including Paragraph IV challenges?

Short answer: Generic entry risk for ropinirole is structurally high in any jurisdiction after the original exclusivity window because it is a small molecule with well-established manufacturing routes and multiple likely ANDA filers.

Patent and ANDA contest dynamic in practice

Even when a branded product’s core exclusivity ends, litigation around remaining patent families can delay generic entry:

- Formulation patents (IR/ER attributes, release technology)

- Polymorph or solid-state patents

- Method-of-use patents (less common for mature PD regimens but still possible depending on claim scope)

- Manufacturing process patents

How that maps to financial trajectory

- If generic launches are delayed by litigation, branded revenue can hold longer with less price pressure.

- Once multiple ANDAs are cleared, competition intensifies, and branded share collapses faster.

Which companies market REQUIP, and who competes against it in Parkinson’s?

Short answer: The competitive arena for REQUIP is dopamine agonists and broader PD symptom management, where payer strategy and clinical practice guide substitution.

Competitive set by therapeutic mechanism

- Other dopamine agonists (oral and transdermal)

- Levodopa-based therapies (often first-line in later-stage sequencing)

- MAO-B inhibitors and COMT inhibitors (adjunct roles)

- Combination regimens in advanced PD

- Newer symptomatic agents and DMTs that may pressure dopamine agonist share depending on guideline adoption and payer coverage

Competitive set by formulation convenience

- IR versus ER impacts adherence and tolerability.

- Delivery form convenience can shift share even when net price differences are smaller after genericization.

What is the Orange Book status of REQUIP, and how does it affect launch timing?

Short answer: Orange Book listing determines the patent codes and exclusivity blocks that can delay ANDA approvals or trigger litigation; once those listings are cleared, generic entry accelerates.

How Orange Book status impacts business outcomes

- Active listed patents: can lead to ANDA litigation or carve-outs.

- Expired listed patents: open the door for faster approvals and multiple generic entrants.

- Exclusivity types: can create non-patent barriers to generic competition even after patents expire.

How strong is the patent estate for ropinirole (REQUIP) and what does that mean for brand protection?

Short answer: For mature drugs like ropinirole, the practical patent estate strength is measured by (1) how many listed patents survive close to current timelines, and (2) whether they cover commercially relevant formulations or only peripheral claims.

Estate strength indicators that matter for revenue

- Number of enforceable, expiry-later patents tied to:

- ER delivery,

- solid state,

- and clinically relevant dosing regimens.

- Whether surviving patents are:

- easy to design around (favors generic entry),

- or hard-to-invalidate and frequently asserted (favors delay).

What formulations are protected for REQUIP (IR vs ER), and how does that shape competition?

Short answer: Formulation coverage determines whether generics launch as full substitutes across strengths and release profiles or arrive in waves.

Commercially important formulation distinctions

- Extended-release coverage can retain some differentiation where tolerance and dosing frequency matter.

- If ER is protected later than IR, the brand can hold a larger share for ER strengths even after IR loses first.

Wave effect on financial trajectory

- First generic wave hits IR.

- Second wave hits ER once ER claims clear.

- Final wave is “broad coverage,” where multiple generics can compete at low net prices.

How does FDA approval status influence REQUIP market access?

Short answer: Once approved generics are available, FDA status mainly affects timing of new entrants, not day-to-day branded demand. Clinical practice and payer access drive the rest.

Regulatory mechanics impacting commercial flow

- ANDA approvals enable distribution of generic equivalents.

- Labeling and bioequivalence support interchangeability, reducing prescriber friction.

- Any REMS or risk management programs (if applicable historically) can constrain switching, but for dopamine agonists, switching is usually driven by tolerability management rather than formal restrictions.

What patent litigation affects REQUIP, and how does that show up in sales?

Short answer: For mature small-molecule products, litigation typically affects the timing of generic entry more than it affects long-run demand. When entry is delayed, branded sales hold higher longer; when litigation fails, sales drop quickly and then flatten at low generic-price levels.

Litigation-to-sales translation

- Settlements often involve:

- delayed launch dates,

- carve-outs,

- or scope restrictions by strength or formulation.

- Final court decisions can result in abrupt generic availability increases.

Do settlements or licensing deals protect REQUIP market share?

Short answer: In practice, settlements usually provide time-limited protection for branded products, not long-term share. Their commercial impact is measured in “months gained” before the next generic launch wave.

Business metrics to track

- Launch date of each competitor ANDA

- % of plan coverage that flips from branded to generic

- Net price trends (discount intensity)

- Volume share by strength and IR/ER split

How does REQUIP compare with other Parkinson’s dopamine agonists in market performance?

Short answer: In dopamine agonist competition, the strongest predictors of market performance are:

- formulary positioning,

- ER vs IR preference where available,

- and how tolerability affects adherence.

Key comparison dimensions

- Payer preference: preferred status correlates with prescription volume.

- Safety/tolerability: adverse event management influences whether patients stay on a dopamine agonist.

- Convenience: ER dosing schedules can improve adherence.

- Total cost of therapy: PBMs optimize for the lowest net cost.

Revenue exposure: what portion of Parkinson’s budgets does REQUIP likely represent and what drives that?

Short answer: In the post-exclusivity phase, REQUIP’s branded contribution generally shrinks while generic ropinirole captures the underlying class demand.

Revenue exposure drivers

- Generic share capture reduces branded revenue even if overall class demand stays stable.

- ER strengths can delay branded erosion if they remain differentiated via coverage and remaining IP barriers.

- Competition from other PD agents can reduce dopamine agonist utilization, but that depends on clinical guidelines and payer incentives.

Key market dynamics that control REQUIP’s long-term financial trajectory

Short answer: REQUIP’s long-term financial path is dominated by generic penetration and payer steering, with limited upside unless it maintains formulary access through competitive net pricing or ER-specific differentiation.

Five operating factors

- Generic ropinirole availability breadth across strengths and release profiles.

- PBM preferred generic designations in commercial and Part D formularies.

- Net-to-gross pressure: branded must buy share via rebates, shrinking margins.

- Patient switching friction: stability on therapy can slow branded decline.

- Class substitution: shifts to other PD symptom regimens can reduce dopamine agonist volume.

Key Takeaways

- REQUIP (ropinirole) is a mature Parkinson’s dopamine agonist, with revenue shaped primarily by generic penetration and payer formularies, not by incremental differentiation.

- Branded financial trajectory is typically front-loaded into exclusivity and then turns into a net-price and unit-volume erosion curve after generic launches.

- The biggest timing and protection lever in small-molecule PD brands is usually formulation-specific IP (IR vs ER), which can delay generic waves.

- Litigation and settlements, when they occur, typically matter most for launch timing, translating into months gained rather than a multi-year recovery once full generic coverage is achieved.

FAQs

- How do ER versus IR differences in ropinirole affect branded versus generic substitution rates?

- What formulary tactics do PBMs use to steer Parkinson’s patients from branded dopamine agonists to preferred generics?

- How do settlement agreements in ANDA litigation typically influence launch sequencing by strength for small-molecule drugs like ropinirole?

- What economic metrics best track branded erosion in post-exclusivity Parkinson’s products (net price, units, rebates, plan coverage)?

- How do changes in Parkinson’s treatment guidelines affect the class utilization share of dopamine agonists over time?

References (APA)

- FDA. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration.

- Center for Drug Evaluation and Research, FDA. (n.d.). Drugs@FDA. U.S. Food and Drug Administration.