Last updated: June 24, 2026

GOLYTELY is an established, low-margin bowel-prep product in a crowded US market dominated by generic equivalents and newer branded competitors that use alternative dosing formats and marketed convenience. Financial performance is driven primarily by insured and cash-pay pharmacy channel penetration, endoscopy scheduling volumes, and payer reimbursement dynamics. Patent-driven exclusivity is no longer the primary determinant of revenue because the active ingredient complex is long off-patent, and unit economics are constrained by intense price competition and high pharmacy substitution.

What is the US market size and demand profile for GOLYTELY bowel prep products?

Featured snippet answer: Demand for PEG-electrolyte bowel preparation tracks US diagnostic and therapeutic endoscopy volumes, with seasonality tied to elective procedures and insurance enrollment patterns. Competitive substitutability keeps revenue growth modest and concentrates gains in channel share, rebates, and dosing convenience rather than pricing power.

Endoscopy volumes and procedure mix: how do they translate into prescriptions?

- Bowel prep prescribing is a derived demand from colonoscopy, sigmoidoscopy, and related GI endoscopy services.

- Revenue sensitivity is linked to:

- elective procedure volumes

- insurance authorization workflows

- prep regimen adherence, which affects rebooking and switching within classes

Payer coverage and substitution: what drives pharmacy movement?

- PEG-based bowel preps are generally interchangeable from a reimbursement perspective, which increases pharmacy substitution and limits price premiums for brands.

- Rebate structures are typically the main lever for maintaining net pricing, pushing branded products to compete on formulary placement rather than list price.

Channel dynamics: retail vs specialty vs institutional

- GOLYTELY is typically dispensed through retail pharmacies and institutional procurement channels depending on health system formularies.

- Institutional demand often shifts based on:

- procurement contracts

- nursing and pharmacy preference for lower-administration burden products

- standardized order sets in GI clinics

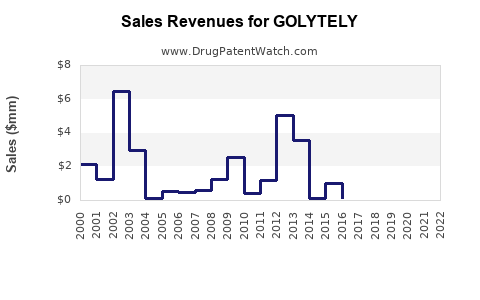

How have GOLYTELY sales and revenue trended historically in the US?

Featured snippet answer: Sales trends for GOLYTELY have generally reflected a mature branded-to-generic transition and ongoing unit-price compression as generics capture incremental pharmacy share. Growth, when it occurs, tends to come from market share resilience, not category expansion or pricing.

What financial trajectory typically looks like for mature bowel-prep brands

- Phase 1: brand launch or re-launch with formulary adoption.

- Phase 2: generic entry compresses net price; brand remains in formularies via rebates.

- Phase 3: competitor formats (reduced volume, same-day dosing, lower-sedation workflows) capture share, keeping category growth near procedure growth rate rather than brand premium.

Pricing pressure mechanics in bowel prep

- High substitution reduces willingness to pay.

- Net revenue depends on:

- payer rebate rates

- wholesaler contract pricing

- pharmacy service fees and contract mix

- pack size choices and dispensing patterns

Which companies and products compete with GOLYTELY, and how does format shape share?

Featured snippet answer: Competition comes from generic PEG-electrolyte solutions and from branded bowel preps that differentiate via volume, taste, dosing convenience, or patient instructions. Format-based switching is a major share driver.

Primary competitive set in PEG-electrolyte bowel preparation

- Generic equivalents of PEG 3350 + electrolytes solution.

- Competitors using alternative dosing formats and branded regimens, including:

- low-volume PEG-based products

- split-dose regimens branded for adherence

- non-PEG osmotic regimens that may be preferred in certain formularies or patient profiles

Why dosing convenience matters in substitution

- Patients switch prep regimens when:

- perceived tolerability is better

- instructions are simpler

- reduced volume improves completion rates

- Clinicians and GI centers shift when:

- protocol adherence improves

- fewer incomplete preps reduce repeat colonoscopy rates

Distribution and contracting: what changes net pricing?

- Institutional contracts can swing volume quickly among therapeutically equivalent preps.

- Retail net pricing is influenced by:

- PBM formulary status

- preferred product tiers

- mandatory substitution rules in state pharmacy practice

What does the Orange Book status of GOLYTELY indicate about exclusivity and generic entry risk?

Featured snippet answer: GOLYTELY’s active ingredient combination has long been off primary exclusivity, which typically leads to widespread generic availability and low barriers to formulation-by-equivalence entry.

How Orange Book mechanics affect commercial exposure

For oral solid and solution equivalents, the key commercial implications are:

- whether any listed drug substance/product patents still have enforceable life

- whether listed exclusivities block generic approval

- whether any additional exclusivity applies to specific dosage forms or manufacturing changes

Practical impact on financial trajectory

- Once generic equivalents are entrenched, branded revenue is constrained by:

- payer switching

- wholesaler stocking preferences

- rebate-driven net price convergence

What patents protect GOLYTELY, and when do they expire?

Featured snippet answer: The PEG-electrolyte combination is mature and typically has limited residual patent leverage. Financial outcomes are therefore more influenced by formulary access, contracting, and competitor differentiation than by late-stage patent cliffs.

Patent estate relevance for bowel prep

Even when individual patents remain on:

- manufacturing processes

- specific formulations

- container-closure or stability improvements

the practical market effect is often muted because clinically equivalent generics can enter when regulatory and IP barriers are weak or expired.

How to interpret patent-driven risk for mature products

For a mature bowel-prep category:

- revenue risk is more about formulary status and competitor format adoption than about a single patent expiration

- litigation-driven exclusivity holds less sway than PBM contracting cycles

What generic entry risks exist for GOLYTELY, including Paragraph IV challenges?

Featured snippet answer: The dominant risk vector is not a late Paragraph IV wave against an actively protected branded product. The recurring risk is incremental generic share capture that continues to erode net pricing.

Paragraph IV in mature bowel prep: how it impacts revenue

- Paragraph IV filings matter when:

- the branded product still has enforceable listed patents

- a settlement constrains generic approval timing

- When the category is already widely generic, revenue impact is primarily through ongoing substitution and contracting, not milestone-based entry.

What to watch commercially

- new generic entrants with different pack sizes or distribution terms

- PBM contract repricing that favors lowest net cost

How does GOLYTELY compare with branded low-volume bowel-prep competitors on marketability?

Featured snippet answer: Products with reduced volume and improved perceived tolerability tend to win share because they reduce patient burden and increase completion rates, affecting repeat procedure avoidance and provider confidence.

Differentiators that shift prescribing behavior

- total volume and perceived palatability

- dosing schedule simplicity

- split-dose compatibility with clinic workflows

- patient education materials and adherence support programs

Consequence for GOLYTELY’s financial trajectory

- If competitors expand in patient-facing marketing and formulary preference, GOLYTELY’s growth is limited to:

- patient segments where PEG-electrolyte solutions are preferred

- clinician protocol inertia

- pharmacy-channel contracts that keep it preferred on net price

What FDA regulatory status considerations affect GOLYTELY commercialization?

Featured snippet answer: GOLYTELY is an established FDA-regulated bowel-prep product; commercial performance is primarily constrained by market competitiveness and formulary access rather than by regulatory pathway uncertainty.

Labeling and patient-use instructions: financial implications

- Bowel-prep products depend on adherence to preparation steps.

- Label instructions affect:

- patient completion rates

- adverse event rates that can trigger switching

Manufacturing and supply continuity

- Bowel prep is sensitive to supply chain disruptions because demand is seasonal and procedure-driven.

- Any supply interruptions can cause temporary loss of channel share, which is hard to regain.

What litigation and settlement dynamics historically matter for GOLYTELY brands?

Featured snippet answer: In mature generics-heavy classes, litigation typically impacts timing or brand/generic exclusivity rather than sustaining long-term pricing power. The persistent driver remains market contracting.

How litigation changes commercial outcomes

- automatic stay, 180-day exclusivity, and settlement-triggered constraints can affect short-term entry timing

- over the long run, multiple generics and therapeutic equivalence dilute brand price leverage

How strong is the patent estate for GOLYTELY as a commercial moat?

Featured snippet answer: The commercial moat for GOLYTELY is weak to moderate versus category competitors because generic equivalents reduce pricing power. Where brand value persists, it usually comes from formulary position and distribution terms rather than patent protection.

Where patent value can still exist

- secondary patents can protect:

- formulation stability or specific preparation

- manufacturing methods

- pack/container improvements

But these rarely sustain premium economics once generics achieve widespread substitution.

What are the most likely future market scenarios for GOLYTELY revenue?

Featured snippet answer: Revenue is likely to track endoscopy procedure growth at a low single-digit rate with ongoing net price compression, unless GOLYTELY regains a preferred formulary tier or a competitor format loses traction through supply, labeling changes, or payer re-contracting.

Scenario A: continued generic dominance and contracting pressure

- Outcome: stable unit volumes with declining net pricing.

- Drivers: PBM preference for lowest net cost equivalents.

Scenario B: share stabilization through contracts and institutional pull-through

- Outcome: flattish revenue with reduced margin volatility.

- Drivers: long-term supply agreements, institutional standardization.

Scenario C: competitor displacement via affordability or adherence advantage reversal

- Outcome: modest brand share gains.

- Drivers: competitor supply constraints, payer shifts to PEG-electrolyte equivalents.

Key metrics to monitor for GOLYTELY financial performance

- Net selling price (after rebates and chargebacks)

- Prescription volume (TRx) in retail and institutional settings

- Formulary status changes across major PBMs

- Wholesaler contract repricing cycles

- Competitive switch rates by dosing volume category

- Supply continuity (case fill rate and backorder frequency)

Key Takeaways

- GOLYTELY operates in a mature, highly substitutable bowel-prep market where financial trajectory is dominated by formulary access, contracting, and patient adherence dynamics, not patent-driven exclusivity.

- Ongoing generic availability compresses net pricing, making revenue growth primarily dependent on share retention and procedure-driven demand.

- Competitive differentiation increasingly comes from dosing convenience and perceived tolerability, which can shift prescribing away from PEG-electrolyte solutions unless GOLYTELY maintains preferred net pricing.

FAQs

1) Does GOLYTELY have strong pricing power in the US market?

No. Pricing is constrained by widespread therapeutic equivalence and aggressive pharmacy substitution, so net pricing depends on rebate and contracting rather than premium differentiation.

2) What drives changes in GOLYTELY prescription volume month to month?

Endoscopy scheduling volumes, payer coverage dynamics, and formulary tier changes that influence substitution at the point of dispensing.

3) How do reduced-volume or alternative bowel prep products affect GOLYTELY share?

They can capture incremental share when adherence and patient completion outcomes favor simpler, lower-burden regimens, prompting payer and provider switching.

4) Are future revenue risks mainly legal or commercial?

Commercial, driven by ongoing generic substitution and PBM contract repricing. Legal impacts are secondary in a class that is already widely generic.

5) What operational factors most affect GOLYTELY sales continuity?

Supply reliability and consistent availability to channels, since missing product can cause durable switching to preferred alternatives.

References

- FDA Orange Book Database. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/

- FDA Drug Safety and Availability / Labeling resources. U.S. Food and Drug Administration. https://www.fda.gov/