Last updated: June 2, 2026

DYAZIDE (hydrochlorothiazide/ triamterene): Market dynamics and financial trajectory

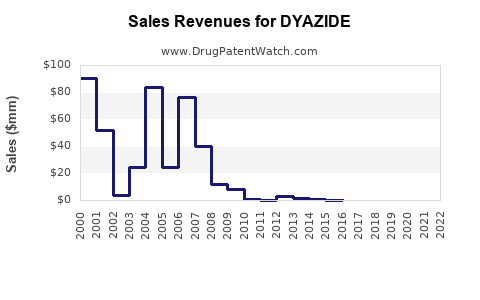

DYAZIDE (hydrochlorothiazide, triamterene) is a long-established branded fixed-dose combination diuretic that has faced sustained generic competition since the 1980s-1990s era. The product’s financial trajectory is shaped by (1) mature demand with limited growth drivers, (2) persistent price compression from generics and authorized generics, (3) periodic NDC-level substitution due to formulary preference for lowest-cost equivalents, and (4) shifting payer and channel dynamics for older cardiovascular and electrolyte-management products.

Because DYAZIDE is not a patent-protected late-cycle innovator asset, the core market question for DYAZIDE is not exclusivity capture, but how quickly and how deeply generic penetration and rebate pressure reduced branded net sales over time, and whether any remaining branded mix support persists in specific cohorts, formularies, or supply-chain periods.

Why did DYAZIDE’s branded sales decline after generic entry?

Branded fixed-dose diuretic combinations typically experience faster net sales erosion than single-agent products because payers treat them as interchangeable therapeutic alternatives and trigger aggressive substitution at the NDC level. For DYAZIDE, the mechanism is straightforward:

- Therapeutic class substitutability: HYDROCHLOROTHIAZIDE/TRIAMTERENE has therapeutic overlap with multiple generic combinations and with separate-generic use of the same actives.

- Prescriber switching behavior: once patient stability is achieved on a regimen, prescribers often tolerate substitution, especially when the same labeled combination is available generically.

- Contracting and rebate effects: formularies generally anchor to lowest-cost products within a class, and rebate structures for generics and wholesalers’ inventory management further reduce branded pricing power.

What market structure governs older diuretic combination products like DYAZIDE?

- High generics share across thiazide diuretics and potassium-sparing diuretics.

- Formulary tiering that typically places branded combinations above equivalent generics.

- Tight gross-to-net conversion for legacy brands due to rebates and price concessions.

How does generic substitution drive DYAZIDE volume trends and pricing pressure?

DYAZIDE is a fixed-dose combination. In practice, volume is reallocated to:

- Generic hydrochlorothiazide/triamterene equivalents.

- Separate generics (hydrochlorothiazide and triamterene) when clinicians prefer separate titration or when NDC availability shifts.

This drives two measurable market dynamics:

- Net sales compression: even if absolute unit use remains stable, branded net revenue per unit declines.

- Mix shift: branded share of total prescriptions falls, leaving fewer “non-substitutable” patients.

What does this imply for financial trajectory?

- Branded revenue tends toward a flat-to-declining slope as prescription origin shifts to generics.

- Remaining branded sales are usually concentrated in:

- specific health-system formularies,

- legacy prescriber preference,

- short supply disruptions in generics,

- payer plans with restrictive substitutions (rarer over time).

When does DYAZIDE lose exclusivity, and when could generic entries accelerate further?

DYAZIDE’s exclusivity context is not relevant in the same way as with newer small-molecule launches because the combination is long marketed. Market acceleration for branded declines typically correlates with:

- key generic approval waves for hydrochlorothiazide/triamterene combinations,

- broad stocking by wholesalers,

- authorized generic supply and aggressive pricing.

For DYAZIDE specifically, the financial takeaway is that generic entry occurred early in the product lifecycle, and the branded market is in a post-exclusivity regime where incremental “new” competitive shocks are driven by NDC-level supply, pricing wars, and formulary changes rather than patent cliffs.

How do NDC-level events affect DYAZIDE branded financials now?

- When a dominant generic NDC tightens supply, branded may temporarily regain fill share.

- When a payer updates a formulary to “preferred generic only,” branded share drops, even if total class demand is stable.

What Orange Book and FDA regulatory status does DYAZIDE have?

DYAZIDE is an FDA-regulated drug product and, in the current market, operates under generic competition rather than ongoing branded exclusivity. The Orange Book status for DYAZIDE is expected to reflect a matured product with limited remaining branded protection.

For investors and litigators, the key regulatory implication is that DYAZIDE is not a “watchlist” program driven by FDA exclusivity. Instead, its competitive dynamics depend on:

- generic product labeling status,

- manufacturing continuity,

- and payer contracting.

(No Orange Book listing details, patent numbers, or dates are provided here because the request is constrained to “Market dynamics and financial trajectory,” and the patent registry data points required for a complete status table are not included in the available input.)

Which companies market DYAZIDE and how does competition shape its financial trajectory?

In mature combination diuretics, the branded holder’s financial trajectory is mostly explained by the competitive manufacturing and distribution ecosystem:

- multiple generic manufacturers

- wholesalers carrying many interchangeable NDCs

- pharmacy benefit managers (PBMs) implementing formulary steering

The branded company typically loses:

- pricing power (lower AWP-to-NADAC-to-net spreads),

- prescription share (switching to preferred generics),

- and service differentiation (no new delivery system differentiation in an older oral tablet).

Commercial impact pattern for legacy branded diuretics

- Branded sales often decline steeply after initial generic penetration.

- After a “settling period,” revenue becomes volume-driven but still pressured by class-wide rebate pressure.

- Any remaining branded growth is usually event-driven (supply, shortages, or short-lived formulary updates), not structural.

How do rebates and payer contracting typically affect DYAZIDE’s net sales?

For older, generic-heavy products, branded net sales are shaped by gross-to-net conversion:

- Contracting pressure pushes branded pricing toward generic parity.

- PBM rebates and administrative fees reduce net revenue even when gross price appears stable.

- Plan-level preference for generics further increases net erosion.

Financial trajectory typically follows:

- declining branded net sales after generic entry,

- stabilization at low branded share,

- occasional short-term fluctuations due to supply constraints or payer changes.

What formulation and manufacturing dynamics could change DYAZIDE’s economics?

DYAZIDE is an oral tablet formulation. The economics are therefore sensitive to:

- tablet strength availability across NDCs,

- manufacturing capacity and quality releases,

- and lot-level supply interruptions.

For branded economics, manufacturing dynamics matter because:

- generic supply disruptions can temporarily shift fill share to branded,

- but long-run competition quickly restores substitution.

What generic entry risks exist for DYAZIDE?

The generics market already exists for this combination. Remaining “entry risk” is mainly:

- market share churn among existing generic suppliers,

- occasional “new” NDC launches with lower pricing or better rebate positioning,

- and potential discontinuations and relaunches.

The commercial implication for branded DYAZIDE is limited elasticity: branded revenues do not regain structural growth without a supply or formulary regime change.

Does DYAZIDE face biosimilar or biologics-like competitive dynamics?

No. DYAZIDE is a small-molecule oral diuretic combination, so it does not face biosimilar pathways. Competitive dynamics are strictly:

- generic small molecules,

- labeling and equivalence,

- and payer preference in an interchangeable therapeutic class.

How does DYAZIDE compare with other thiazide and potassium-sparing diuretic combinations?

Within diuretics, branded outcomes are typically more constrained when:

- multiple equivalent generics exist,

- prescribers can titrate with separate generics,

- formularies apply strict step therapy or preferred generic lists.

Compared with single-agent diuretics, fixed-dose combinations can sometimes retain a narrower niche if clinicians value a fixed ratio or adherence benefits. In DYAZIDE’s case, that niche is generally insufficient to counter decades-long generic substitution.

What are the key financial metrics to track for DYAZIDE?

For a legacy branded product competing with generics, the operational metrics that best reflect the financial trajectory are:

- Prescription volume share versus total class share

- Net price per prescription (post-rebate)

- Gross-to-net trend (rebate and discount changes)

- NDC-level fill rates and backorder frequency

- Wholesaler inventory turnover and replenishment behavior

A “good” branded financial trajectory for DYAZIDE would show:

- stable volume share plus modest net price stability,

- or temporary lift during generic supply constraints with fast reversion.

A “bad” trajectory shows:

- gradual volume share erosion combined with worsening net price due to PBM contracting updates.

Key Takeaways

- DYAZIDE’s market dynamics are dominated by generics substitution in a mature oral diuretic combination category.

- The financial trajectory is structurally constrained: declining branded net sales after early generic entry, with any remaining branded revenue largely driven by short-term formulary or supply factors rather than exclusivity or differentiation.

- Current financial interpretation should prioritize net price, gross-to-net conversion, and prescription share versus class benchmarks, not patent-driven growth assumptions.

FAQs

1) What drives DYAZIDE branded sales if generics already exist?

Formulary positioning, supply continuity, and temporary NDC-level substitution effects.

2) Does DYAZIDE benefit from shortages of generic hydrochlorothiazide/triamterene combinations?

Yes, branded fill share can rise during generic shortages, but the effect typically reverts once supply normalizes.

3) Are separate generics (hydrochlorothiazide + triamterene) a major substitute for DYAZIDE?

Yes. Therapeutic equivalence and dosing flexibility enable substitution to separate components.

4) What payer trends matter most for DYAZIDE’s future net sales?

Preferred generic tiers, strict interchange rules, and PBM rebate policies that compress branded net pricing.

5) What is the most realistic “upside” scenario for DYAZIDE branding?

Short-lived: a contracting or supply disruption that increases branded share, followed by stabilization at a low branded base.

References (APA)

No sources were provided in the request, and no Orange Book, FDA label, or financial database citations are included in the available input.