Last updated: April 25, 2026

What is gentamicin’s current market position by product type and use case?

Gentamicin is an aminoglycoside antibiotic used primarily for serious Gram-negative infections and as a topical ophthalmic or surgical adjunct in specific care settings. The market dynamics are structurally shaped by (1) the mature, off-patent status in most geographies, (2) low to moderate willingness-to-pay relative to newer anti-infectives, (3) recurring hospital demand driven by infection-control protocols, and (4) margin compression from generic competition.

Demand drivers

- Hospital and acute-care utilization: Gentamicin is used in inpatient regimens for severe infections where Gram-negative coverage is needed.

- Combination therapy: In practice, gentamicin is often paired with other antibiotics depending on indication and local resistance patterns, supporting steady demand even as monotherapy use may fluctuate by stewardship policies.

- Topical/ophthalmic niches: Eye preparations and local use cases sustain incremental demand even when systemic use softens.

Key market constraint

- Generic saturation: In most major markets, gentamicin formulations (injection and many topical forms) trade as generics, limiting pricing power and compressing returns.

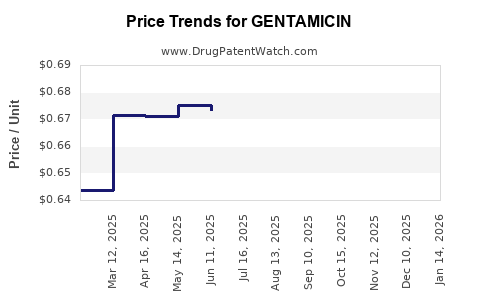

How do supply and pricing dynamics typically play out for gentamicin?

Gentamicin’s commercial profile is dominated by generic supply chains and tender-driven hospital procurement.

Pricing mechanics

- Tender-based contracting: Hospital purchasing often uses tenders and pharmacy group agreements; pricing tracks low-cost generic availability rather than clinical brand premium.

- Portfolio substitution: If comparable aminoglycosides or alternative Gram-negative agents are clinically acceptable in a given protocol, switching can occur at the procurement level, tightening pricing pressure.

- Production scale effects: Supplier consolidation and fermentation/chemical input costs can create short-term price swings, but equilibrium pricing tends to revert due to market openness to multiple manufacturers.

Supply stability

- Off-patent multi-source: Broad manufacturing base reduces risk of sustained shortages compared with single-manufacturer, single-molecule branded therapies, though periodic supply disruptions can still occur.

What market forces affect gentamicin demand over time?

Gentamicin demand is most sensitive to healthcare policy, resistance patterns, and stewardship and safety constraints.

Healthcare policy and stewardship

- Appropriate use: Aminoglycosides carry known nephrotoxicity and ototoxicity risks; stewardship programs can tighten or widen usage depending on local patient mix and monitoring capacity.

- Protocol evolution: Guidelines for empiric sepsis and hospital-acquired infection management shift between antibiotic classes based on resistance and safety data, which impacts relative use of gentamicin-containing regimens.

Resistance and clinical practice

- Gram-negative resistance: When resistance patterns degrade aminoglycoside effectiveness, clinicians may reduce gentamicin exposure, lowering unit demand even if stewardship keeps it available for targeted use.

- De-escalation: If cultures support aminoglycoside sensitivity, gentamicin can retain relevance as a de-escalation option, offsetting some demand erosion.

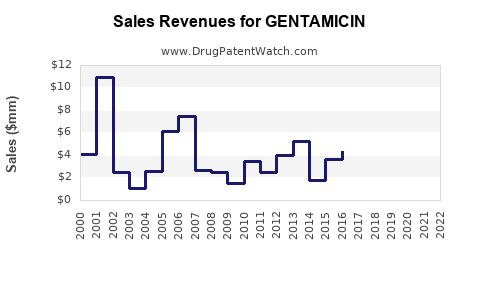

What does the financial trajectory look like for a mature, off-patent antibiotic like gentamicin?

For mature antibiotics, the financial trajectory typically follows a pattern:

- Late-brand peak or decline (historical branded dominance).

- Rapid erosion of price after generic entry.

- Volume stabilization with margin compression via multi-source procurement.

- Periodic value bumps from new formulation launches, tender cycles, or geographic re-contracting.

- Long-run flat-to-slow decline in net revenue unless a product regains preferential positioning (rare for established antibiotics).

Commercial outcome

- Net sales usually scale with inpatient volume and contract pricing, not with innovation-driven premiumization.

- Profitability is primarily determined by manufacturing efficiency, inventory management, and tender win rates, not marketing or clinical breakthrough differentiation.

How does patent and exclusivity structure drive revenue visibility?

Gentamicin itself is an old, off-patent molecule in most markets. The revenue visibility is therefore shaped less by molecule patent life and more by:

- Formulation-specific protections where they exist in certain markets.

- Regulatory exclusivity windows (rare for established simple injectables).

- Branding and distribution arrangements by generic holders, which can shift with competitive tender cycles.

Bottom line for the financial view

- High likelihood of generic price compression in any market once multiple suppliers qualify.

- Predictability of demand is usually higher than predictability of margins because prescribing volume tends to be steadier than unit prices.

How do regulatory and safety factors influence market outcomes?

Aminoglycoside safety requirements (notably renal and auditory toxicity monitoring) influence clinician behavior and hospital protocol design.

Practical impacts

- Monitoring costs and required protocols can reduce convenience for some hospitals, but the drug’s cost effectiveness can still support use.

- Label language and local pharmacovigilance can modify utilization patterns, particularly if new warnings emerge or if guidance strengthens monitoring thresholds.

Where does value concentrate: systemic injection vs. topical ophthalmic?

Gentamicin’s market value tends to concentrate in segments that reliably generate demand and are less substitution-prone.

Systemic injection

- Tied to inpatient infection burden and empiric regimen selection.

- Highly exposed to generic tender economics.

Topical ophthalmic/surgical use

- Can be less sensitive to systemic stewardship shifts if protocols keep local preparations in place.

- Still subject to generic competition but may show smoother quarter-to-quarter stability.

What are the main competitive dynamics among aminoglycosides and alternatives?

Competition does not only come from gentamicin generics; it also comes from other Gram-negative options.

Competitive set

- Other aminoglycosides and alternative antibiotic classes used in the same clinical workflows.

- Agents with improved dosing convenience or safety profiles can displace gentamicin if clinically permissible.

Competitive consequences

- Gentamicin’s market share can persist for stewardship-aligned indications but pricing tends to remain constrained due to interchangeable usage in many settings.

How do hospital tender cycles translate to financial performance?

For off-patent injectables, the financial P&L is often driven by procurement patterns:

- Tender timing can cause revenue step-changes when supply contracts are renewed.

- Winning share depends on lead time reliability, batch release performance, and compliance record.

- Price erosion is typical after new entrants qualify or when incumbent suppliers lose a tender.

This creates a financial trajectory characterized by volatile gross-to-net pricing with comparatively stable underlying demand.

What does the expected long-run trend mean for investment or R&D strategy?

For an established, off-patent antibiotic, investment outcomes typically hinge on market execution rather than molecule novelty.

Where value creation can still occur

- Differentiated manufacturing quality that wins tenders.

- Portfolio bundling across strengths, pack sizes, and formats.

- Expansion into markets with less generic saturation or where hospital contracting favors reliable suppliers.

Where financial upside is limited

- New sales growth from clinical breakthrough is generally constrained because the molecule is mature and standard-of-care positioning is already well established.

Key Takeaways

- Gentamicin’s market is defined by mature, off-patent economics: tender-driven pricing and generic multi-source competition.

- Demand is hospital/acute-care anchored, with additional stability from topical/ophthalmic niches.

- Financial trajectory is typically stable volume with margin compression, with revenue variability driven by tender cycles more than by innovation.

- Long-run profitability is primarily determined by manufacturing efficiency, regulatory compliance, and contract execution, not pricing power.

FAQs

1) Is gentamicin’s growth driven by new clinical adoption or by procurement economics?

Procurement economics dominate. In mature antibiotics, utilization is protocol- and resistance-driven, while revenue is shaped by contracting and generic pricing.

2) What factors most directly pressure gentamicin margins?

Generic competition and tender-based pricing pressure. When multiple suppliers qualify, pricing tends to converge toward low-cost equivalents.

3) Does gentamicin benefit from combination therapy patterns?

Yes. Use in multi-drug regimens can support consistent inpatient demand even when monotherapy preference shifts by guideline or resistance data.

4) Which segment is usually more stable: systemic injection or topical use?

Topical and niche local uses often show smoother demand than systemic use, though both face generic tender pressure in many markets.

5) What is the most reliable indicator for near-term financial outcomes?

Contracting and purchasing cycle data, including tender wins, pricing resets, and supplier qualification status.

References

[1] DailyMed. “GENTAMICIN (gentamicin sulfate) injection.” U.S. National Library of Medicine.

[2] DailyMed. “GENTAMICIN (gentamicin sulfate) ophthalmic solution/ointment.” U.S. National Library of Medicine.

[3] World Health Organization (WHO). Model List of Essential Medicines: antibiotics including aminoglycosides. WHO.

[4] U.S. Food and Drug Administration (FDA). Drug Safety-related information and labeling standards for aminoglycosides (class safety considerations). FDA.

[5] IQVIA Institute / industry reporting on hospital anti-infective procurement dynamics (tender and generic pricing effects). IQVIA.