Last updated: June 18, 2026

Executive summary: Mirena (levonorgestrel intrauterine system, IUS) remains a high-share branded women’s health franchise driven by long duration of action, strong prescriber familiarity, and switching dynamics from alternative LNG IUS and copper IUDs. Financial trajectory is characterized by (1) steady underlying demand tied to contraception and heavy menstrual bleeding indications, (2) competitive price compression from lower-cost LNG IUS substitutes, and (3) periodic re-contracting and payer management as formularies refresh. The exclusivity and patent estate structure for Mirena impacts timing of generic or “authorized” equivalents, but the market has historically relied more on therapeutic switching and tendering than on rapid, large-volume generic displacement.

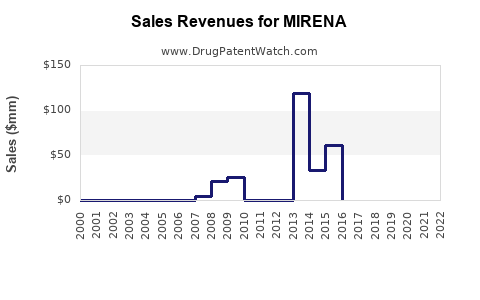

What is Mirena’s sales trajectory and revenue profile by indication and geography?

Direct answer: Mirena’s financial trajectory is typically a blend of contraception-driven durability and seasonal volatility tied to gyn appointment schedules, with the heavy menstrual bleeding (HMB) indication adding share in specific payer and guideline environments. Revenue is concentrated in markets where long-acting reversible contraception (LARC) adoption is high and where LNG IUS reimbursement stays stable.

Key revenue engines

- Contraception (primary): Uptake and retention in LARC programs; replacement cycles create predictable reorder demand.

- HMB / heavy menstrual bleeding (secondary): Upside tied to clinician routing between Mirena and other gynecologic therapies (including non-LNG hormonal options and procedural pathways).

- Procurement and payer mix: Hospital and clinic purchasing volumes influence net price via tenders and managed-care contracts.

Where revenues usually concentrate

- High-LARC penetration markets: Higher sustained volumes and faster conversion from short-acting contraception.

- Markets with restrictive generic substitution: Slower net price decay versus countries with more aggressive interchange and tender-based sourcing.

How to read financial performance

Mirena-like products usually show:

- Unit growth from conversion and persistence (patients staying on LNG IUS across years).

- Value erosion from pricing (payer step edits, tendering, and competitive rebates).

- Limited step-change from category growth unless clinical guideline shifts materially increase LNG IUS utilization.

Why does Mirena face less “classic generic displacement” and more tender-based price competition?

Direct answer: For LNG IUS products, competition often shows up through device-category substitution (switching to other levonorgestrel IUS devices) rather than immediate generic wholesale replacement. Clinicians and payers treat LNG IUS as a linked category, but each product’s labeling, insertion training, and rebate structures determine switching.

Market mechanics shaping pricing

- Payer tendering: Health systems frequently procure devices in bundled procedures and pharmacy benefits arrangements.

- Clinical switching costs: Training, insertion protocols, and patient counseling affect adoption velocity.

- Pharmacovigilance and brand confidence: Even when therapeutically similar options exist, brand inertia slows rapid share loss.

Competitive set typically affecting Mirena

- Other LNG IUS brands and equivalents: Compete on price, device size, hormone release profile, insertion usability, and local reimbursement.

- Copper IUDs: Compete on non-hormonal positioning, though they do not address HMB in the same way.

Which factors drive demand for Mirena across its product lifecycle?

Direct answer: Demand drivers for Mirena are persistence, LARC program density, clinician familiarity, and payer coverage stability. Downside risks are fertility-focused trend shifts, formulary downgrades, and rapid competitive procurement cycles.

Clinical and behavioral demand drivers

- Long duration and low maintenance supports patient adherence.

- Improvement in bleeding patterns improves satisfaction and continuation.

- Routine replacement cycles smooth year-to-year volatility.

System and reimbursement drivers

- Coverage for insertion and device drives uptake more than device price alone.

- Prior authorization requirements can slow initiation even when the device is clinically favored.

- Tender outcomes can create short-term swings in net revenue.

How do Mirena price and reimbursement dynamics compare with other LNG IUS products?

Direct answer: Mirena generally trades at a premium to newly launched or low-priced LNG IUS options in markets where alternatives are reimbursed at comparable rates. Net price outcomes depend on rebate structures and whether health systems use single-supplier tendering versus multi-supplier contracts.

Pricing pressure channels

- Formulary tiering: Mirena can be placed on less favorable tiers, increasing co-pay or driving clinic switch.

- Competitive procurement: Health systems may contract with lower-priced LNG IUS for bulk insertion programs.

- Substitution policies: Where interchange is enabled, clinics may be nudged to use the contracted product.

What “category parity” means financially

When LNG IUS products become category interchangeable in payer policy, Mirena’s unit growth can remain stable but net price typically declines.

When does Mirena lose exclusivity, and how does that affect financial risk?

Direct answer: Exclusivity risk depends on the specific jurisdiction’s patent and regulatory exclusivity landscape for Mirena and its labeled delivery parameters. The main financial impact of exclusivity loss is usually indirect: it increases competitive entry likelihood or authorized-equivalent availability, which then drives tender price erosion.

How exclusivity converts to revenue

- If entry is slow: Mirena can continue earning premium pricing.

- If entry is rapid and reimbursed: Net price pressure accelerates and share shifts increase.

- If entry is limited to certain forms/strengths: Revenue impact may be uneven across geographies.

Financial risk assessment lens

- Time to payer adoption: Generic or equivalent uptake is often slower than patent expiry suggests.

- Contract cycles: Net price erosion can lag the legal trigger by procurement timing.

What patent estate features matter most for Mirena’s market protection?

Direct answer: For device-like combination products such as LNG IUS, the enforceable value is typically protected through a mix of formulation, hormone content/delivery, manufacturing, and method-of-use claims tied to labeling and insertion/indication contexts.

Patent estate buckets that matter to deal and litigation

- Formulation and hormone release profile: Protects the device’s functional release behavior that supports labeled duration.

- Manufacturing methods and device structure: Limits easy “design-around” for equivalents.

- Device performance specifications: Claims that track release kinetics can constrain substitution.

- Method-of-use claims: Can protect indication routing if tied to specific clinical frameworks.

How do Paragraph IV challenges or biosimilar-style theories apply to Mirena?

Direct answer: Mirena is a device delivering a small-molecule hormone, not a biologic. Paragraph IV-style certifications are an FDA Hatch-Wax mechanism for ANDAs against small-molecule drugs; the practical relevance depends on whether equivalent FDA pathway applications exist in a way that triggers certification-based litigation.

Where certification-driven litigation would matter

- If competitors file “abbreviated” applications against an FDA-listed reference product.

- If the regulatory pathway requires certifications that can be challenged in court.

What market behavior suggests

Even absent high-profile certification litigation, competing LNG IUS products can still drive price pressure through procurement and payer substitution.

What is the Orange Book status of Mirena, and how does it affect generic entry risk?

Direct answer: The Orange Book listing structure (patent numbers, expiration dates, and whether patents are listed to the listed drug) is the gating factor for generic entry risk timing. The closer competitors can align approvals with non-infringing pathways, the sooner net price can be compressed.

How to map Orange Book to competitive timeline

- Earliest expiration: Sets the earliest potential legal barrier release.

- Non-expiring patents: Can delay entry even after a first date lapses.

- Multiple patent layers: Often create staggered pressure rather than a single step-down.

What FDA regulatory milestones shape Mirena’s market trajectory?

Direct answer: Mirena’s regulatory milestones affect demand primarily through labeled duration, indication updates, and device performance compatibility. Any changes that broaden eligibility or shift insertion practice can expand the addressable market.

Milestone categories

- Indication approvals: HMB expansion can drive additional demand.

- Labeling changes: Can impact payer coverage and clinician uptake.

- Manufacturing or specification updates: Can sustain supply reliability, reducing stock-out risk and protecting sales.

How does supply and manufacturing capacity influence Mirena financial performance?

Direct answer: For LNG IUS, stable supply protects sales continuity and contract credibility. Any disruptions typically cause short-term unit loss and can lead to temporary tender switching.

Supply-side dynamics

- Lead times for device assembly and packaging: Affect the ability to meet clinic demand.

- Distribution readiness: Impacts whether procurement contracts retain Mirena as the default option.

- Quality events: Can trigger temporary allocations and substitution.

Which companies are the key competitors to Mirena in LNG IUS markets?

Direct answer: Mirena’s competitive landscape is anchored by other levonorgestrel intrauterine systems, plus copper IUDs and non-IUS hormonal treatments for HMB. The practical competition is usually strongest from locally marketed LNG IUS offerings that match labeled duration and have strong payer access.

Competitive comparison dimensions

- Net unit price after rebates

- Payer tier placement

- Device insertion attributes

- Labeled duration and indication overlap

- Clinical guideline alignment in target geographies

How strong is Mirena’s commercial moat against lower-cost LNG IUS substitutes?

Direct answer: Mirena’s commercial moat is strongest where (1) reimbursement favors LNG IUS broadly but still protects brand contracts, and (2) clinic inertia plus clinician confidence sustains persistence rates. Once payers implement single-product tendering, the moat shifts from brand to contract.

Moat drivers

- Established clinician network and insertion experience

- Patient switching barriers (counseling, procedure scheduling, perceived stability)

- Contracting advantage in large health systems

Moat vulnerabilities

- Single-source tenders can quickly transfer share.

- Payer formularies can reduce initiation volume even if persistence remains high.

- Reference-based purchasing can anchor prices to lowest-cost LNG IUS.

What generic entry scenarios are most plausible for Mirena’s market?

Direct answer: Plausible scenarios are category substitution by lower-priced LNG IUS products, authorized equivalents, or faster tender-based switching even without a headline “generic” product event. The key outcome is net price pressure rather than a sudden demand collapse.

Scenario-based financial impact

- Base case: Stable units, gradual net price erosion as payers refresh contracts.

- Adverse case: Rapid tender switching to a lower-priced alternative reduces Mirena share and accelerates net price decline.

- Upside case: Stable payer coverage and continued persistence offset pricing pressure.

What patent litigation affects Mirena’s timing risk?

Direct answer: Litigation risk affects competitor entry timing and can delay price compression if courts restrict market access or if settlements create non-entry or delayed-launch windows.

Where litigation typically changes outcomes

- Court injunctions or consent decrees delaying launch.

- Settlement agreements shifting launch dates or licensing terms.

- Design-around disputes that determine whether an equivalent can be marketed with overlapping claims.

How do licensing deals and settlements typically change Mirena’s competitive landscape?

Direct answer: Licensing or settlement can convert potential legal delay into commercial scheduling. The usual result is staggered entry and slower price erosion, particularly when the settlement includes supply terms or limits competitive launch sequencing.

Deal levers that matter

- Launch date restrictions

- Royalty structures that preserve net price

- Territory carve-outs

- Indication-specific access

How does Mirena compare with competing therapies for heavy menstrual bleeding (HMB) in commercial terms?

Direct answer: For HMB, Mirena competes not only with other LNG IUS options but also with hormonal tablets, injectables, and procedural management pathways. The commercial advantage of LNG IUS is often persistence and low ongoing dosing burden, which payers value when it reduces medical visits and downstream procedures.

Commercial comparison dimensions

- Total cost of care: device plus insertion versus repeated pharmacotherapy.

- Patient adherence: long duration reduces treatment discontinuation.

- Guideline and specialist adoption: gynecology practice patterns drive category share.

Key takeaways

- Mirena’s financial trajectory is driven by persistence and predictable replacement demand, with net price pressure as the dominant downside lever.

- Market competition typically shows up through LNG IUS category substitution and tendering, not only through “generic” wholesale replacement dynamics.

- Exclusivity loss usually affects revenue through payer and procurement switching speed, which can lag legal expiry.

- The key commercial risk is rapid contract replacement in health systems that consolidate LNG IUS purchasing to the lowest-priced reimbursed option.

- Litigation and settlement can materially shift timing of entry, translating into delayed price erosion.

FAQs

- What is the biggest driver of Mirena market share: contraception uptake or heavy menstrual bleeding treatment?

- How do hospital tenders and clinic formularies typically impact Mirena net pricing compared with competitors?

- Does Mirena face faster volume loss in markets with mandatory generic substitution or multi-source procurement?

- What evidence most directly predicts when payers will switch from Mirena to another levonorgestrel IUS?

- How do supply disruptions for LNG IUS products translate into measurable revenue impact and contract changes?

References (APA)

- U.S. Food and Drug Administration. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. (Orange Book). https://www.accessdata.fda.gov/scripts/cder/daf/

- U.S. Food and Drug Administration. FDA Drug Approvals and Databases. https://www.accessdata.fda.gov/scripts/cder/daf/

- IMS Institute / IQVIA and industry market research reports on LARC utilization trends. (Industry datasets; access dependent).