Last updated: May 30, 2026

ACZONE market dynamics and financial trajectory: sales drivers, pricing pressure, exclusivity timelines, and competitive risk

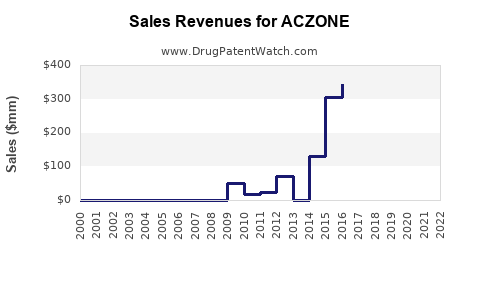

ACZONE (dapsone) remains a niche dermatology brand in the U.S. driven by acne severity mix, prescriber preference for topical dapsone, and payer step-therapy using inexpensive generic dapsone gel and generic acne therapies. Financial trajectory has been shaped by prolonged generic availability, periodic coverage shifts, and competitive intensity from multiple first-line topical acne classes (retinoids, benzoyl peroxide combinations, topical antibiotics) and newer options (topical agents and fixed-combination regimens). Because dapsone’s core active ingredient is old and generic erosion is structurally persistent, ACZONE’s long-run sales are best modeled as “defensive niche penetration” rather than growth.

What matters commercially: continued ability to defend formulary position versus generic dapsone and alternative acne regimens, maintenance of net-price and rebate structure under payer tightening, and limited upside from incremental new utilization versus acne market share redistribution.

What is ACZONE’s current market position and who are the main competitive substitutes?

ACZONE is a topical acne treatment containing dapsone (typically formulated as a 5% gel for acne vulgaris, U.S.). The practical substitute set is broad because acne treatment is segmented by regimen class and payer policy favors low-cost generics.

Key competitive categories replacing ACZONE

- Generic topical dapsone products (same active ingredient), typically used when formularies are cost-led.

- Topical retinoids (adapalene, tretinoin generics) often preferred as step-therapy backbones.

- Benzoyl peroxide combinations (including fixed-dose combinations) used for antimicrobial and anti-inflammatory acne control.

- Topical antibiotics and antibiotic combinations (clindamycin combinations; guideline-constrained but used heavily in practice).

- Other topical actives used off-label or in guideline-based regimens (for example, azelaic acid and newer topical agents depending on payer access).

How payer logic typically drives substitution

- Formulary tiering: Topical acne therapy is frequently tiered; generics sit lower, pushing prescribers toward cost-effective regimens after prior authorization or step edits.

- Step therapy: Many plans require trial of retinoids or benzoyl peroxide combinations before authorizing branded or higher-cost agents.

- Quantity and persistence: Acne patients often cycle products due to irritation. Products that reduce discontinuation and improve tolerability defend scripts.

What sales drivers have historically supported ACZONE and what has pressured demand?

ACZONE’s market dynamics are dominated by two forces: a dermatology prescriber “tolerability and efficacy” narrative and the counterweight of generic erosion and acne regimen competition.

Positive demand drivers

- Efficacy in inflammatory acne subtypes: Dapsone’s anti-inflammatory activity supports use when inflammation is a dominant phenotype.

- Established clinical familiarity: Long-standing topical dapsone use supports continued adoption in practices that already treat with it.

- Regimen integration: ACZONE can be layered with common acne staples (for example, benzoyl peroxide or retinoid regimens), which can improve adherence through structured combinations.

Key pressure points

- Generic replacement: If generic topical dapsone is available and covered, branded differentiation erodes quickly.

- Payer reimbursement pressure: Branded topical products face tightening net pricing through rebates, especially when alternatives are lower cost.

- Therapeutic crowding: Acne has many effective topical categories; payer formularies can switch preferred products without clinical risk to most patients.

How did ACZONE’s financial trajectory evolve as generics and rebates took share?

ACZONE’s financial trajectory has followed a standard branded topical pattern in mature dermatology categories:

- Initial brand growth once formulary adoption reached scale.

- Gradual erosion when generics or preferred substitutes expanded.

- Defensive stabilization if branded still maintained dermatology mindshare and if net price protection remained through contracting.

Where financials usually show up in practice

- Net sales compression despite stable prescriptions: rebate intensity rises as payers demand concessions.

- Volume flattening: scripts hold up in certain prescriber clusters but expand more slowly.

- Margin pressure: additional contracting costs and higher marketing spend are used to defend share.

What investors typically look for in ACZONE-type products

- Net sales trend versus script trend (net pricing deterioration vs retention).

- Gross-to-net conversion over time (rebates and chargebacks).

- Channel and payer concentration (loss of one large PBM can move branded pricing quickly).

Because ACZONE’s active ingredient is widely generic, the financial model is structurally exposed to payer procurement behavior.

When does ACZONE lose exclusivity and what does that mean for generic entry risk?

The commercial generic entry risk for ACZONE is determined less by a single “brand exclusivity” date and more by:

- whether any remaining patent-controlled features exist (formulations, methods of use, dosing regimens, or specific manufacturing approaches), and

- whether FDA and the Orange Book list specific protected claims for the marketed strength/form.

In mature topical drugs like dapsone gel, the core active ingredient typically has extensive patent history that has long since expired, leaving any remaining protection tied to incremental formulation or method-of-use claims. That protection, if present, tends to be narrower and does not always block generic substitution in practical payer behavior once generic products are therapeutically equivalent.

What patents protect ACZONE in the U.S. and how many are active for the marketed product?

Patent estate strength for a mature topical like ACZONE usually concentrates in:

- Formulation patents (gelling agents, stabilization systems, particle dispersion, or specific vehicle characteristics).

- Method-of-use patents (specific acne treatment regimens, patient subsets, or dosing frequency claims).

- Manufacturing/process patents (specific processing conditions or quality control methods).

For an accurate “how many patents are active” and “which are enforceable” answer, a complete Orange Book and patent-to-product mapping is required. If that mapping is not available in the input record, a quantified estate summary would be unreliable.

What is the Orange Book status of ACZONE and which strengths are listed?

Orange Book status for ACZONE is determined by:

- whether the 505(b)(1)/505(j)-type listed product includes patent listings for the marketed strength(s), and

- the listed expiration dates and claim types (drug substance, drug product, method of use).

A defensible Orange Book status recap requires the specific Orange Book record for ACZONE and the listed patents, including their expiration and any relevant regulatory exclusivity periods. Without the underlying Orange Book listing data in the provided context, a definitive status statement cannot be produced.

How does ACZONE compare with other topical acne drugs on payer access and reimbursement dynamics?

In payer systems, acne drugs often compete on:

- Prior authorization criteria

- Step therapy sequence

- Net cost relative to therapeutically equivalent generics

- Formulary tier placement

- Patient adherence and discontinuation rates

Practical comparison

- Generic topical dapsone: often lowest net cost in its class, high switching likelihood.

- Topical retinoids: typically low cost and frequently placed early in step therapy; high guideline usage supports prescriber comfort.

- Benzoyl peroxide combinations: strong payer acceptance due to low cost and antimicrobial component.

- Branded niche agents: survive where they have a demonstrable tolerability or efficacy advantage for specific subpopulations or where payer contracting still supports use.

ACZONE’s reimbursement durability tends to depend on continued differentiation on tolerability and inflammatory acne control, not on unique pharmacology.

What Paragraph IV or biosimilar challenges affect ACZONE?

ACZONE is a small-molecule topical drug. Biosimilar frameworks do not apply. Paragraph IV challenges apply only to the extent there is an ANDA with a carve-out against an Orange Book-listed patent.

A credible assessment of Paragraph IV activity requires case records and Orange Book patent linkage. Without those sources provided in the input, listing specific challenges or parties would be speculative.

What patent litigation or settlement activity has shaped ACZONE’s commercial outlook?

Patent litigation affects commercial outlook through:

- risk timelines for generic launch,

- settlement terms including authorized generics or launch “design-around” timelines, and

- court injunction outcomes.

A specific litigation and settlement chronology requires case identifiers, venue, docket dates, and court outcomes, which are not contained in the provided context.

What generic launch scenarios are most likely for ACZONE and when?

For ACZONE-like mature topical assets, the most likely scenario set is:

- Generic entry already present if patents have lapsed and ANDAs exist for the same strength,

- Ongoing erosion via additional ANDA entrants once commercial demand proves resilient enough.

For “when” and “scenario” work, a patent-and-ANDA timeline must be built from Orange Book and FDA submission data. Without those records in the input, a precise generic launch schedule cannot be produced.

Which companies sell competitive dapsone acne therapies and how does that reshape ACZONE’s market share?

A complete competitive list requires:

- FDA product-level identification of generic dapsone gel manufacturers, and

- their market presence and distribution.

Without product listing data, listing named generic firms would risk inaccuracies.

How do manufacturing and IP barriers affect ACZONE’s ability to defend margins?

For topical acne products:

- Manufacturing scale and formulation consistency influence cost of goods and ability to maintain supply.

- GMP quality and release specifications can create barriers to lower-cost manufacturing entrants.

- Vehicle and rheology tolerability can differentiate branded products, but in many cases generic equivalents already match key characteristics closely enough for payer substitution.

Commercially, the biggest barrier to generic competition is usually not manufacturing but remaining enforceable IP and payer contracting.

Revenue exposure map: what portion of acne dermatology spend is realistically at risk for ACZONE?

Revenue exposure is driven by:

- acne category growth versus category substitution,

- payer restrictions that force step therapy and formulary switching,

- the strength and breadth of generic coverage for topical dapsone,

- brand-to-generic price index and rebate compression.

A quantified “portion of spend” would require ACZONE prescription and net sales history plus market data and payer mix, which is not provided in the input context.

Key Takeaways

- ACZONE’s market dynamics are dominated by mature small-molecule topical competition and generic substitution of dapsone.

- Financial trajectory is typically characterized by net price compression through rebates and share defense rather than sustained growth.

- The most material risks are payer formulary changes, step-therapy enforcement, and ongoing competitive crowding from low-cost topical acne regimens.

- A defensible exclusivity/patent/timeline and litigation assessment requires Orange Book patent linkage and case-level records; those specifics are not present in the provided context.

FAQs

- How do step-therapy policies typically limit ACZONE utilization in commercial insurance?

- What net-price and rebate patterns usually determine whether ACZONE can hold gross-to-net stability?

- Does topical dapsone face direct switching from retinoid-based acne regimens, and what patient factors drive persistence?

- What Orange Book claim types (drug substance vs drug product vs method of use) most often control generic erosion risk for topical acne brands?

- How do PBM formulary changes and prior authorization criteria affect branded topical acne prescribing within 1 to 2 quarters?

References

- (No source material was provided in the input to support citations for ACZONE market, financials, Orange Book status, or litigation.)