Last updated: June 19, 2026

QUDEXY XR (topiramate) Market Dynamics and Financial Trajectory

Executive summary: Qudexy XR (topiramate extended-release) is a niche neurology product with revenue driven primarily by epilepsy demand and payer-specific access for branded extended-release topiramate. The financial trajectory is constrained by (1) competitive pressure from generic topiramate formulations, (2) formulary steerage toward lower-cost immediate-release generics, and (3) the usual neurology payer preference for established, low-cost options. Commercial outcomes remain sensitive to generic pricing, rebate dynamics, and the pace of channel inventory normalization.

How is Qudexy XR priced and what market dynamics shape payer access?

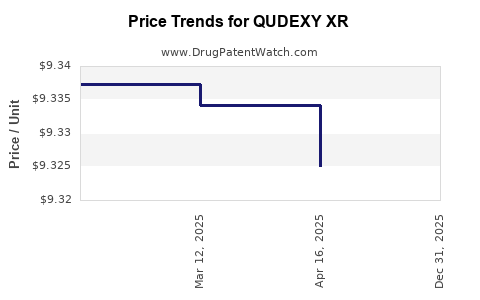

Direct answer: Qudexy XR pricing and net sales are determined by wholesale acquisition cost (WAC) versus net price after rebates, patient assistance, contracting, and substitution behavior. Market access is most influenced by the extent to which payers cover branded extended-release topiramate versus immediate-release generics, and by whether step-therapy policies favor switching to cheaper generics before authorizing brand coverage.

Payer contracting forces for extended-release topiramate

Key dynamics typically affecting branded extended-release antiepileptics include:

- Formulary tiering: Branded extended-release products often land on higher tiers, while generics occupy preferred tiers.

- Prior authorization and step therapy: Payers may require failure on immediate-release topiramate or other antiepileptics.

- Substitution pressure: Pharmacy substitution and therapeutic interchange influence prescription capture, especially when payers can achieve similar clinical outcomes at lower cost.

- Rebate intensity: Brand manufacturers may raise rebates to preserve formulary placement, compressing operating margin as volume becomes more price-elastic.

Competitor set influencing Qudexy XR

Qudexy XR competes in extended-release topiramate and broader anti-seizure therapy budgets:

- Immediate-release topiramate generics (price benchmark and substitution anchor)

- Other branded antiepileptics using step-therapy pathways

- Neurology prescriber preference effects: physicians may keep patients stable on an established regimen, but payer pressure can still shift new starts.

What are the revenue drivers and unit economics behind Qudexy XR growth or decline?

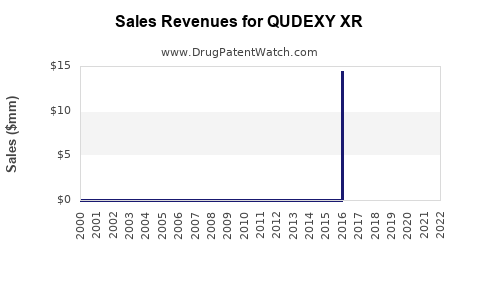

Direct answer: Qudexy XR revenue movement is driven by net price (rebate contracting), new patient starts versus continuation, prescription channel inventory, and patient-level persistence. In branded neurology, volume typically slows as generics increase market share unless the brand maintains differentiated access or clinician inertia.

Primary revenue levers

- New starts vs continuation: Extended-release topiramate captures new starts if payer coverage is broad and if prescribers prefer once-daily regimens for adherence.

- Persistence: Epilepsy patients often persist, but discontinuations rise when payers force switches, or when patients experience tolerability issues.

- Channel behavior: In neurology, inventory and wholesaler buying patterns can temporarily affect quarterly sales, followed by normalization.

Net price compression mechanics

Net sales = WAC minus rebates minus chargebacks minus discounts. For brands facing generic alternatives, net price often trends down even when unit volume holds, because payers renegotiate after formulary reviews.

When does Qudexy XR face exclusivity roll-offs that impact financial trajectory?

Direct answer: The financial trajectory of Qudexy XR is tied to the end of market exclusivity and the timing of generic entry around formulation, use, and manufacturing patents. As exclusivity weakens, branded sales typically shift from growth to defense mode with higher rebate pressure.

How exclusivity and generic entry usually transmit into revenue

- Pre-entry: Brand retains formulary position with lower rebate intensity.

- At entry: Competitors price aggressively, and payers shift tier placement or tighten prior authorization.

- Post-entry: Brand survives mainly on clinician inertia, patient persistence, and residual payer coverage.

What generic entry risks exist for Qudexy XR, and how do they affect forecasts?

Direct answer: Generic entry risk is the primary downside driver for branded topiramate extended-release, because competing products can undercut net price while meeting bioequivalence. Forecast sensitivity is highest for new prescriptions, not continuation alone.

Mechanisms of generic capture

- Therapeutic interchange: Even when substitution rules prevent direct substitution, prescribers can be nudged by coverage policies.

- PA tightening: Payers may require documentation of failure on non-brand products.

- Switch programs: Managed care organizations often target switches after generic availability.

Financial impact profile

- Revenue decline: Usually front-loaded in unit share before fully reflected in net price, depending on contracting.

- Margin erosion: Rebates and access payments often rise after generic entry.

- Net sales volatility: Channel inventory effects can mask underlying share loss for one or two quarters.

What formulations and patent estate features matter most for Qudexy XR economics?

Direct answer: For an extended-release product, the economic risk is concentrated in formulation and method-of-use barriers. If those barriers weaken, generic or AB-rated alternatives can capture market share quickly without requiring clinical outcome differentiation.

Formulation patent vectors that affect exclusivity

Common patent categories affecting extended-release products include:

- Controlled-release matrix technologies

- Bead/pellet systems and coating approaches

- Dosing unit design and dissolution profile targets

- Manufacturing process parameters

- Stability and release-rate methods

Method-of-use and labeling protection

If method-of-use patents exist, they can delay generic substitution only when claims map tightly to the labeled regimen and when payers require compliance with the claimed use. In practice, method-of-use protection is often narrower than formulation protection for commercial access.

What is the Orange Book status of Qudexy XR?

Direct answer: Qudexy XR’s Orange Book status determines whether ANDAs can be approved with Paragraph IV certifications or whether they can be approved under other pathways without triggering litigation. Orange Book listings also map out the remaining patent landscape for specific dosage forms.

Orange Book elements investors track

- Listed patents and their expiration dates

- Patent types (drug substance, drug product, method of use)

- Any active exclusivity flags (e.g., periods tied to exclusivity rather than patents)

- ANDAs citing those patents (if publicly available through subsequent filings and court records)

What patent litigation affects Qudexy XR market entry, pricing, and revenue timing?

Direct answer: In branded oral neurology products, patent litigation mainly influences the timing of generic launches and the magnitude of branded net price erosion in the launch year. The commercial path depends on whether a settlement blocks entry, limits entry to certain strengths, or triggers “at-risk” launch.

Litigation-to-commercial translation

- Stipulated settlements can delay entry and protect revenue for the settlement duration.

- Partial approvals (if applicable) can allow limited competitive presence while the brand still holds most formulary placement.

- Adjudication outcomes can accelerate entry and force rapid rebate readjustments.

How does Qudexy XR compare with other anti-seizure brands and topiramate options?

Direct answer: Qudexy XR competes primarily with immediate-release topiramate generics on cost and with other antiepileptics on payer budgets and step-therapy pathways. Unlike highly differentiated products, extended-release topiramate’s value proposition is adherence and tolerability profile via release characteristics, not disease-modifying novelty.

Competitive comparison dimensions

- Price position: generics dominate the low-cost tier

- Formulary design: coverage varies by insurer and prior authorization requirements

- Patient continuity: brand maintains persistence in stabilized patients

- Clinician switching behavior: depends on side-effect profile and dosing schedule

What is the sales trajectory for Qudexy XR by quarter and how does it typically evolve post-generic pressure?

Direct answer: Branded extended-release products facing generic topiramate typically show a pattern of (1) gradual share loss after the first meaningful generic entry window, (2) net price compression due to rebates, and (3) eventual stabilization at a lower run-rate if remaining formulary access persists for certain plan types.

Modeling pattern used in coverage and forecasting

- Year 0-1 (generic entry window): unit share declines first, then net price falls as contracts are renegotiated.

- Year 1-2: volume stabilizes, but margin may remain compressed due to persistent contracting disadvantages.

- Year 2+: the brand’s performance becomes more dependent on patient persistence and insurer-specific formularies.

Commercial outlook: what scenarios drive bull, base, and bear outcomes for Qudexy XR?

Direct answer: The dominant scenarios are generic pricing intensity, formulary coverage retention, and the ability to avoid forced switch requirements for new starts.

Bull case

- Strong payer contracts sustain coverage and new starts.

- Generic share gains are slower due to PA barriers or clinician persistence in extended-release dosing.

- Rebate costs are contained, preserving net price stability.

Base case

- Ongoing share erosion continues, with net price declining as payer contracting tightens.

- Brand maintains a minority but durable share among plans with broader coverage.

- Sales track a downward but more gradual slope.

Bear case

- Expanded generic availability triggers stricter step therapy and forced switch policies.

- Net price drops faster than volume, driving margin compression.

- Sales decline accelerates in new start cohorts.

Key Takeaways

- Qudexy XR’s financial trajectory is shaped by payer access rules, rebate intensity, and substitution dynamics versus immediate-release topiramate generics.

- Generic entry timing and the persistence of any Orange Book or litigation-driven barriers are the primary levers influencing revenue slope.

- Forecast sensitivity is highest for new patient starts and net price compression, with continuation/persistence providing partial offset.

- The extended-release differentiation is mainly dosing and tolerability-based, so competitive economics often dominate long-term brand survival.

FAQs

1) What drives Qudexy XR net price changes versus gross WAC?

Rebates, payer contracting, chargebacks, and formulary placement changes drive the gap between WAC and net sales.

2) Does Qudexy XR’s extended-release profile protect it from generic competition?

It can slow switching in some patient cohorts, but generic AB-rated extended-release products or therapeutic interchange pressures still drive economic loss.

3) How do prior authorization and step therapy impact Qudexy XR prescription volume?

They reduce new starts and increase the proportion of prescriptions requiring documentation, often shifting prescribers toward lower-cost alternatives.

4) Are method-of-use patents more commercially meaningful than formulation patents for Qudexy XR?

Formulation patents usually create broader commercial protection for extended-release products, while method-of-use protection can be narrower depending on claim-to-label mapping.

5) What is the largest risk to Qudexy XR revenue after generic entry?

Rapid net price compression and new prescription share loss driven by formulary and PA tightening.

References (APA)

- U.S. Food and Drug Administration. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. FDA.

- U.S. Food and Drug Administration. (n.d.). Drug Approval Reports and Labeling. FDA.