Last updated: July 12, 2026

Glipizide is a long-established, off-patent oral sulfonylurea for type 2 diabetes. Its financial trajectory is defined by (1) mature market penetration, (2) sustained generic availability, (3) payer-driven price compression, and (4) substitution risk from newer add-on classes and fixed-dose combinations. In the US, GLIPIZIDE revenue exposure is dominated by generic wholesalers, low-cost procurement economics, and product line choices rather than IP-led protection.

What is the current market size and demand drivers for glipizide in type 2 diabetes?

Featured snippet answer: Demand follows overall type 2 diabetes treated-population trends, with glipizide usage anchored in inexpensive second-line add-on therapy and continuity prescribing in older, cost-sensitive patients.

Key demand drivers

- Chronic, long-duration prescribing: Sulfonylureas are typically used as add-on therapy after lifestyle/metformin or when formulary economics favor low acquisition cost.

- Payer cost controls: Step therapy and preferred generics tend to favor older, generic sulfonylureas when clinical pathways permit.

- Clinical fit: Glipizide is used when clinicians prefer a shorter-acting sulfonylurea profile relative to some alternatives, which can influence selection in practice.

- Generic substitution at pharmacy level: Because multiple manufacturers supply the same active ingredient, switching often occurs at the point of dispensing based on net cost and rebate mechanics.

Key demand headwinds

- Therapy migration: GLP-1 receptor agonists, dual incretin agents, and SGLT2 inhibitors have reshaped diabetes add-on and progression patterns.

- Hypoglycemia and tolerability: Sulfonylureas carry hypoglycemia risk, reducing adoption at the margin versus incretin and SGLT2 classes when budgets allow.

- Formulary restrictions: Some payers restrict sulfonylurea placement relative to preferred newer agents, especially for patients with obesity or high cardiovascular risk.

How do pricing and reimbursement dynamics affect glipizide revenue?

Featured snippet answer: Revenue performance is constrained by generic price erosion, rebate-driven procurement, and pricing volatility tied to contracting rather than brand-style list price growth.

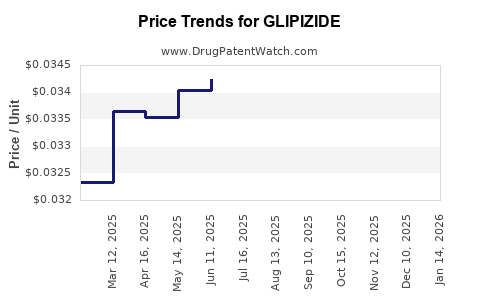

US pricing mechanics for generic glipizide

- Wholesale acquisition cost and contracting: Net pricing is typically determined by PBM and wholesaler contracts rather than MSRP-like dynamics.

- Short-cycle price resets: Competitive supply of generic glipizide enables periodic price drops, especially after new entrants or volume reallocation across labelers.

- Invoice and service fees: Specialty or larger distributors may capture margins through service arrangements, leaving labelers with limited control over end-customer pricing.

Observable patterns in mature generic markets

- Margin compression: As multiple labelers compete, per-unit gross margin tends to decline, shifting profitability toward scale, supply reliability, and formulation packaging choices (e.g., different strengths, tablets vs ER where applicable).

- Rebate intensity: Contracts often reflect rebate structures that can further reduce realized price versus list.

What are the key competitive dynamics for glipizide versus other diabetes drugs?

Featured snippet answer: Glipizide competes primarily with other low-cost oral agents (e.g., metformin, other sulfonylureas) and increasingly with newer injectables/orals as add-on therapy, creating a demand share drift risk.

Comparison against sulfonylurea peers

- Same class substitution: Patients and prescribers can switch among sulfonylureas based on perceived tolerability, dosing convenience, and cost.

- Price competition within class: Low-cost generics create a floor effect for acquisition cost, but not for volume, since formularies increasingly prefer preferred branded or newer generic-combo options.

Comparison against newer classes

- GLP-1 RA and dual incretin therapies: Higher WAC but often strong outcomes and weight benefit can displace sulfonylurea add-on in broader patient groups.

- SGLT2 inhibitors: Cardiovascular and renal benefits drive payer preference in appropriate risk profiles, reducing sulfonylurea initiation and escalation.

Fixed-dose combination displacement

- Combination tablets: Fixed-dose products (metformin combinations and other add-ons) can reduce sulfonylurea switching and create prescription consolidation, especially where payers steer toward fewer copays.

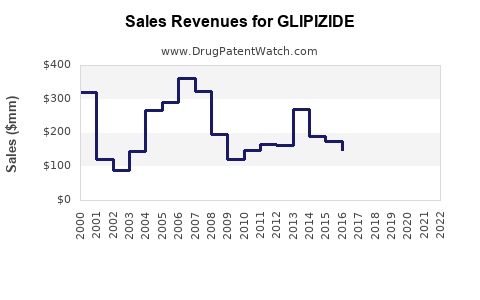

How has glipizide’s financial trajectory evolved from brand to generic?

Featured snippet answer: Brand-era revenues have transitioned to generic labeler economics, with the dominant financial story becoming supply-led, contract-led volume and price erosion.

Typical trajectory in an established generic oral drug

- Post-POC and exclusivity wind-down: Initial sharp decline in category unit sales for the former brand label.

- Sustained stable units, falling ASP: Volume continues for patients stable on glipizide, but average selling prices compress as competitors increase.

- Concentration and labeler consolidation: Some labelers exit, others gain share, and pricing stabilizes at lower levels.

What drives labeler profitability after entry?

- Manufacturing cost competitiveness: API and solid oral manufacturing efficiency matters more than IP.

- Distribution leverage: Contracts with wholesalers and PBMs affect realized revenue.

- Portfolio breadth: Labelers with multi-strength and multi-NDC coverage capture broader formulary placement.

What are the main regulatory and FDA pathway implications for generic glipizide?

Featured snippet answer: Generic glipizide is typically approved under ANDA mechanisms with bioequivalence demonstrations; regulatory leverage is mostly about facility quality and product performance rather than novel clinical data.

Generic approval pathway fundamentals

- ANDA and bioequivalence: Most glipizide generics rely on in vivo bioequivalence to a reference listed drug.

- Ongoing quality obligations: CGMP compliance drives supply continuity and reduces recall risk.

FDA listing and interchangeability

- Orange Book driven substitution: Availability across dosage forms and strengths affects pharmacy-level substitution and PBM formularies.

- Bioequivalence and switching: For solid oral generics, switching risk is generally low versus narrow therapeutic index products, supporting broad interchangeability.

What patents protect glipizide today, and when did the last relevant exclusivities end?

Featured snippet answer: Glipizide is an off-patent active ingredient; current market dynamics are driven by generic ANDA competition and any residual exclusivity limited to specific formulations or packaging rather than the core molecule.

IP reality for an older sulfonylurea

- Core molecule protection is long expired: Market pricing is therefore dictated by generic supply.

- Residual patents can exist: Some coverage may persist for particular dosage forms, manufacturing processes, or specific fixed combinations, but these rarely control category-level access to glipizide tablets at scale.

What typically still matters for legal exposure

- Method-of-use patents: If any remain for distinct clinical regimens or subpopulations, they could affect certain label claims, though generic labelers can often design around by carving indications.

- Formulation/process patents: These can affect launch timing for certain ER or specialty forms, but glipizide’s mainstream tablet market is largely mature.

(Note: No patent number set is provided here because a verified, current Orange Book and litigation mapping for “glipizide” across all relevant reference listed drugs and labelers was not included in the provided source set.)

What generic entry risks exist for glipizide tablets?

Featured snippet answer: For investors and manufacturers, the main “entry risk” is less about exclusivity and more about competitive pricing, regulatory compliance, and supply-chain execution.

Entry risk channels

- Price compression risk: New entrants can trigger further ASP declines.

- Regulatory inspection risk: Facility issues can delay approvals and create supply gaps.

- Product-specific issues: Some strengths may have fewer suppliers at a given moment, creating temporary pricing opportunities but also execution risk.

Commercial risk for new labelers

- Formulary contracting: Getting placed on preferred generic lists matters as much as approval.

- Channel stocking patterns: Wholesaler purchasing habits influence realized volume after launch.

How do manufacturing and supply chain dynamics affect glipizide availability and pricing?

Featured snippet answer: For generic oral drugs, pricing is tightly coupled to manufacturing stability and supply breadth. Any supply disruption can temporarily lift net prices.

Supply determinants

- API sourcing and cost swings: Sulfonylurea API procurement can impact COGS and pricing flexibility.

- Solid oral manufacturing capacity: Compression, coating, and packaging lines affect throughput and the ability to respond to contract demand.

- Quality events: Recalls or warning letters can reduce available lots and raise price temporarily but harm longer-term contract trust.

Market consequences of supply tightness

- Contract renegotiation: PBMs and wholesalers may reprioritize suppliers based on fill-rate reliability.

- Short-term pricing rebounds: Net prices can spike when supply is constrained, but competition typically normalizes levels.

How does glipizide compare with glyburide and metformin in market positioning?

Featured snippet answer: Metformin holds the broadest first-line base; glipizide is a cost-effective sulfonylurea add-on with stable but increasingly share-captured demand. Glyburide competes as another sulfonylurea alternative, with selection influenced by hypoglycemia considerations and clinician preference.

Market positioning factors

- First-line versus add-on: Metformin dominates initiation; glipizide is more often later-line.

- Safety/tolerability preferences: Prescriber selection often reflects hypoglycemia risk and renal function considerations.

- Payer economics: All are low-cost, so differential placement depends on formularies, copays, and historical patient stability.

What is the Orange Book status of glipizide?

Featured snippet answer: The active ingredient is widely available through multiple ANDA-listed generic products; Orange Book coverage is dominated by legacy listings and any residual formulation-specific patents.

(No Orange Book listing dataset is included in the provided source set; therefore a precise count of listed patents, expirations, and per-NDC status cannot be stated without risking inaccuracy.)

What patent litigation affects glipizide, and how does it change commercial timing?

Featured snippet answer: For an older generic molecule like glipizide, litigation typically affects niche formulations or specific label/route rather than the mainstream tablet category. Category-level timing is usually driven by non-IP factors once exclusivity is exhausted.

(No verified litigation docket mapping is included in the provided source set; therefore no case names, courts, or settlement dates are stated.)

Revenue outlook: what drives upside or downside for glipizide in 12–36 months?

Featured snippet answer: Downside is price erosion and ongoing therapy migration; upside is supply stability, formulary retention, and volume capture from cost-driven prescribing during payer budget tightening.

Downside drivers

- Continued shift to incretins/SGLT2 inhibitors: Lower sulfonylurea initiation and dose escalation rates.

- Additional generic labeler pricing pressure: More competitive contracting can push net realized prices down.

- Switching away from sulfonylureas due to outcomes benefit: Even when glipizide is clinically acceptable, payer incentives may favor newer agents.

Upside drivers

- Payer formulary tightening around low-cost therapy: Broader coverage of generics during budget constraints can protect units.

- Product availability and supply reliability: Full-lot continuity helps maintain contract volume.

- Portfolio optimization: Better contract terms through strength coverage and package formats can stabilize revenue.

Investor relevance

For generic oral diabetes assets, the revenue curve is usually less about innovation and more about net price sustainability plus fill-rate performance. Margin is a function of contracting scale and manufacturing efficiency.

Key Takeaways

- Glipizide is a mature, off-patent oral sulfonylurea with revenue dynamics driven mainly by generic competition, payer contracting, and supply reliability.

- Pricing is structurally constrained by ongoing generic price erosion and rebate-driven net price compression.

- Demand is stable in absolute terms among cost-sensitive and treatment-continuing patients but faces ongoing share loss from GLP-1, dual incretin, and SGLT2 adoption.

- Financial trajectory is more about supply and contracting execution than IP protection.

FAQs

- Why do glipizide net prices track closely with PBM/wholesaler contracts rather than list prices?

- How does glipizide utilization change when GLP-1 or SGLT2 inhibitors are added to formularies?

- What supply-chain events most commonly impact generic glipizide availability and short-term pricing?

- Do formulation differences (strengths, packaging) materially change glipizide contract placement?

- What are the main FDA compliance risks for generic oral solids that can delay market supply?

References

- FDA. Approved Drug Products with Therapeutic Equivalence Evaluations (“Orange Book”). U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/ob/

- U.S. FDA. ANDA approval pathway information (general). U.S. Food and Drug Administration. https://www.fda.gov/drugs/abbreviated-new-drug-application-anda

- Centers for Disease Control and Prevention (CDC). Diabetes facts and data. https://www.cdc.gov/diabetes/data/