Last updated: April 23, 2026

How does the market for mometasone furoate move, product-by-product?

Mometasone furoate (MF) is a top-tier, long-established corticosteroid used across allergic and inflammatory indications, with demand anchored by (1) entrenched branded and generic intranasal therapies, (2) low incremental switching costs because many products are considered interchangeable by prescribers, and (3) ongoing share transfer to generics as patents and exclusivities expire. The market structure is typically: brand launches or line extensions in specific dosage forms, then sustained generic pressure once exclusivity ends, with pricing and margin compression followed by stabilization at low net price levels.

Key demand drivers

- Chronic seasonality and long-tail use: Allergic rhinitis and related inflammatory conditions create recurring seasonal demand plus physician-driven chronic control in a subset of patients.

- Multiple administration routes: Intranasal and topical formats diversify channels and mitigate single-form volatility.

- Formulation substitution: Patients and clinicians often treat within-class alternatives as therapeutically similar, shifting purchases toward the lowest net price.

Key supply and pricing mechanics

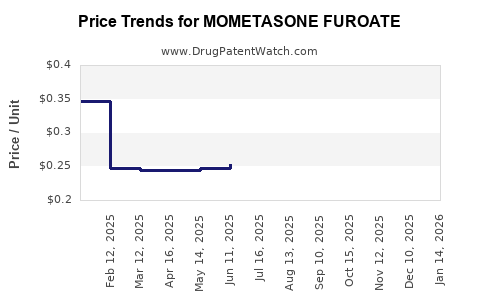

- Generic share growth: MF faces persistent generic entry in most geographies for several dosage forms. The economic pattern is faster generic penetration leading to reduced average selling prices (ASPs).

- Channel effects: Pharmacy benefit design and payer preferences often accelerate substitution to the lowest-cost equivalent.

- Line extension cadence: Companies maintain volume through reformulations, device changes, and combination products, but these typically do not fully reverse generic gravity.

What do the revenue and profitability trends show for mometasone furoate?

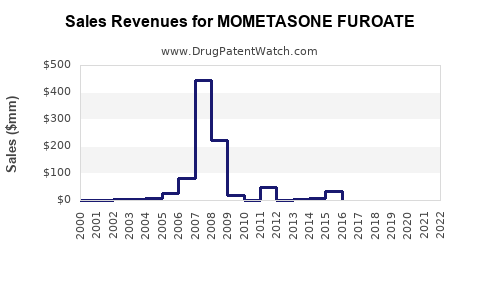

MF’s financial trajectory is best characterized as “volume-led, price-down” after generic entry. The market typically follows a two-phase pattern:

1) Pre-generic / exclusivity period

- Higher net price and margin profile.

- Stable market share due to established prescriber habits and patient familiarity.

- Limited competition from immediate equivalents.

2) Post-generic / broad substitution period

- Sharp decline in net price as branded share erodes.

- Gradual stabilization as the market becomes dominated by a small set of generic manufacturers and continued payer-driven substitution.

- Remaining profitability concentrates in efficient manufacturing, packaging, and distribution scale.

What to expect financially in most MF product lines

- Revenue: tends to hold up better than price due to recurring use, but growth is usually modest and driven by population and utilization rather than pricing power.

- Gross margin: compresses materially after widespread generic entry.

- Operating cash flow: often stays positive given low R&D intensity relative to novel drugs, though working capital and promotional spend can swing by cycle.

How do patent and exclusivity events typically reshape the curve?

MF products are subject to the usual interlocking ecosystem: composition-of-matter coverage, formulation/delivery patent families, and regulatory exclusivity in the form of Hatch-Waxman protections for U.S. generics (through Orange Book-listed exclusivities where applicable) and analogous protections elsewhere. Once exclusivity expires for a specific presentation (dose form, strength, device), the market usually shifts quickly to generics and resets pricing.

Practical dynamics

- Event-driven declines: Revenue drops cluster around the start of generic competition for each dosage form.

- Share redistribution: Generic share often consolidates among high-volume distributors and manufacturers with reliable supply and competitive pricing.

- Brand response: Brands typically reduce promotional spend post-loss of exclusivity and focus on remaining defensible niches (device differentiation, patient support programs, or combination products).

Where does the money concentrate: formulations and indications?

MF is sold in multiple dosage forms that affect reimbursement and payer behavior differently:

Common monetizable MF categories

- Intranasal corticosteroids: High-volume chronic/seasonal demand with strong formulary management.

- Topicals (dermatology): More fragmented geography and payer rules; often faster to genericize due to formulation similarity and easier substitution at the pharmacy counter.

- Combination products (where available): Can sustain revenue longer because switching costs rise, though these are usually smaller than pure MF segments.

Implication for financial trajectory

- Intranasal generally anchors revenue base due to persistent utilization.

- Topical often experiences sharper price competition but can maintain volume with adequate reimbursement.

How do payer and pharmacy dynamics affect net pricing?

Mometasone furoate’s pricing trajectory is tightly linked to formulary placement and pharmacy substitution:

- Formulary tiering: Once an MF product is relegated to a lower tier or replaced by a preferred equivalent, demand shifts quickly.

- PBM contracting: PBMs often drive net pricing down through mandatory rebates and competitive bidding.

- Therapeutic interchange: Clinicians and plans treat many intranasal corticosteroids as functionally substitutable, pushing MF toward lowest net cost.

Result: the market’s dominant financial feature is net price compression, with revenue largely supported by utilization.

What are the cost, manufacturing, and supply-chain realities?

MF is a mature molecule with a well-established manufacturing footprint. Financial outcomes tend to depend on:

- Scale manufacturing economics: cost per unit falls as volumes rise for generic producers.

- Quality systems and regulatory compliance: expensive but stable barriers once products are on the market.

- Distribution logistics: low complexity compared with biologics; supply chain disruptions typically cause temporary disruptions rather than lasting market structure shifts.

For investment and R&D planning, that means MF is generally not a margin story built on innovation; it is an execution story built on cost, supply reliability, and payer access.

What does the U.S. regulatory framework imply for competitive entry?

MF products in the U.S. sit within the Orange Book ecosystem and Hatch-Waxman pathway for generics. Competitive entry timing is controlled by the listed patents and exclusivities for the specific listed drug product (drug, strength, dosage form, and manufacturer). Once those protections end, generic entry becomes a deterministic factor for pricing pressure.

Practical consequence

- Pricing trajectories in most MF presentations are less sensitive to clinical differentiation and more sensitive to regulatory event windows for each product listing.

Source: FDA Orange Book for listed drug protections and FDA-reviewed generic pathways. [1]

Financial trajectory map (market-style model for MF)

Below is a structural view of what investors and business planners typically observe across MF dosage forms after exclusivity windows close.

| Phase |

Typical market state |

Revenue trend |

Net price trend |

Competitive intensity |

| Exclusivity tail |

Brand holds share; fewer close equivalents on preferred tiers |

Stable to modest growth |

Higher net price |

Moderate |

| Generic entry |

Multiple ANDA products launch; substitution accelerates |

Slower growth or decline |

Sharp decline |

High |

| Post-entry stabilization |

Market consolidates among efficient suppliers |

Flat to modest growth |

Low, stable |

Medium-high |

| Line extension offset |

Device/formulation/combination supports niche |

Partial stabilization |

Limited recovery |

Medium |

This pattern aligns with how genericized specialty primary-care products typically evolve, including those in the corticosteroid class within Allergic Rhinitis and dermatology.

What milestones determine forward-looking financial outcomes for MF?

Future financial trajectory is driven less by molecule novelty and more by “market plumbing” milestones:

- Loss and expiry of listed protections per specific MF presentation (strength, dosage form) in each geography.

- Generic launch execution (timing, supply continuity, lot acceptance, and wholesaler coverage).

- Formulary status changes in managed care (tier moves, step edits, preferred product lists).

- Pricing and rebate strategy as PBMs and purchasers renegotiate after generic penetration.

Key Takeaways

- Mometasone furoate’s market dynamics follow a mature specialty model: recurring utilization supports volume while generic substitution drives net price down.

- The financial trajectory is typically “volume-led, price-down,” with margins compressing after exclusivity losses per dosage form.

- Forward outcomes depend primarily on regulatory event timing by product listing and payer contracting behavior, not on clinical differentiation.

- The intranasal segment generally anchors revenue stability, while topical segments often face sharper price competition due to easier interchange and faster payer substitution.

FAQs

1) Is mometasone furoate primarily a growth or decline product?

Post-generic-entry, it behaves like a volume product with pricing pressure. Growth is usually modest and utilization-driven rather than price-led.

2) What most determines net revenue for mometasone furoate?

Net price after PBM rebates and payer preference rules, which are heavily influenced by generic entry and formulary tiering.

3) Does the same financial pattern apply across intranasal and topical MF?

The core “generic substitution pressure” is the same, but intranasal typically holds revenue more steadily while topical pricing often compresses faster.

4) How do patent expirations translate to market share changes?

Once the relevant protections end for a specific product listing, generic entry accelerates substitution and quickly shifts share toward the lowest net-cost equivalents.

5) What is the key business lever for companies with MF products?

Execution on supply reliability and cost competitiveness, paired with payer-access strategy to maintain formulary presence.

References (APA)

[1] U.S. Food and Drug Administration. (n.d.). Drugs@FDA: FDA Approved Drug Products (Orange Book) Search. https://www.accessdata.fda.gov/scripts/cder/daf/