Last updated: February 19, 2026

This report analyzes the market dynamics and financial trajectory of CELEXA (citalopram hydrobromide), focusing on its patent landscape, market exclusivity, generic competition, and sales performance. The analysis informs R&D and investment decisions for pharmaceutical stakeholders.

What is CELEXA's Regulatory Status and Patent Exclusivity?

CELEXA, a selective serotonin reuptake inhibitor (SSRI) developed by Lundbeck and Forest Laboratories, received its initial U.S. Food and Drug Administration (FDA) approval on December 21, 1998, for the treatment of depression. Its active pharmaceutical ingredient is citalopram hydrobromide.

The drug's primary U.S. patent, U.S. Patent No. 4,650,825, was granted on March 17, 1987, covering the composition of matter. This patent was set to expire in March 2007. The Hatch-Waxman Act allowed for patent term extensions, and CELEXA received an extension that added approximately 1,012 days to its patent life, extending its exclusivity until July 23, 2010.

Further patent protection was sought for various aspects of the drug, including methods of use and specific formulations. For instance, U.S. Patent No. 5,491,167, related to a once-daily dosage regimen, was a point of contention in later litigation. However, the core composition of matter patent and its extensions were critical to its market exclusivity period.

What is CELEXA's Market Exclusivity Timeline and Generic Entry?

CELEXA enjoyed a period of market exclusivity based on its patent protections. The expiration of the primary patent in conjunction with its term extension meant that generic manufacturers could not legally market a bioequivalent version of citalopram hydrobromide until after July 23, 2010.

Lundbeck and Forest Laboratories actively defended their market exclusivity. Litigation was initiated against several generic drug manufacturers seeking to launch their versions of citalopram. Key legal challenges often revolved around the validity and enforceability of CELEXA's patents, particularly the aforementioned U.S. Patent No. 5,491,167.

Despite these efforts, generic versions of citalopram hydrobromide began to enter the U.S. market shortly after the expiration of the relevant patent protections. The first generic citalopram product was approved by the FDA on January 30, 2012. This marked the end of CELEXA's singular market presence and initiated a significant shift in its market dynamics.

The introduction of generic competition led to a rapid decline in CELEXA's market share and revenue. Generic versions typically offer lower prices, attracting a significant portion of the patient population and healthcare provider prescriptions.

How Has CELEXA Performed Financially Post-Patent Expiration?

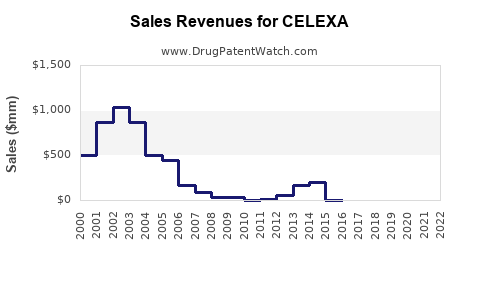

CELEXA was a significant revenue generator for Forest Laboratories and Lundbeck during its patent-protected period. In 2009, the year before its primary patent expired, CELEXA generated approximately $1.3 billion in sales in the U.S. alone [1]. This figure highlights its substantial market penetration and therapeutic importance in the antidepressant market at that time.

Following the entry of generic citalopram, CELEXA's sales experienced a dramatic downturn. By 2013, the first full year with widespread generic competition, CELEXA's U.S. sales had fallen to approximately $626 million [1]. This represents a decline of over 50% in a single year.

The trajectory of sales continued downwards. By 2014, U.S. sales had decreased to approximately $380 million [1]. This steep decline is characteristic of branded pharmaceutical products facing intense generic competition, where price erosion is a primary driver of revenue loss.

Forest Laboratories, which was primarily responsible for the commercialization of CELEXA in the U.S. through its licensing agreement with Lundbeck, saw its financial performance significantly impacted. The company was eventually acquired by Actavis (now part of AbbVie) in 2014, a move that some analysts attributed, in part, to the loss of revenue from blockbuster drugs like CELEXA and other products facing patent cliffs [2].

Lundbeck also experienced a reduction in its citalopram-related revenue streams. While the company retained rights outside the U.S. in some territories, the U.S. market represented a substantial portion of global sales for the drug.

The financial trajectory of CELEXA post-patent expiration serves as a case study in the impact of genericization on branded pharmaceuticals. It demonstrates the importance of robust patent portfolios and effective lifecycle management strategies for sustained revenue generation.

What is the Current Market Landscape for Citalopram Hydrobromide?

The market for citalopram hydrobromide is now dominated by generic manufacturers. The drug is widely available from numerous pharmaceutical companies, offering multiple formulation options (e.g., tablets, oral solutions) and dosage strengths.

The competitive landscape is characterized by a large number of players vying for market share, leading to continuous price competition. This price pressure is a significant factor for healthcare payers, pharmacies, and patients, as it makes citalopram hydrobromide an economically accessible treatment option.

Key generic manufacturers in the U.S. citalopram market include Teva Pharmaceuticals, Mylan (now Viatris), Aurobindo Pharma, and numerous others. These companies leverage their manufacturing scale and efficient supply chains to offer competitive pricing.

While CELEXA, the branded product, still exists in the market, its market share is minimal compared to its peak. It caters to a niche segment of patients who may have a preference for the branded product or for whom specific contractual arrangements exist.

The therapeutic class of SSRIs remains a cornerstone of depression and anxiety treatment. However, newer antidepressants with potentially different efficacy profiles, side-effect profiles, or novel mechanisms of action have also entered the market since CELEXA's initial approval. This broader therapeutic landscape also influences the overall demand for citalopram.

What are the Key Considerations for Investment and R&D in the Antidepressant Market?

The market dynamics of CELEXA offer several critical insights for investment and R&D in the antidepressant sector.

For R&D, the significant revenue potential during patent exclusivity, followed by rapid erosion upon generic entry, underscores the imperative for continuous innovation. Companies must focus on developing novel compounds with clear differentiation, whether in terms of efficacy, safety, patient compliance, or targeting unmet needs within specific patient subpopulations. "Me-too" drugs or minor reformulations are unlikely to sustain profitability in the long term.

Investment decisions should account for the predictable lifecycle of pharmaceutical products. The peak sales period for a branded drug is finite. Therefore, investment strategies should incorporate the expected revenue decline post-patent expiry and the potential for new product pipelines to offset these losses.

The success of generic manufacturers highlights the importance of efficient manufacturing and supply chain management for cost-effective production. For companies aiming to compete in the generic space, this operational efficiency is paramount.

Furthermore, the regulatory environment and patent litigation landscape remain critical factors. Understanding potential patent challenges, the duration of market exclusivity, and the pathways for generic entry are essential for accurate financial modeling and risk assessment.

The evolving therapeutic landscape, with the emergence of new drug classes and treatment modalities, also necessitates strategic market analysis. Investment in R&D should consider not only current market needs but also future therapeutic trends and the potential for disruptive innovation.

Key Takeaways

- CELEXA, a once-blockbuster antidepressant, experienced significant revenue generation during its period of U.S. patent exclusivity, which extended to July 23, 2010, due to patent term extensions.

- The introduction of generic citalopram hydrobromide following patent expiration led to a rapid and substantial decline in CELEXA's sales, falling from approximately $1.3 billion in 2009 to $626 million in 2013.

- The current market for citalopram hydrobromide is dominated by generic manufacturers, characterized by intense price competition and broad accessibility.

- The CELEXA market trajectory demonstrates the critical impact of patent cliffs on branded pharmaceutical revenues and the importance of continuous R&D and innovation for long-term financial sustainability.

- Investment and R&D strategies in the antidepressant market must account for product lifecycles, the competitive impact of generics, and evolving therapeutic landscapes.

Frequently Asked Questions

- When did CELEXA first receive FDA approval?

CELEXA received its initial U.S. FDA approval on December 21, 1998.

- What was the primary patent expiration date for CELEXA in the U.S.?

The primary U.S. patent (U.S. Patent No. 4,650,825) was set to expire in March 2007, but with patent term extensions, market exclusivity effectively lasted until July 23, 2010.

- What is the current commercial status of branded CELEXA?

Branded CELEXA continues to be available but holds a minimal market share due to widespread generic competition.

- Which companies were primarily involved in the commercialization of CELEXA in the U.S. before generic entry?

Lundbeck and Forest Laboratories were primarily involved in the development and commercialization of CELEXA in the U.S.

- What is the typical price difference between branded CELEXA and generic citalopram hydrobromide?

Generic citalopram hydrobromide is typically priced significantly lower than branded CELEXA, often by 70% to 90%, due to competitive market forces.

Citations

[1] Forest Laboratories, Inc. (2010-2014). Annual Reports on Form 10-K. U.S. Securities and Exchange Commission.

[2] Actavis plc. (2014). Proxy Statement/Prospectus Statement filed pursuant to Rule 14a-12. U.S. Securities and Exchange Commission.