Last updated: June 7, 2026

Lithobid (lithium carbonate) market dynamics and financial trajectory: sales trends, payer pressure, and generic/biosimilar risk

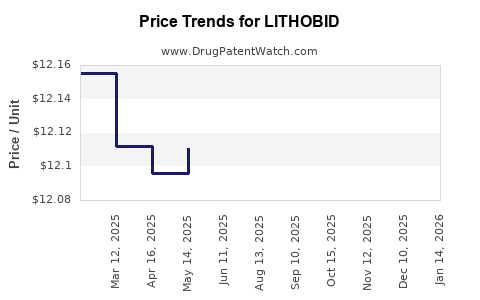

Lithobid (lithium carbonate, extended-release) is a legacy, off-patent psychiatry product with low branded pricing power, limited product differentiation, and sustained competitive pressure from generics. Market dynamics are dominated by (1) long-standing generic availability, (2) payer formulary management for maintenance bipolar disorder, (3) substitution and interchangeability for extended-release lithium carbonate, and (4) revenue sensitivity to patient adherence, tolerability-driven dosing persistence, and site-of-care patterns (psychiatry clinics vs. primary care).

Because lithium carbonate is not a biologic and has no biosimilar class risk, the principal “new entrant” threat is generic and authorized generics, with commercial outcomes determined by net price, pharmacy reimbursement rules, and channel mix rather than by new regulatory exclusivity cycles.

Bottom line: Lithobid’s financial trajectory is shaped less by patent-driven launch timing and more by generic erosion, tight pharmacy reimbursement, and chronic use dynamics that either maintain stable volumes or produce slow decline when payers steer patients to lower-cost equivalents.

Is Lithobid (lithium carbonate ER) still selling meaningfully in 2026, and where does demand come from?

Featured snippet answer: Lithobid demand is driven by chronic maintenance therapy for bipolar disorder and long-term adherence to extended-release lithium carbonate, but branded unit economics erode as generics and authorized generics compete on price.

Where demand concentrates

- Therapeutic area: maintenance treatment of bipolar disorder (classic “mood stabilization” category).

- Use profile: chronic, continuous therapy; patient retention matters more than patient acquisition after stabilization.

- Prescribing setting: psychiatry and mixed primary care-psychiatry management; switching is often driven by formulary step edits and cost.

What sustains volume

- Clinical practice inertia: once a patient is stable on a specific extended-release lithium carbonate regimen, prescribers may resist switching due to tolerability or symptom-control history.

- Dosing discipline: extended-release formulations help with once- or twice-daily adherence, which can influence persistence.

What reduces branded share

- Switching and substitution behavior: pharmacy-level substitution and prescriber substitution to generic extended-release lithium carbonate is common once coverage narrows branded coverage.

- Payer cost controls: formularies typically prefer lower-cost generics and apply prior authorization only sporadically, but the economic baseline favors generic continuity.

What are the key market dynamics affecting Lithobid net sales (price, utilization, channel mix)?

Featured snippet answer: Net sales move mainly with net price erosion from generic pressure and modest utilization shifts driven by bipolar maintenance adherence and switching.

Net price: the dominant lever

- Branded lithium carbonate faces ongoing discounting to maintain coverage.

- Even if some patients remain on-brand, the net price trajectory is compressed by:

- multiple generic entrants,

- wholesaler buying behavior that reflects generic price anchoring,

- pharmacy reimbursement rules and step therapy norms.

Utilization: slow-moving, chronic-demand dynamics

- Bipolar maintenance usage changes gradually with:

- diagnosis prevalence and case detection,

- relapse patterns leading to therapy initiation or discontinuation,

- clinician prescribing norms around mood stabilizers.

Channel mix: specialty vs. retail behavior

- Lithium carbonate is typically dispensed through retail pharmacy with chronic refills.

- Retail dynamics amplify substitution and formulary pressures, which accelerates branded share loss once generic coverage is broad.

When did generic competition erode Lithobid, and how does that timing drive today’s revenue profile?

Featured snippet answer: By the time Lithobid reached the mature-market stage, generic extended-release lithium carbonate supply reduced branded share, producing a revenue profile that is typically stable at first and then gradually declines as payer preferences tighten.

Generic erosion pattern typical for legacy lithium salts

- Early phase: branded share holds due to prescriber familiarity and patient stability.

- Mid phase: payer formularies increasingly restrict brand use to higher-cost exceptions.

- Late phase: branded remains a minority share product, often maintained by coverage exceptions, physician preference in special cases, and patient-level inertia.

Why timing matters for financial trajectory

- Branded revenue often transitions from “growth” to “stabilization,” then to “attrition,” with attrition rate driven by:

- number and pricing of generic suppliers,

- payer rebate intensity,

- persistence on brand (switching friction).

What patent and exclusivity constraints matter for Lithobid’s commercial window?

Featured snippet answer: For legacy lithium carbonate ER, the commercial window is governed by the maturity of the molecule and by the fact that generic manufacturers can use non-reference pathways once Orange Book patent coverage has expired or been cleared.

Practical implications for a branded legacy product

- Once key Orange Book listings for the branded product expire, the market shifts from exclusivity-driven competition to price-and-access competition.

- With chronic use, the post-expiry stage is usually defined by:

- market share transfer to generics,

- ongoing branded discounting to keep access.

What is the Orange Book status of Lithobid (lithium carbonate ER), and how many listings constrain generic entry?

Featured snippet answer: Lithobid is a legacy product where the remaining Orange Book impact is typically limited; generics of lithium carbonate extended-release usually compete without meaningful regulatory exclusivity constraints.

What Orange Book listings generally do in this category

- They can delay generic approval only if still in force and tied to the reference product.

- If those listings are expired, generic competition is primarily a business negotiation rather than a legal/regulatory gate.

Commercial consequence

- For financial forecasting, the key variable is not exclusivity timing but net price trajectory and share loss rate.

How strong is the patent estate for Lithobid, and which IP categories typically remain?

Featured snippet answer: For older small-molecule CNS brands like Lithobid, any remaining IP tends to be limited in scope and does not usually block generic lithium carbonate ER supply.

IP categories that typically show up (and why they matter less)

- Formulation/process claims: may exist but are often bypassed with alternative manufacturing approaches once broad exclusivity expires.

- Method-of-use claims: are less common for generic lithium salts unless tightly drafted and still in force.

- Device/dosing regimen claims: for an established molecule, such claims rarely create a large commercial barrier.

What this means for a competitor strategy

- Generics compete based on:

- AB-rated substitutability,

- manufacturing reliability,

- pricing and contracting.

What Paragraph IV (and other Hatch-Waxman) litigation risk exists for Lithobid?

Featured snippet answer: Litigation risk is low in the ongoing sense for mature legacy lithium carbonate because entry barriers have largely been cleared over multiple years and the market is already served by generics.

How litigation affects financial trajectory when it occurs

- When a brand faces a new generic challenge, near-term branded revenue can spike or drop depending on settlement outcomes.

- For a product already widely available in generic form, subsequent entrants generally have less impact because the market is already competitively fragmented.

How do payer and reimbursement policies affect Lithobid’s brand-to-generic substitution?

Featured snippet answer: Coverage rules typically favor generics for chronic maintenance drugs, pushing branded Lithobid into exception-based use.

Payer levers

- Formulary tiering: brand typically higher tier than generic.

- Prior authorization and step therapy: may appear for brand access, even if not universal.

- Copay design: can create patient-level switching or nonadherence if brand copays are higher.

Net sales impact

- Net sales typically track:

- branded share after formulary changes,

- rebate and discount practices to preserve coverage,

- patient persistence.

What generic entry risks exist for Lithobid and how do they change the outlook by revenue line?

Featured snippet answer: The main risk is further price compression from additional generic entrants and broader authorized generic contracting, which can drive net revenue down even if prescription counts hold.

Revenue line behavior for legacy brands

- Units decline more slowly than gross margin: payers reduce net price faster than they reduce volume.

- Wholesale buying cycles: can shift demand toward the cheapest available supply.

- Seasonality: lithium therapy is chronic; seasonality is usually muted.

How does Lithobid compare with other lithium carbonate extended-release products (commercially and competitively)?

Featured snippet answer: Lithobid competes most directly with AB-rated generics of lithium carbonate extended-release and other lithium formulations. Competition is primarily price and coverage, not clinical differentiation.

Competitive set characteristics

- Same active ingredient: lithium carbonate ER, AB-rated.

- Substitution likelihood: high when payer policies allow interchange.

- Differentiation levers: typically packaging, pill strength availability, and perceived tolerability, but prescriber-level preference declines as coverage tightens.

What “market share” means here

- Brand share is often a function of:

- prior patient history,

- regional contracting,

- pharmacy switching patterns.

What financial trajectory should investors model for Lithobid-style legacy CNS brands?

Featured snippet answer: A typical model is long-run volume stability with persistent net price erosion, producing gradual revenue decline and margin pressure driven by rebates, channel contracts, and share loss.

Modeling framework (practical)

- Net sales = unit volume x net price.

- Unit volume: tends to decay slowly in mature chronic therapies.

- Net price: declines faster due to:

- formulary pressure,

- competitive contracting,

- rebate re-optimization to retain access.

Key sensitivities

- Payer contracting changes: can accelerate share loss.

- Generic pricing floor: new generic supply can push net price down quickly.

- Patient persistence: tolerability and relapse prevention improve persistence and blunt volume decline.

Key Takeaways

- Lithobid’s market dynamics are dominated by generic and payer-driven price compression rather than exclusivity cycles.

- Demand is chronic and adherence-dependent, which supports slower unit erosion but does not prevent branded net price decline.

- The competitive risk is continued price pressure from additional generic entrants and authorized generics.

- Financial trajectory for Lithobid-like legacy CNS brands typically shows gradual revenue decline with persistent margin pressure, driven by net price and coverage access more than by utilization spikes.

FAQs

1) What drives prescription persistence on Lithobid versus generic lithium carbonate ER?

Persistence is most often driven by patient stability, tolerability history on the specific ER regimen, prescriber reluctance to switch after control is achieved, and pharmacy coverage behavior that reduces substitution friction.

2) Does Lithobid face biosimilar competition?

No. Lithium carbonate is not a biologic, so biosimilar dynamics do not apply.

3) How do formulary decisions typically change Lithobid’s net sales?

Formulary tier shifts and brand access restrictions typically reduce net price through higher patient cost-sharing and tighter rebate leverage, accelerating branded share decline.

4) What is the biggest commercial risk for a legacy branded lithium ER product?

The biggest risk is ongoing net price erosion from generics and authorized generics, which can reduce revenue even if prescription volumes remain relatively stable.

5) Are method-of-use or formulation patents likely to create a new protection window for Lithobid?

For legacy lithium salts, remaining IP often has limited practical ability to block AB-rated generic competition, so commercial protection typically depends on expiring listings that are already largely cleared.

References

- U.S. Food and Drug Administration. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations (Lithobid; lithium carbonate, extended-release). FDA.

- U.S. Food and Drug Administration. Drug Approval Reports and Regulatory Information. FDA.