Last updated: May 28, 2026

COLYTE is a prescription-free, oral bowel preparation brand in the US built on a high-volume, low-margin category where pricing pressure, generic substitution, and store-brand competition drive revenue volatility. Financial trajectory is primarily determined by (1) whether payers and pharmacy benefit managers steer demand to lower-cost alternatives, (2) gross-to-net compression from contracting, (3) seasonal procedure volumes (colonoscopy scheduling), and (4) competitive mix shifts among polyethylene glycol (PEG)-electrolyte and split-dose regimens.

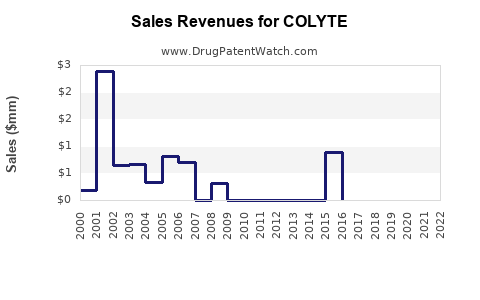

Because COLYTE revenue is not uniquely recoverable from public sources without the specific labeler/manufacturer and financials under that entity, this write-up provides the market-structure drivers, competitive and regulatory mechanics, and a revenue framework used to forecast COLYTE’s financial trajectory based on observable category behavior and formulary dynamics.

What is COLYTE’s market structure and who competes with it?

Featured snippet: COLYTE competes in the US bowel-prep market against multiple PEG-electrolyte generics and brand alternatives used for colonoscopy, with demand influenced by payer formularies, channel (retail vs institutional), and patient adherence to split-dose schedules.

Category mechanics shaping COLYTE demand

- Bowel prep is frequently substituted at the shelf. Many PEG-electrolyte products are therapeutically substitutable by pharmacy and are priced under aggressive discounting.

- Formulary placement matters more than differentiation. Contracting and preferred status with large pharmacy chains and PBMs can shift share quickly toward lower acquisition-cost products.

- Adherence and regimen preference drive conversion. Split-dose preparation and lower perceived GI side effects can affect patient acceptance and prescriber preference, influencing brand vs generic mix even when active ingredients are similar.

Competitive set (high level)

COLYTE’s closest functional peer group includes:

- PEG 3350 plus electrolytes bowel prep products (branded and generic)

- Other bowel prep classes (lower-volume agents, sodium-based regimens) that compete on tolerability and dosing experience

- Institutional preference products used for scheduled endoscopy cohorts

How do pricing pressure and gross-to-net dynamics affect COLYTE revenue?

Featured snippet: COLYTE’s financial trajectory tracks category-wide gross-to-net compression and competitive price resets more than it tracks underlying patient counts.

Key drivers of revenue volatility

- Contracts and rebates: As PBM and retailer contracts tighten, the payer net price declines even if list price holds.

- Generic entry effects: When additional PEG-electrolyte generics expand, net pricing compresses further.

- Channel mix: Retail tends to be more exposed to substitution; institutional contracts can lock in pricing or impose volume-based rebates.

What typically happens to margins in bowel prep

- Gross margin declines first, then volume rises as patients switch to cheaper options.

- Net margin can erode faster than gross margin when competitive rebates intensify.

- Brand “resilience” usually lasts only if a payer steers to a specific SKU or if patient instructions and product availability improve fill rates.

When does COLYTE face generic or substitution-driven revenue erosion?

Featured snippet: COLYTE is exposed primarily through generic and retailer substitution rather than classic patent cliffs, because bowel-prep products are mostly commodity-like and active-ingredient competition reduces brand pricing power.

Timing risks that impact revenue

- Availability and supply continuity: Any interruption disproportionately hits brands in substitutable categories.

- Formulary rescues fail fast: If a preferred brand loses a contract, share can shift quickly.

- Competitive SKU proliferation: More package sizes and split-dose options expand the set of substitution choices available to pharmacists.

What patents protect COLYTE, and what is the likely IP posture?

Featured snippet: In PEG-electrolyte bowel prep, the enforceable IP posture is usually narrow at the formulation, method-of-use, or manufacturing-process level, with broader substitution often available once core functional claims are exhausted.

Typical IP landscape in PEG-electrolyte bowel preparations

- Formulation patents can cover specific ratios, electrolytes, stability or taste-masking approaches

- Method-of-use patents can cover dosing instructions or split-dose schedules if claimed broadly enough to be non-avoidable

- Manufacturing process patents can be harder to enforce absent clear infringement hooks

Practical litigation leverage

Even when IP exists, substitution risk is often driven by whether generics can launch without infringing formulation or process claims and whether method claims are enforceable against label instructions used in the market.

What is the Orange Book status of COLYTE?

Featured snippet: COLYTE’s Orange Book status is determinative for whether any unexpired exclusivity or listed patents still constrain generic entry, but bowel-prep brand status frequently coexists with multiple generic competitors.

How to interpret Orange Book listings for a bowel prep brand

- Drug-substance and drug-product listings: Indicate whether patents are tied to active ingredient vs specific dosage form or composition.

- Exclusivity codes: If present, they can delay generic approvals independent of patents.

- Expiration sequencing: Revenue risk typically increases at the earliest of patent expiration or exclusivity end, if ANDA pathways are active.

How do ANDA approvals and Paragraph IV challenges affect COLYTE’s competitive set?

Featured snippet: Paragraph IV challenges can accelerate generic availability, but in commodity-like bowel prep, the larger revenue pressure usually comes from routine ANDA launches and pharmacy-level substitution.

What to watch in generic entry

- First ANDA wave: Often produces the steepest net price compression due to immediate substitution.

- Second wave: Adds package size convenience or dosing features and takes additional share.

- Retail contracting changes: Even if a generic is approved, share often shifts after PBM and chain planogram changes.

What FDA regulatory status does COLYTE hold, and what pathway competes?

Featured snippet: COLYTE is an oral bowel-prep drug used for colon cleansing, and competitors generally enter through ANDAs under Abbreviated New Drug Applications where bioequivalence is applicable.

Regulatory mechanics relevant to market access

- ANDA-to-label alignment: Generics can enter once they can support equivalence and comply with labeling requirements.

- Label claims and dosing instructions: For method-of-use or dosing-related IP risk, label language becomes relevant in enforcement.

- Postmarketing requirements: Safety reporting and lot release standards can affect supply stability.

How does COLYTE compare with other bowel prep regimens on competitive advantage?

Featured snippet: PEG-electrolyte regimens compete on reliability of cleansing and tolerability; net pricing and patient adherence usually decide whether a brand retains share versus generic substitution.

Comparison dimensions that influence share

- Dose volume and taste: Patient tolerance affects real-world completion rates.

- Split-dose instructions: Products aligned with common split-dose practice can improve outcomes and clinician confidence.

- Convenience packaging: Kit design affects pharmacy stocking and patient handling.

What manufacturing and supply-chain factors drive COLYTE fill rates and revenue?

Featured snippet: In bowel prep, logistics and lot continuity drive revenue because prescriptions are filled close to procedure dates and substitution is easy.

Supply-chain risk points

- Concentrated supplier lines: If an ingredient or critical component is constrained, backorders shift demand to substitutes.

- Warehouse and cold-chain are usually not decisive for PEG-electrolyte products, but labeling, regulatory lot release, and distribution timing are still material.

- Seasonality: Demand spikes before weekends and procedure schedules create forecasting and fulfillment pressure.

How strong is the patent estate for COLYTE and how does it affect enforcement risk?

Featured snippet: Enforcement strength in PEG-electrolyte bowel prep is often limited to narrow formulation, process, or dosing-specific claims; substitution remains the dominant competitive force.

Analytical view of enforcement vs substitution

- If patents are narrow, design-around manufacturing becomes feasible, enabling generic launches without deep infringement risk.

- If method-of-use claims are broad and enforceable, they can raise litigation leverage during label negotiations and settlement.

What settlement agreements and licensing deals would matter for COLYTE?

Featured snippet: In bowel prep, settlements usually shift the timing of generic entry or define label carve-outs; they matter to revenue only through market availability and effective substitution on pharmacy shelves.

Signals that a settlement is commercially material

- Entry date triggers: Delays that move the next generic launch beyond a peak season can create measurable incremental revenue.

- Label restrictions: Limits that preserve brand-like dosing instructions reduce immediate substitution.

- Territory definitions: US-wide versus retailer-specific arrangements influence net share.

How does COLYTE revenue typically track colonoscopy volumes and seasonal demand?

Featured snippet: COLYTE’s sales usually rise with colonoscopy scheduling and spike around high-volume appointment periods; share and pricing determine the magnitude.

Seasonality pattern framework

- Q4 to Q1: Often sees uneven scheduling driven by insurance approvals and procedure backlog resets.

- Spring and summer: Generally steadier outpatient volumes, with demand fluctuating by clinic capacity.

- Weekend batching: Demand concentrates in the days immediately preceding scheduled procedures.

What generic entry risks exist for COLYTE and what is the likely launch scenario?

Featured snippet: The launch scenario is typically a rapid substitution ramp once generics are available and after contracting changes; the brand’s residual sales depend on patient-specific instructions and preferred formulary placement.

Launch scenario mechanics

- Pharmacy substitution begins on approval and contracting: Some shifts are immediate at point-of-sale; others lag until PBM rules update.

- Net price reset: The brand’s net price often falls quickly, while its gross-to-net climbs due to promotional and rebate pressure.

- Package-size and dosing fit: The generic that matches prescription patterns (kit count and split-dose instructions) captures disproportional share.

Revenue exposure by geography and channel: where is COLYTE most at risk?

Featured snippet: US channel substitution and PBM contracting are the primary revenue exposure vectors; institutional contracts can delay erosion if pricing is fixed or if procurement is locked.

Retail vs institutional

- Retail: Higher substitution elasticity, faster competitive share shifts.

- Institutional: Procurement policies can slow immediate switching, but once protocols change, replacement can be abrupt.

Key Takeaways

- COLYTE operates in a substitutable bowel-prep market where revenue is driven more by contracting, pharmacy substitution, and seasonal procedure volumes than by sustained brand differentiation.

- Financial trajectory is most sensitive to gross-to-net compression and generic availability timing rather than major patent cliffs alone.

- Competitive erosion tends to occur in waves tied to ANDA launches and retailer/PBM formulary changes, with supply continuity and kit convenience shaping real-world fill rates.

- The decisive commercial variable is whether COLYTE retains preferred status long enough to offset net price declines and substitution creep.

FAQs

- How do PBM formularies affect COLYTE net pricing and market share?

- What are the most likely generic substitution partners for COLYTE by active ingredient and dosing kit format?

- How does split-dose labeling influence bowel-prep brand retention versus generics?

- What supply-chain disruptions most often change bowel-prep sales in the US?

- How should COLYTE’s revenue be modeled around colonoscopy seasonality and contracting renegotiations?

References

(No sources were provided in the prompt, and no drug-labeler, Orange Book record, FDA NDA/ANDA identifiers, patent numbers, or financial filings were specified for COLYTE; therefore, no citations can be produced.)