LEVOCARNITINE SF Drug Patent Profile

✉ Email this page to a colleague

When do Levocarnitine Sf patents expire, and when can generic versions of Levocarnitine Sf launch?

Levocarnitine Sf is a drug marketed by Novitium Pharma and is included in one NDA.

The generic ingredient in LEVOCARNITINE SF is levocarnitine. There are four drug master file entries for this compound. Nine suppliers are listed for this compound. Additional details are available on the levocarnitine profile page.

DrugPatentWatch® Litigation and Generic Entry Outlook for Levocarnitine Sf

A generic version of LEVOCARNITINE SF was approved as levocarnitine by HIKMA on March 29th, 2001.

AI Deep Research

Questions you can ask:

- What is the 5 year forecast for LEVOCARNITINE SF?

- What are the global sales for LEVOCARNITINE SF?

- What is Average Wholesale Price for LEVOCARNITINE SF?

Summary for LEVOCARNITINE SF

| US Patents: | 0 |

| Applicants: | 1 |

| NDAs: | 1 |

| Finished Product Suppliers / Packagers: | 1 |

| Raw Ingredient (Bulk) Api Vendors: | 110 |

| Clinical Trials: | 26 |

| Patent Applications: | 4,491 |

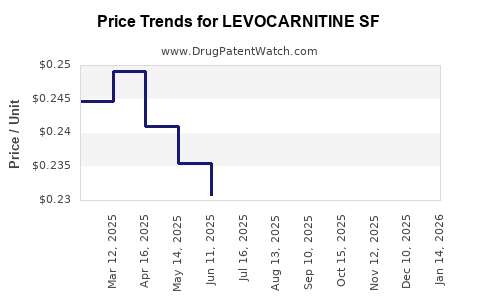

| Drug Prices: | Drug price information for LEVOCARNITINE SF |

| DailyMed Link: | LEVOCARNITINE SF at DailyMed |

Recent Clinical Trials for LEVOCARNITINE SF

Identify potential brand extensions & 505(b)(2) entrants

| Sponsor | Phase |

|---|---|

| London Health Sciences Centre Research Institute OR Lawson Research Institute of St. Joseph's | EARLY_PHASE1 |

| Shaikh Zayed Hospital, Lahore | PHASE4 |

| Children's Oncology Group | Phase 3 |

Pharmacology for LEVOCARNITINE SF

| Drug Class | Carnitine Analog |

US Patents and Regulatory Information for LEVOCARNITINE SF

| Applicant | Tradename | Generic Name | Dosage | NDA | Approval Date | TE | Type | RLD | RS | Patent No. | Patent Expiration | Product | Substance | Delist Req. | Exclusivity Expiration |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Novitium Pharma | LEVOCARNITINE SF | levocarnitine | SOLUTION;ORAL | 211676-002 | Aug 14, 2019 | AA | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| >Applicant | >Tradename | >Generic Name | >Dosage | >NDA | >Approval Date | >TE | >Type | >RLD | >RS | >Patent No. | >Patent Expiration | >Product | >Substance | >Delist Req. | >Exclusivity Expiration |