Last updated: July 12, 2026

Pentasa (mesalamine) market dynamics and financial trajectory: sales, exclusivity risks, competitive landscape, and patent pressure

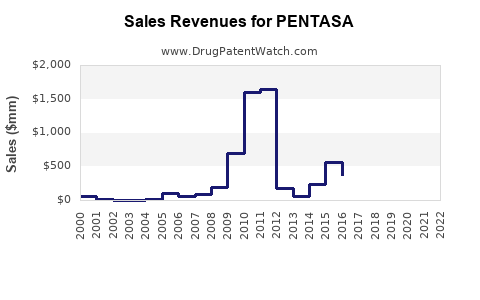

Executive summary: Pentasa (mesalamine) generated sustained global demand for ulcerative colitis and Crohn’s disease maintenance, but its long-term financial profile has been shaped by (1) loss or erosion of exclusivity in key markets for mesalamine formulations, (2) intense generic and branded-formulation competition in 5-ASA, and (3) payer-driven substitution toward lower net-cost products. Pentasa’s revenue trajectory is therefore dominated less by blockbuster inflection and more by share retention, channel mix (pharmacy vs institutional), and ability to defend differentiated delivery mechanics (extended-release beads/tablets) versus low-cost generics.

How has Pentasa performed financially and what is the sales trajectory for mesalamine?

Featured snippet answer: Pentasa’s financial trajectory has been steady-to-declining in many markets as mesalamine formulations face generic substitution, with performance depending on regional patent/enforcement history, channel contracting, and formulation-level differentiation.

Key commercial drivers

- Indication breadth: Ulcerative colitis and Crohn’s disease (notably ileal/colonic involvement) supports recurring maintenance demand and steady refill cycles.

- Chronic therapy economics: 5-ASA chronic use reduces churn but increases pressure on net price.

- Payer substitution: Formularies increasingly prefer “A-rated” generic mesalamine products unless branded delivery has payer-recognized value.

- Competition across 5-ASA delivery types: Extended-release, delayed-release, and multi-matrix bead systems compete on dosing convenience, symptom control, and tolerability.

What market participants generally underwrite

- Net sales rather than list price: Pentasa’s realized pricing is shaped by rebates, contract pharmacy discounts, and tender outcomes.

- Growth vs mix shift: When volume declines due to generic substitution, share recovery is usually limited to narrower patient segments or specific payer contracts.

- Therapy switching behavior: Patients and clinicians are less likely to change during stable remission, but once a cheaper equivalent is established on formulary, migration accelerates.

What patents protect Pentasa (mesalamine) and how long does exclusivity last?

Featured snippet answer: Pentasa’s IP landscape is typically formulation- and process-oriented for specific extended-release delivery platforms, with earlier core chemical or composition protections largely exhausted. Real-world exclusivity is determined by jurisdiction-specific formulation patents plus any patent term extensions and regulatory exclusivity attached to specific product approvals.

Where exclusivity pressure comes from

- Generic and follow-on product entry: In the US, generic mesalamine products have historically entered across multiple oral and rectal formats, often before current-branded product lifecycle milestones would protect demand.

- Formulation fragmentation: Even within mesalamine, distinct delivery technologies (beads, tablets, granules, pH-dependent coatings) create multiple patent clusters. Each can fall independently, enabling partial-to-full generic replacement.

- Paragraph IV and litigation risk: Where US patents still list in Orange Book for a given Pentasa presentation, it can trigger Hatch-Waxman litigation and settlement-driven delay. Where no enforceable patents remain, entry tends to be immediate.

Patent estate mapping approach (how the market values it)

- Steer by jurisdiction and presentation: Pentasa is sold as specific dosage forms and strengths, so patent listings must be evaluated by NDC/presentation, not only brand name.

- Separate drug substance vs delivery systems: For business outcomes, the enforceable portions are usually the delivery system and manufacturing process patents tied to the specific product.

What is the Orange Book status of Pentasa and which patents drive generic entry timing?

Featured snippet answer: Pentasa’s Orange Book listings govern US generic substitution timing at the product-presentation level. When the last listed patent covering a presentation expires or is carved out via settlement, generics can launch once regulatory requirements are satisfied.

What to look for in Orange Book-driven dynamics

- Patent type: Composition and method-of-use patents affect different launch triggers than formulation patents.

- Expiry sequencing: If multiple patents list, the “last expiring” relevant patent determines the practical barrier unless a generic challenges and wins early.

- Oral vs rectal coverage: Pentasa spans specific oral formulations; other mesalamine brands have different rectal systems that alter competitive mapping.

How Orange Book status translates into financial outcomes

- Settlement-driven delay: When settlements occur, branded revenue can be protected temporarily by agreed launch dates and market allocation.

- Carve-out entry: If generics are permitted entry for certain strengths or presentations, revenue erosion can be immediate in targeted SKUs.

- Payer behavior can move ahead of IP: Even if IP delays certain entries, payers can build long-term preferred status for lower-cost alternatives in advance of launch.

Which generic competitors or branded-formulation rivals pressure Pentasa’s market share?

Featured snippet answer: Pentasa faces sustained competitive pressure from generic mesalamine products and other branded 5-ASA delivery systems that are priced below or close to branded net costs, with formulary placement determining the magnitude of erosion.

Competitive set logic for 5-ASA

- Within-molecule generic: Multiple ANDA products compete directly as therapeutically equivalent mesalamine.

- Delivery differentiation: If an alternative branded formulation has strong payer pull or has better outcomes in a segment, it can take volume even when generic mesalamine exists.

- Placebo-like differentiation is rare: In 5-ASA, clinical differentiation tends to be modest versus strong cost signals, so the “default” competitive advantage goes to formulary and net price.

Where Pentasa’s differentiation can matter commercially

- Dosing regimen adherence: Patients and prescribers favor formulations that maintain remission with manageable pill burden and perceived efficacy.

- Patient phenotype fit: Some patients respond better to specific release profiles or anatomical targeting (e.g., distal vs proximal coverage).

- Switch resistance: Clinician and patient inertia can delay switch rates even after generic availability.

When do generic entry risks emerge for Pentasa and what does a launch timeline look like?

Featured snippet answer: Generic entry risk rises after the effective expiry of the last enforceable presentation-specific patent and any statutory exclusivity windows. The financial impact often begins earlier through stocking and payer formulary updates, then accelerates at launch.

Generic launch timeline typical for mesalamine brands

- IP step-down: As listed patents approach expiry, challengers finalize ANDA readiness and wholesalers pre-position.

- Pre-launch contracting: Payers negotiate pricing with generics, and prescribers see formulary status changes.

- Launch and substitution: Once approval and exclusivity constraints end, pharmacy claims shift quickly, especially for maintenance therapy.

Settlement scenario vs no-settlement scenario

- With settlement: A delayed generic launch can preserve branded volume for an additional period, but not necessarily at full original price because payers re-rate the product during the delay.

- Without settlement: Claims migration begins at first approved generic launch, typically causing a sharp net sales decline.

How does Pentasa compare with other mesalamine brands and delivery systems on market power?

Featured snippet answer: Pentasa’s competitive profile is determined by its specific delivery technology and payer positioning relative to both generics and competing branded formulations. In many settings, branded differentiation does not fully offset generic-driven net price pressure once exclusivity falls.

Comparison dimensions used by payers and formularies

- Net cost vs clinical equivalence: If generics are available at large discounts, payers treat branded value as limited unless a niche outcome advantage is recognized.

- Formulary tiers and prior authorization: Prior authorization requirements can slow substitution and protect share temporarily.

- Patient services: Support programs can influence persistence but rarely reverse long-term substitution once payer status changes.

Commercial outcome pattern in mature 5-ASA

- Stable demand with declining net revenue per unit after generic diffusion.

- Share retention for brands that keep favorable formulary status and maintain physician preference in specific segments.

What patent litigation affects Pentasa and how do settlements change business outcomes?

Featured snippet answer: Pentasa-related litigation typically involves ANDA challenges to formulation and manufacturing patents and may resolve through settlements that delay launches or limit which strengths/presentations can be marketed by the generic.

Business impact channels

- Launch date control: Settlements can shift financial outcomes by controlling when the first generics enter.

- Design-around outcomes: If generics avoid infringement via formulation changes, their entry may occur sooner or with broader SKU coverage.

- Re-auctioning risk: After an entry settlement, payers re-open contracting, compressing net prices even before full generic diffusion.

What regulatory status and FDA pathway issues matter for Pentasa market dynamics?

Featured snippet answer: Pentasa’s US competitive environment is shaped by FDA approval pathways for generics (ANDA) and by which specific product presentations are covered by relevant patents listed for those NDAs.

Why FDA pathway matters commercially

- ANDA triggers and timing: Generic launch depends on FDA approval plus resolution of patent constraints tied to Orange Book listings.

- Interchangeability and substitution: Pharmacies substitute based on approved therapeutically equivalent status and payer rules, accelerating net sales erosion once barriers clear.

Which global markets have the highest revenue sensitivity to generic substitution for Pentasa?

Featured snippet answer: Markets with earlier generic penetration, weaker branded enforcement, or aggressive payer substitution exhibit the largest revenue sensitivity. Mature EU and non-US markets typically show higher substitution rates than markets with later enforceable patent term.

Drivers by geography

- Reimbursement design: Hospital vs outpatient reimbursement and tender structures strongly influence substitution speed.

- Patent enforcement rigor: Availability and enforcement strength of formulation patents determines effective exclusivity duration.

- Local generic ecosystem: Number of qualified ANDA equivalents and pricing intensity drive how quickly branded share erodes.

How resilient is Pentasa’s revenue under biosimilar-like substitution dynamics in 5-ASA?

Featured snippet answer: Unlike biologics, Pentasa is not affected by biosimilar competition; however, substitution dynamics across mature oral small molecules can create similar “winner takes net share” outcomes once IP barriers fall.

What substitutes for biosimilar risk here

- Generic price compression: The primary driver is net price compression and formulary displacement.

- Therapeutic class switching: Patients can switch within 5-ASA without biologic-style immunogenicity concerns, increasing migration.

- Contract renewal leverage: Payers can reprice annually; brands with weaker formulary leverage see faster erosion.

Key revenue exposure: where does Pentasa face the steepest financial downside?

Featured snippet answer: The steepest downside occurs in jurisdictions and presentations where the last protectable formulation patents have already expired or where patent settlements have enabled early generic entry, leading to rapid pharmacy claims substitution.

Downside map (commercial logic)

- Oral extended-release presentations: Highest exposure where multiple generics are available and payer policies allow automatic substitution.

- Higher-strength SKUs: Sometimes face slower substitution if packaging-specific barriers exist, but volume often follows across strengths with formulary normalization.

- Rectal formulations: If in-scope presentation-specific IP is weaker, they can be replaced quickly, though Pentasa’s brand association is more prominent in oral systems.

What are the most likely future market scenarios for Pentasa?

Featured snippet answer: The dominant scenario is continued share dilution with modest volume protection at best, unless new enforceable formulation IP or clinically compelling differentiation secures durable payer access.

Scenario structure

- Base case (most likely): Gradual share loss to generics, net price compression, and flat-to-declining net sales in mature markets.

- IP outperformance case: Remaining formulation patents plus effective litigation delay extend branded share, but payer contracting still compresses net price.

- Competitive shock case: A concentrated entry by multiple low-cost generics can accelerate share erosion and worsen net price recovery.

Key Takeaways

- Pentasa’s long-term financial trajectory is primarily driven by generic substitution and payer net-price pressure, not by sustained exclusivity typical of newer therapeutic classes.

- Exclusivity and patent protection are presentation- and jurisdiction-specific, so the practical barrier is the Orange Book-listed, enforceable formulation or process IP tied to specific dosage strengths.

- Orange Book status, Hatch-Waxman litigation, and settlement outcomes determine the timing of generic launch and thus the shape of revenue decline or protection.

- Competitive resilience depends on formulary access, channel contracting, and delivery-system preference, which can slow but rarely prevent erosion once generics are widely adopted.

FAQs

- What dosage forms of Pentasa face the highest generic substitution risk?

- How do Paragraph IV challenges typically affect mesalamine brand revenue after settlement?

- Does payer tiering change faster than patent expiry dates for Pentasa?

- Which factors influence physician and patient willingness to switch between mesalamine extended-release formulations?

- How does FDA approval timing for ANDAs translate into real-world pharmacy claims shifts for 5-ASA?

References

- FDA. “Approved Drug Products with Therapeutic Equivalence Evaluations (Orange Book).” U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/index.cfm

- FDA. “Hatch-Waxman Act and the ANDA Approval Pathway.” U.S. Food and Drug Administration. https://www.fda.gov/drugs/abbreviated-new-drug-application-anda