Last updated: February 6, 2026

What Are the Market Dynamics for ATARAX?

Market Position:

Hydroxyzine, marketed as ATARAX, is an antihistamine used primarily for allergies, anxiolytic purposes, sedation, and nausea. The drug holds a niche position in the psychotropic and allergy markets, with global sales driven by its efficacy in short-term allergy relief and anxiety management.

Market Size & Segmentation:

The global antihistamine market totaled approximately USD 8.8 billion in 2022, with hydroxyzine accounting for a small but steady portion. The U.S. holds roughly 40% of this market, with Europe and Asia-Pacific following. The anxiolytic segment within antihistamines is growing due to rising stress-related disorders.

Demand Drivers:

- Increasing prevalence of allergic rhinitis and anxiety disorders.

- Growing awareness of mental health treatment options.

- Preference for off-label sedation uses in surgical or diagnostic procedures.

Competitive Landscape:

Hydroxyzine competes with newer agents like cetirizine and loratadine, which lack sedative effects. It also faces competition from benzodiazepines in anxiety treatment. The drug’s demand persists where rapid sedative or anti-itch effects are needed.

Regulatory Environment:

Hydroxyzine is available via prescription in most markets. Regulatory controls focus on its sedative potential and misuse risk, potentially limiting distribution channels.

Pricing & Reimbursement:

Pricing varies regionally; in the U.S., generic formulations cost approximately USD 10-20 per tablet. Reimbursement depends on specific insurance coverage and formulary placement.

What Is the Financial Trajectory of ATARAX?

Sales Trends:

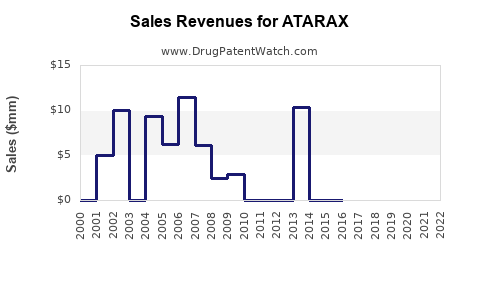

Between 2018 and 2022, ATARAX's sales have been relatively flat with slight declines in mature markets due to generic competition. In the U.S., sales estimated at USD 50-70 million annually. Global sales accounting for all formulations can reach USD 100 million, but this includes off-label and institutional uses.

Patent and Market Exclusivity:

Hydroxyzine patents have expired, exposing the drug to generic competition. No current patent protections significantly extend the drug's market exclusivity, which constrains profitability.

Impact of Generics:

The entry of multiple generics since the mid-2000s has driven prices down. Manufacturers now rely on volume rather than premium pricing. The loss of patent exclusivity in major markets has limited growth prospects.

Revenue Forecasts:

- Short-term (1-3 years): Moderate decline due to market saturation and competition.

- Mid-term (3-5 years): Stabilization expected if new formulations or combination products are introduced.

- Long-term (beyond 5 years): Decline anticipated unless driven by new indications or market repositioning.

Investment & Development Outlook:

No significant pipeline or reformulation initiatives are currently public. R&D efforts tend to focus more on drugs replacing antihistamines due to safety concerns or broader spectrum antihistamines.

What Factors Influence the Future of ATARAX?

- Regulatory Changes: Stricter controls on sedatives or anxiolytics could restrict use.

- Market Penetration: Potential expansion into emerging markets may offer growth opportunities.

- Medical Trends: Shift towards non-sedating antihistamines and the decline of off-label sedative use could erode demand.

- Competition: The rise of newer agents may reduce ATARAX's relative market share.

Summary

Hydroxyzine (ATARAX) operates within a mature, highly competitive antiviral and allergy treatment landscape. Its sales are constrained by generic competition and a limited pipeline. Future growth depends on market expansion, potential new indications, or reformulations, none of which currently hold high development priority.

Key Takeaways

- The global antihistamine market was USD 8.8 billion in 2022, with hydroxyzine representing a small fraction.

- Due to patent expiration, generic competition has driven prices down and sales mainly rely on volume.

- ATARAX's annual global sales are estimated between USD 50-100 million, with a declining trend in mature markets.

- Future prospects depend on market expansion, regulatory changes, and shifts in medical practice away from sedative antihistamines.

- No current pipeline initiatives signal limited near-term growth for ATARAX.

FAQs

1. Can ATARAX regain market exclusivity?

No. Patent protections have long expired, and no new patents are in process to extend exclusivity.

2. Are there regulatory risks that could affect ATARAX?

Yes. Changes in regulations surrounding sedatives and anxiolytics could restrict its use.

3. What are key competitors to hydroxyzine?

Non-sedating antihistamines like cetirizine, loratadine, and newer anxiolytics like benzodiazepines.

4. Is there potential for new indications for ATARAX?

Limited current pipeline activity suggests low prospects unless new research demonstrates additional uses.

5. How might market expansion impact future sales?

Emerging markets could provide growth avenues, but price sensitivity and regulatory hurdles may limit upside.

Sources

- MarketWatch, "Antihistamines Market Size, Share & Trends," 2023.

- IQVIA, Global Prescription Drug Sales Data, 2022.

- FDA, Drug Approval & Patent Data, 2023.