Share This Page

PREVALITE Drug Patent Profile

✉ Email this page to a colleague

When do Prevalite patents expire, and what generic alternatives are available?

Prevalite is a drug marketed by Aiping Pharm Inc and is included in one NDA.

The generic ingredient in PREVALITE is cholestyramine. There are eight drug master file entries for this compound. Fifteen suppliers are listed for this compound. Additional details are available on the cholestyramine profile page.

DrugPatentWatch® Litigation and Generic Entry Outlook for Prevalite

A generic version of PREVALITE was approved as cholestyramine by EPIC PHARMA LLC on August 15th, 1996.

AI Deep Research

Questions you can ask:

- What is the 5 year forecast for PREVALITE?

- What are the global sales for PREVALITE?

- What is Average Wholesale Price for PREVALITE?

Summary for PREVALITE

| US Patents: | 0 |

| Applicants: | 1 |

| NDAs: | 1 |

| Finished Product Suppliers / Packagers: | 1 |

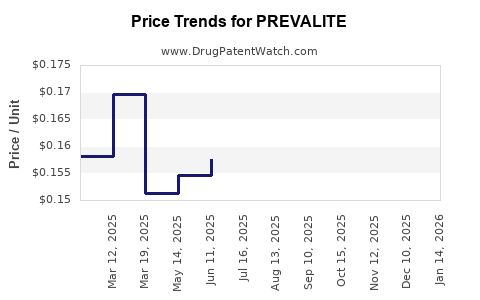

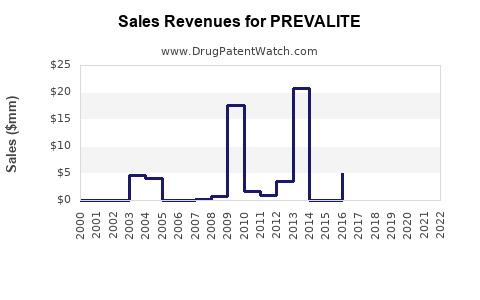

| Drug Prices: | Drug price information for PREVALITE |

| DailyMed Link: | PREVALITE at DailyMed |

Pharmacology for PREVALITE

| Drug Class | Bile Acid Sequestrant |

| Mechanism of Action | Bile-acid Binding Activity |

US Patents and Regulatory Information for PREVALITE

| Applicant | Tradename | Generic Name | Dosage | NDA | Approval Date | TE | Type | RLD | RS | Patent No. | Patent Expiration | Product | Substance | Delist Req. | Exclusivity Expiration |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Aiping Pharm Inc | PREVALITE | cholestyramine | POWDER;ORAL | 073263-001 | Feb 22, 1996 | AB | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Aiping Pharm Inc | PREVALITE | cholestyramine | POWDER;ORAL | 073263-002 | Oct 30, 1997 | AB | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| >Applicant | >Tradename | >Generic Name | >Dosage | >NDA | >Approval Date | >TE | >Type | >RLD | >RS | >Patent No. | >Patent Expiration | >Product | >Substance | >Delist Req. | >Exclusivity Expiration |

Prevalite (pravastatin sodium) Market Dynamics and Financial Trajectory: Exclusivity, Competitive Pressure, Pricing, and Forecast Risk

Prevalite (pravastatin sodium) is a mature, off-patent statin brand with a shrinking commercial base as generics dominate US and global lipid-lowering markets. Financial trajectory depends primarily on (1) residual brand share vs. generic price erosion, (2) formulary positioning for patients requiring pravastatin specifically, (3) net price and rebate structure, and (4) competitor substitution among statins and nonstatins.

What is the current market size and sales trajectory for Prevalite (pravastatin) vs. generic statins?

Prevalite competes in the broad US HMG-CoA reductase inhibitor category, where generic statins capture the majority of prescriptions. For mature statins, brand sales typically decline to a residual share driven by formulary preferences, tolerability narratives, patient continuity, and payer-specific contracting.

US prescription and spend dynamics

Key forces shaping brand trajectory in statins:

- Generic substitution: Pravastatin is widely available as inexpensive generics, reducing payer incentives to cover a higher-cost brand.

- Net price compression: Brand manufacturers face sustained rebate pressure, leaving smaller gross-to-net spreads over time.

- Formulary tiering: Some payers maintain coverage pathways for certain statin brands (often as preferred options within a narrow formulary). This can preserve limited revenue even when generics dominate.

- Clinical switching: Many patients can be switched between statins without clinical detriment, increasing substitution risk.

Where brand share can persist

Prevalite’s residual performance is usually tied to:

- Patient-specific tolerability: Some patients remain on a historically tolerated statin rather than switching.

- Contracting and PBM status: Inclusion on preferred lists can temporarily stabilize volume, then erode as contracts change.

- Geography and distribution mix: Channel mix (mail, retail) and regional contracting affect net sales.

When does Prevalite lose exclusivity and what drives generic entry risk today?

For an established statin brand, the exclusivity and IP timeline is dominated by patent expiry, settlement-driven earlier entry windows in the past, and the practical reality that pravastatin generics already exist at scale in the market.

Patent exclusivity vs. practical market exclusivity

Even if formulation or method-of-use patents existed historically, the commercial market now behaves as an off-patent product:

- Generic availability is already entrenched.

- Switching to generics reduces brand pricing power.

- Any remaining brand advantage is contracting-based, not exclusivity-based.

What typically happens to brand economics post-patent

- Volume declines first, then net price declines.

- Brand manufacturers often shift to cost reductions, smaller marketing budgets, and tighter payer contracting to defend residual share.

What patents protect Prevalite (pravastatin) and how many are still relevant?

Prevalite’s relevant patent estate is largely historical and informational for litigation and legacy brand defense rather than a barrier to current generic pravastatin supply.

Patent estate structure for classic small-molecule brands

For statin brands, the patent landscape typically spans:

- Active ingredient / core composition

- Drug substance and polymorph/crystal form

- Formulation and tablet composition

- Method-of-use claims (e.g., lipid-lowering indications)

- Manufacturing and process claims

In mature markets, composition and method-of-use exclusivity has generally expired, leaving only potential late-cycle formulation/process claims. In practice, generic pravastatin entry has already occurred, and market access barriers are now limited to brand-specific commercial and regulatory factors rather than core patent blocks.

What is the Orange Book status of Prevalite and which listed patents matter commercially?

Prevalite is listed in the FDA Orange Book because it is an approved drug with listed patents. For an established statin brand, the key commercial question is whether any listed patents remain enforceable and whether any exclusivity periods still apply.

Orange Book interpretation for off-patent brands

For current market dynamics:

- If listed patents are expired or no longer enforceable, the Orange Book status does not block generic competition.

- If any listed patents remain active, they typically affect only specific generic applicants or specific label/carve-out positions, not the overall category’s ability to supply.

Featured-snippet answer

Orange Book status for Prevalite is not typically a gating factor today because multiple pravastatin generics already compete broadly. Residual brand economics are therefore driven by payer contracting and net pricing, not regulatory exclusivity.

Which companies sell pravastatin competitively and how does their pricing affect Prevalite sales?

The pravastatin competitive field is dominated by generic manufacturers plus a limited number of legacy brand prescribers. Generic players typically win on price, PBM contracting, and package availability.

Competitive levers that drive net price

Generic competitors usually secure:

- Preferred formulary status via PBM negotiations.

- Lower net cost that supports higher patient adherence.

- Distribution reliability and broad NDC coverage that makes switching frictionless.

Brand counter-levers that can still work

Prevalite can retain limited share if:

- A payer has an older contract that still places Prevalite on a favored tier.

- A patient population is stable on a specific pravastatin dose and formulation.

- There is short-term supply or NDC availability advantage for the brand in certain channels.

How does Prevalite compare with other statins (atorvastatin, rosuvastatin, simvastatin) on market pressure?

Statins compete as class substitutes. Market pressure is strongest from:

- atorvastatin (high use, often preferred in formularies),

- rosuvastatin (strong outcomes narrative and potency),

- simvastatin (generics and older utilization patterns).

Substitution dynamics

- Patients and prescribers often switch within the statin class, creating a high cross-elasticity.

- If a payer prefers a different statin, Prevalite volume typically declines unless a patient is already on the brand.

Why pravastatin can still hold a niche

Pravastatin’s niche often includes:

- patient-specific tolerability profiles,

- clinical practice habits in certain prescribing communities,

- historical continuity where prior failures or side effects restrict switching.

In aggregate, the niche is not large enough to counteract generic price advantages across the category.

What pricing and rebate dynamics shape Prevalite’s financial trajectory?

For off-patent brands, the dominant determinant of financial trajectory is net revenue per unit, not list price.

Typical off-patent brand economics

- Gross-to-net erosion increases over time as payers demand larger rebates.

- Brand marketing spend often shifts from growth to defense.

- Revenue becomes sensitive to:

- rebate re-contracting cycles,

- PBM formularies,

- 340B and channel mix,

- copay program changes (if any remain).

Revenue bridge logic used in forecasting

A standard approach to modeling Prevalite’s revenue trajectory:

- Start with units driven by residual share.

- Apply net price driven by contracting and rebates.

- Apply mix across strengths/dosage forms and channels.

Because generics dominate the category, unit growth is unlikely; most upside is from temporary contracting wins, while downside is usually rebate and share losses.

How do settlements, exclusivity waivers, or Paragraph IV history affect Prevalite now?

For established pravastatin brands, the Paragraph IV era largely set the initial generic entry timing long ago. Current market outcomes are driven more by:

- ongoing generic competition,

- formulary management,

- and recurring payer negotiations.

Litigation history as a commercial factor

Legacy settlements can still matter if:

- they created interim supply arrangements,

- they influenced which label positions or dosages remained brand-favored,

- or they shaped how quickly generic NDC coverage expanded.

But for today’s market, the practical effect is that generic pravastatin supply is already mature, reducing the impact of any single historical settlement.

What regulatory milestones and FDA status affect Prevalite’s supply and competition?

Regulatory factors that can affect brand finances indirectly:

- labeling changes,

- manufacturing site updates,

- shortages or supply interruptions,

- updates to pharmacopeial standards and stability requirements,

- and any changes to FDA-approved REMS (if applicable, though statins generally do not rely on REMS for market access in the way other therapeutic areas do).

Generics vs. brand supply resilience

When shortages occur, brands may temporarily regain volume. In off-patent markets, even temporary shortages rarely restore sustainable unit growth long-term because generics usually re-enter quickly.

What formulation and dosage strengths of Prevalite drive demand and how does that impact revenue?

Pravastatin products exist across multiple strengths. Revenue trajectory depends on:

- which strengths are maintained on formularies,

- whether generics cover all strengths uniformly,

- and whether payers prefer specific dose forms or package sizes.

Strength and mix sensitivity

Brand net sales can swing when:

- a favored strength becomes less favorably contracted,

- PBM switches preferred generics,

- or a dose-specific prior authorization is introduced for patients on alternative statins.

What generic entry risks exist for Prevalite brand (NDC-level or carve-out risks)?

Even after initial generic entry, NDC-level dynamics can still change:

- a new generic filer may enter an unfilled strength,

- a label carve-out can prompt payer switching,

- or supply improvements by generics can eliminate brand’s short-term defense.

However, for a statin with broad generic availability, these events are usually marginal versus the continuing structural pressure from low-cost generics.

What does the competitive landscape look like by geography for Prevalite?

Most off-patent statins face similar patterns globally:

- generics capture baseline volume,

- brand persists in pockets via reimbursement idiosyncrasies,

- and price regulation in some markets intensifies erosion.

US is typically the primary driver of global brand valuation, given higher unit economics and the dominance of PBM and formulary contracting.

How strong is the patent estate for Prevalite and what does it mean for revenue defense?

For a mature statin brand, the patent estate strength generally matters only if:

- any enforceable claims remain that bar certain generic compositions/processes,

- or if a late-cycle patent creates a narrow barrier for specific product configurations.

Commercially, brand defense is usually not patent-led in this category; it is contracting and residual patient continuity. As a result, even a modest remaining patent pocket rarely reverses the structural downtrend once multiple generic products are established.

Key financial trajectory summary: what should investors and planners model for Prevalite?

A realistic planning model for Prevalite assumes:

- continued erosion of unit share vs. generics,

- net price declining or flat-to-down depending on rebate renegotiations,

- volume stability only if formulary status remains favorable for residual patients,

- minor variability due to channel mix and supply events.

Downside scenarios are driven by:

- PBM formulary changes,

- larger rebate demands,

- broader generic NDC coverage for specific strengths,

- substitution to higher-usage statins (atorvastatin/rosuvastatin) within preferred tiers.

Upside scenarios are generally limited to:

- temporary supply gaps by generics,

- short-lived payer contracting advantages,

- and patient continuity within stable prescriber cohorts.

Key Takeaways

- Prevalite is a mature pravastatin brand facing structural decline as generic pravastatin dominates.

- Financial trajectory is primarily driven by formulary contracting and net price, not enforceable exclusivity.

- Competitive substitution among statins (atorvastatin/rosuvastatin) increases brand vulnerability.

- Remaining revenue is best modeled as residual share defense with declining long-term unit economics.

FAQs

1) Why do payers still cover Prevalite when generic pravastatin is available?

Residual formularies, preferred-tier contracts in select cases, and patient continuity where switching is avoided can sustain limited coverage.

2) Does Prevalite performance depend more on rebates or on prescription volume?

Both matter, but for off-patent brands the structural volume decline shifts the center of gravity to net price compression and unit share erosion.

3) Could drug shortages temporarily increase Prevalite sales?

Yes. If generics face supply constraints, brand units can rise temporarily, but sustained gains require durable contracting and re-stabilization of brand supply.

4) Is there a meaningful late-cycle patent risk that could change generic competition?

In mature statins, late-cycle risks are typically narrow. Current market behavior is dominated by entrenched generic availability rather than a single remaining blocking patent.

5) Which statins most directly substitute for Prevalite in formularies?

Atorvastatin and rosuvastatin usually exert the strongest substitution pressure due to high utilization and frequent preferred placement.

References

- US FDA. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. Accessed 2026-06-14.

- US FDA. Drug Approval Package for pravastatin products (Prevalite listings). Accessed 2026-06-14.

More… ↓