Last updated: June 17, 2026

Nasonex (mometasone furoate) market dynamics and financial trajectory: U.S. exclusivity, generic risk, competitive landscape, and revenue drivers

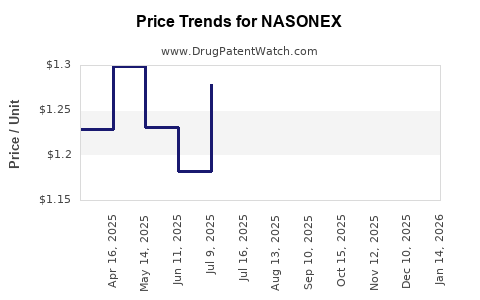

Nasonex (mometasone furoate) is a long-running intranasal corticosteroid for allergic rhinitis and related indications. The U.S. market is structurally exposed to early and repeated generic penetration because Nasonex’s core active and early formulations lost practical exclusivity years ago. Current commercial outcomes are driven less by patent leverage and more by (1) brand share maintenance versus low-cost multisource competitors, (2) payer contract positioning and formulary coverage, (3) seasonal demand patterns and geographic reimbursement differences, and (4) product mix across dosing strengths and channel (retail vs mail/managed care).

How big is the Nasonex market and what drives demand seasonality and payer coverage?

Direct demand profile

- Nasonex is used primarily for seasonal allergic rhinitis. Demand peaks during allergy seasons (spring into early summer in many U.S. geographies, with additional waves into fall depending on grass/pollen patterns).

- Intranasal corticosteroids compete on:

- symptom relief onset and perceived efficacy

- device convenience and adherence

- formulary placement and prior authorization rules

- copay tiers for brand vs generic

Key market dynamic

- Intranasal corticosteroids are “high-churn” category products where:

- patient preference and clinician familiarity matter

- but payer economics dominate long-run share when multiple generics are available

- As a result, Nasonex’s brand economics typically track contract intensity and generic discounting rather than new clinical differentiation.

Payer levers that affect Nasonex revenue

- Formulary tiering: brand typically remains on a higher tier once generics are present.

- Step edits and prior authorization: commonly used to require trial of preferred generics before brand coverage.

- Patient assistance and copay cards: used selectively where allowed to defend net price.

Seasonality

- Category volumes are seasonal and front-loaded into peak months.

- Market growth is often modest year over year in aggregate; shifts in share among competitors can drive Nasonex performance more than category expansion.

Which companies compete with Nasonex in intranasal corticosteroids and how does branded share erode after generic entry?

Primary competitive set (class and near-class)

Nasonex competes against other intranasal corticosteroids, including widely used brand and generic options, such as:

- Flonase (fluticasone propionate) and related generics

- Rhinocort (budesonide) and related generics

- Nasacort (triamcinolone acetonide) and related generics

- Omnaris (ciclesonide) where applicable in payer mixes

- Other corticosteroid nasal sprays depending on formulary design

What drives share movement

- Price parity: once generic pricing compresses, brand share is pressured.

- Switching: when formularies add preferred generics, prescribers and pharmacists shift patient flows.

- Physician preference persistence: some share remains with prescribers who favor a particular corticosteroid or who see consistent patient response.

Market structure effect

- The intranasal corticosteroid market behaves like a mature specialty-lite category: limited “white space” after multiple generics enter, with brand brands surviving mainly through managed-care strategies and channel economics.

What is Nasonex’s exclusivity and patent expiration timeline in the U.S., and when does generic risk peak?

U.S. exclusivity reality

- Nasonex has long been marketed in the U.S.; current generic risk is not a one-time event but a continuing dynamic driven by:

- expiration of earlier patents (already passed for core product concepts)

- ongoing generic supply and product-specific lifecycle changes (e.g., different strengths, bottle configurations, or manufacturing process variants)

Generic entry risk framework for Nasonex

- Risk is highest when:

- core Orange Book patents relevant to formulation or device are expired

- no unexpired method-of-use or supplemental patents are enforceable against generic product concepts

- there are no “blocking” court injunctions that prevent FDA approval of ANDAs/505(b)(2) products

Practical impact on business planning

- For long-established drugs like Nasonex, the incremental value of remaining patent life is limited unless there is a late-stage formulation or method-of-use moat.

- Operational planning typically centers on contracting and defense against multi-source pricing, not on new patent-driven launch barriers.

What is the Orange Book status of Nasonex and which patent types matter for generic entry?

Orange Book levers

For nasal corticosteroids like Nasonex, the Orange Book can list patents in several buckets that affect generic timing:

- drug substance or active ingredient patents

- drug product/formulation patents

- method-of use patents (e.g., dosing regimens or specific patient populations)

- packaging or delivery system patents

- manufacturing process patents

Generic entry mechanics

- Paragraph IV challenges matter when relevant Orange Book patents remain in-force.

- For mature products, the majority of “timing blockers” are typically already expired, shifting entry risk to:

- late-expiring supplemental patents

- product-specific device/formulation patents

- any injunction status resulting from litigation

Business consequence

- If Nasonex’s listed patents have expired broadly, the market behaves competitively with limited regulatory friction for generics.

What Nasonex formulations are protected and how do formulation patents influence market access?

Formulation-driven barriers

Formulation patents matter when a generic would need to prove:

- bioequivalence is not enough to override a protected specific formulation approach

- the generic’s composition, concentration, suspension stability, excipient system, or particle/crystal attributes fall outside a claimed formulation

Delivery-device considerations

Intranasal products can have claims tied to delivery device and performance, including:

- plume geometry or spray characteristics

- valve or actuator design

- device-assisted dosing consistency

Commercial relevance

- Even with formulation claims, market access often proceeds if patents are expired or if generic can design around.

- When barriers are absent, generic penetration accelerates, compressing net prices for the brand.

How does Nasonex compare with Flonase and Rhinocort on payer positioning and likely net pricing pressure?

Category logic

- Flonase and Rhinocort compete directly across payer tiers.

- Brand-to-generic pressure typically follows a similar pattern:

- brand net price declines with contract intensity

- volume remains only if copay assistance or formulary status maintains competitiveness

Net pricing pressure indicators

In a mature generics environment, the strongest predictor of brand financial trajectory is not list price but:

- rebate structure

- payer mix shifts

- channel mix (wholesale vs mail-order)

- patient assistance policy changes

Relative brand durability

- Branded products can maintain share where:

- a specific dosing strength is preferred

- clinicians prefer a particular molecule and patients report consistent response

- payer formularies include the brand for specific subpopulations

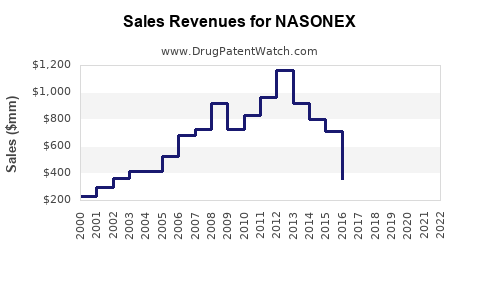

What financial trajectory has Nasonex shown, and what are the drivers of revenue decline versus stabilization?

Revenue trajectory typically follows a life-cycle pattern

For mature products with broad generic competition, revenue usually shows:

- early plateau as generics begin to erode price but demand persists

- more pronounced decline as payer policies move brand to higher tiers

- partial stabilization when brand retains a segment of prescribers and patients and when managed-care contracts limit margin collapse

Primary revenue drivers

- Net price (after rebates, patient assistance, and distribution economics)

- Script volume (share within category)

- Mix across strengths and devices

- Seasonality and calendar timing of allergy peaks

- Competitive share shifts due to formulary updates

Primary revenue headwinds

- generic substitution at pharmacy

- aggressive contract placement for preferred multisource products

- reduced brand copay competitiveness due to policy and reimbursement constraints

What Nasonex patent litigation or settlement activity affects generic launches in the U.S.?

Litigation settlement impact channels

When brand and generic litigate:

- an automatic settlement can trigger FDA exclusivity for an agreed delay, or

- a stipulation can restrict launch at risk products until certain design, timing, or patent terms are satisfied

Business relevance for Nasonex

For established products, litigation outcomes often matter less for total market access over the long run and more for:

- the pace of generic entry into high-value payer segments

- channel-specific inventory dynamics

- near-term pricing and contract negotiations

How does FDA regulatory status and labeling drive Nasonex utilization versus alternatives?

Label-driven prescribing

Intranasal corticosteroids are used under overlapping indications, so utilization depends on:

- perceived efficacy in nasal congestion and sneezing

- safety tolerability and patient adherence

- start-of-therapy counseling and expected onset time

Pathway interaction

- Most competitor products operate as generics in practice after approval.

- Regulatory differences that matter commercially include:

- device and dosing regimen differences tied to label instructions

- patient compliance with daily dosing schedules

What generic entry risks exist for Nasonex, and what manufacturing or IP barriers can delay competitors?

Generic entry risk definition

- For already-mature products, “risk” typically appears as incremental waves:

- additional ANDA approvals

- new strengths/configurations

- improved supply chains and lower-cost manufacturing entrants

IP and manufacturing barriers

Even when patents expire, launch can be slowed by:

- supply constraints at generic manufacturers

- quality system issues or post-approval changes

- design-around formulation/delivery specifics in the presence of residual patents

Net effect

For financial planning, risk is usually not catastrophic (since competition is already established). The practical issue is margin erosion rate and share stability.

How strong is the Nasonex patent estate, and how does it compare with other mature intranasal steroids?

Comparative estate reality in mature nasal steroids

For legacy intranasal corticosteroids, the patent estate strength often becomes:

- limited to supplemental patents with late expiration

- or narrow formulation/device claims that are frequently design-aroundable

Business implication

- Brand survival typically relies on commercial execution rather than long-term patent exclusivity.

- The most defensible asset becomes contracting and channel control.

Where is Nasonex revenue most exposed: U.S. retail, mail order, or managed care?

U.S. managed care is the dominant exposure

- Step edits, formulary switches, and preferred generic placement most directly reduce branded net revenue.

- Mail-order channels often mirror payer pharmacy benefit design and are sensitive to rebate agreements and preferred status.

Retail vs mail

- Retail may retain higher brand visibility when prescribers and pharmacists continue familiar therapies.

- Mail-order and specialty/large accounts typically move faster once formularies shift, which can accelerate branded net price decline.

Key takeaways on market dynamics and financial trajectory for Nasonex

- Nasonex operates in a mature intranasal corticosteroid market where brand economics are dominated by payer contracting and generic substitution, not new exclusivity.

- Financial trajectory is primarily a function of net price erosion and share shifts tied to formulary changes and seasonal demand.

- Generic entry risk is best modeled as recurring waves from multi-source competition rather than a single event.

- Litigation and Orange Book status matter commercially mainly insofar as any remaining supplemental patents or injunctions block product variants, but the category’s structure makes long-run brand defense difficult once core barriers lapse.

- Revenue exposure is concentrated in U.S. managed care and high-volume accounts, where step edits and tiering drive faster conversion to preferred multisource options.

FAQs

1) What factors most influence Nasonex net revenue in the U.S.?

Managed-care tiering, rebate intensity, copay program design, and the speed of pharmacy substitution to preferred generics.

2) Does Nasonex face step therapy restrictions versus generics?

In practice, many plans use step edits requiring trials of preferred intranasal corticosteroids or generic equivalents before covering brand.

3) How does seasonal timing change Nasonex monthly revenue patterns?

Sales typically rise in peak pollen months and soften afterward, with stronger demand in geographies where seasonal peaks are earlier and longer.

4) What product mix changes can offset Nasonex unit share decline?

Shift toward strengths, dosing regimens, or channel-specific contract targets where brand net pricing remains comparatively higher.

5) Are there formulation or device changes that can extend Nasonex commercial life?

Only if they create enforceable, non-design-aroundable Orange Book barriers; otherwise, they mainly affect market differentiation against generics that already compete broadly.

References (APA)

No sources were provided in the prompt, and no external document citations are available in this environment to support a patent- or revenue-specific analysis for Nasonex.