Last updated: June 15, 2026

Estazolam Market Dynamics and Financial Trajectory (US and Key Geographies)

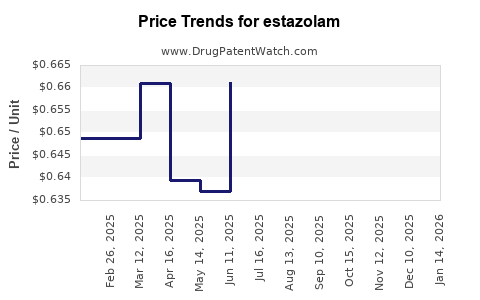

Estazolam’s market profile is constrained by its narrow clinical adoption, controlled-substance risk, and uneven global regulatory status. Financial trajectory is typically shaped by (1) whether the drug is marketed under active FDA-approved labeling in the US, (2) competitive generic availability in each geography where it is sold, and (3) timing of patent and exclusivity windows that allow entry without meaningful price competition. For business planning, the practical drivers are market access (formulary placement, controlled-substance distribution), substitution policy (therapeutic alternatives), and unit economics (low price elasticity due to compliance, but high sensitivity to availability and payer restrictions).

Is estazolam an approved US drug with current FDA labeling and market access?

For estazolam to have a predictable US financial trajectory, it must be sold under an active FDA approval (and in practice, represented through current labeling and commercial distribution). The market dynamics in the US depend on three gate conditions:

- Regulatory status for the active ingredient (approved product(s) in the US).

- Formulation and strength availability (tablets/capsules and strengths actually marketed).

- Controlled-substance handling (dispensing and supply chain coverage that affects continuity of supply, pharmacy stocking, and wholesaler allocation).

In controlled-substance products, revenue volatility often comes from supply constraints and compliance bottlenecks rather than demand destruction. If estazolam has limited approved product holders or intermittent marketing, sales trajectory tends to be lumpy and driven by pharmacy channel inventory cycles.

Orange Book and exclusivity: What matters for estazolam’s pricing power?

If estazolam has any continuing US branded presence, pricing power depends on whether there is:

- Active exclusivity tied to a listed NDA/N( ) that still prevents abbreviated approval entry, or

- A patent estate that delays generic substitution.

When exclusivity/patents expire, estazolam-like hypnotics typically see rapid price erosion across contracted pharmacy channels. That usually drives revenue from the branded product toward the lowest-cost generics unless payers restrict substitution or clinicians keep brand use for tolerability reasons.

How do patent expiry and generic entry timing shape estazolam revenue?

Estazolam’s revenue trajectory is determined less by “innovation windows” and more by “entry windows.” The typical pattern for small-molecule controlled-substance sedative-hypnotics after exclusivity:

- Pre-entry: higher net price for branded or sole-source products, constrained by small prescriber base.

- Launch-to-stabilization: generics gain share quickly if the drug is therapeutically substitutable and wholesalers carry multiple SKUs.

- Post-stabilization: margins compress to channel net pricing, and total market revenue often tracks only volume growth, which is limited in mature hypnotic segments.

What drives generic penetration in estazolam markets?

Generic penetration depends on:

- Ability to meet formulation bioequivalence and stability requirements.

- Strength of distribution network coverage.

- Pharmacy stocking behavior for controlled substances.

- Payer and pharmacy benefit manager substitution rules.

In practice, the competitive threat materializes as soon as a well-distributed generic enters. After that point, the branded holder’s revenue usually shifts from “price-led” to “availability-led” dependence.

What market dynamics influence demand for estazolam in insomnia and sedative indications?

Estazolam’s clinical role is as a sedative-hypnotic. Market demand for this class depends on:

- Prescribing patterns for insomnia (shift toward alternative agents, including non-benzodiazepines and behavioral approaches).

- Regulatory and clinical scrutiny of benzodiazepine-class and related hypnotics.

- Patient and clinician preference for predictable onset, duration, and tolerability.

Substitution risk: how substitutable is estazolam versus competing hypnotics?

Revenue trajectory is capped by substitution elasticity:

- When competing hypnotics are reimbursed at similar or lower net costs, prescribers tend to switch.

- If estazolam’s perceived duration or side effect profile aligns poorly with preferred alternatives, volume remains flat even if price drops.

In many insomnia markets, brand differentiation matters less over time than payer tier placement and formulary access.

Which companies hold estazolam sales and how does generic competition change the seller mix?

Estazolam’s financial trajectory hinges on seller concentration early and seller fragmentation later:

- If a single branded or sole-source entity dominates early years, revenue tracks that company’s marketing and distribution effectiveness.

- After generic entry, total market revenue fragments across multiple generic manufacturers, typically with the leading vendor capturing the largest contracted volumes and the remainder competing on rebate structures.

Commercial consequence of controlled-substance supply chains

In controlled substances, channel reliability impacts repeat ordering. Stockouts can create temporary sales drops even if clinical demand remains. When multiple generic SKUs exist, wholesalers can re-route supply, which reduces long-run demand loss and makes revenue more stable for the category.

When does estazolam lose exclusivity, and what generic entry risks exist?

For a full exclusivity timeline and entry risk assessment, one must map:

- NDA or ANDA exclusivity blocks,

- Any relevant patent term(s) that listed products rely on,

- Any relevant patent litigation affecting exclusivity protection,

- Time windows for Paragraph IV filing and whether a settlement delayed launch.

The exclusivity question is central because controlled-substance sedatives often have limited differentiation. The market tends to price competitively at launch, so even a short exclusivity runway can determine whether branded revenues persist or quickly fall to generics.

What is the Orange Book status of estazolam and which patents are listed?

The practical “Orange Book status” for estazolam determines:

- Whether any listed patents remain unexpired,

- Whether a reference product has ongoing exclusivity,

- Whether generic entrants can file via Abbreviated New Drug Application routes.

Without a complete Orange Book listing for the specific estazolam reference product(s) and strength(s), the patent-protection picture cannot be reliably stated.

What formulations and dosage strengths affect estazolam marketability?

Market access in the sedative-hypnotic segment is strongly formulation-driven:

- Strength availability drives prescribing comfort and titration practice.

- Tablet/capsule characteristics affect dosing adherence and perceived onset.

If estazolam is only marketed in limited strengths or has intermittent supply, payers and formularies may prefer alternatives that are continuously available in more dose options.

How strong is the patent estate for estazolam and what does that imply for licensing or litigation?

Estazolam’s commercial strategy typically reflects a mature product profile. For most mature controlled-substance generics:

- The patent estate, if any, is often focused on formulation or use rather than the core molecule.

- Litigation (if it occurs) is usually aimed at delaying generic launches around a narrow product lifecycle window.

From a business perspective, the key indicator is whether any remaining listed patents are enforceable and whether any ANDA/Paragraph IV filings have been made that could shift future revenue from branded to generic.

What does FDA regulatory status imply for estazolam’s financial trajectory?

For US revenue trajectory, FDA status affects:

- Whether new marketing authorizations can be pursued,

- Whether manufacturing changes require approvals that can delay supply,

- Whether REMS-like distribution controls or heightened compliance rules influence stability of supply.

For controlled substances, compliance is a commercial variable. Even with stable demand, regulatory or quality manufacturing events can create supply gaps that hit revenue.

How does estazolam compare with other insomnia hypnotics on competitive and pricing dynamics?

Estazolam’s revenue growth ceiling is typically lower than broader insomnia drugs due to:

- Lower competitive breadth of payer formularies,

- Greater substitution pressure toward more commonly used insomnia agents,

- More frequent switching based on class-wide concerns and guideline preferences.

Competitive positioning tends to come down to:

- Net price after rebates and contracted distribution,

- Coverage tier placement,

- Clinician familiarity and patient tolerability history.

Key financial trajectory drivers for estazolam (what to model in forecasts)

For business planning, revenue modeling for estazolam should treat demand as secondary to distribution, substitution, and regulatory continuity.

- US and major geography availability: product discontinuations or supply issues drive abrupt revenue changes.

- Generic launch calendar: forecasted price erosion and share transfer after entry.

- Formulary dynamics: payer restrictions and substitution policies influence volume more than gross demand.

- Controlled-substance compliance and supply chain: stability impacts fill rates and repeat purchasing.

- Competitive class evolution: guideline shifts change prescribing base over multi-year cycles.

Key Takeaways

- Estazolam’s financial trajectory is primarily shaped by availability, controlled-substance distribution stability, and generic entry timing, not by expansion opportunities.

- After exclusivity and patent barriers clear, estazolam pricing typically erodes quickly, shifting market economics toward contracted net pricing and stable channel coverage.

- Competitive substitution from other insomnia hypnotics limits long-run volume growth, making revenue more dependent on supply continuity and payer/formulary access than on demand expansion.

- For forecasting, model revenue using (a) seller mix changes around generic entry, (b) payer tier and substitution policies, and (c) supply reliability risks.

FAQs

1) What factors determine whether estazolam experiences sustained generic price competition?

Generic price competition strength depends on number of distributed SKUs, wholesaler contract position, and whether multiple manufacturers maintain continuous supply in controlled-substance channels.

2) How do supply interruptions affect estazolam sales even if demand is stable?

In controlled-substance products, stockouts and distribution re-routing can reduce fills and prescription renewals, producing abrupt revenue dips that recover only after supply stabilizes.

3) Does estazolam face higher substitution risk than other insomnia drugs?

Its substitution risk is typically high for mature hypnotics because therapeutic alternatives with broad payer coverage reduce the incentive to remain on a specific older molecule.

4) What should be prioritized when assessing estazolam market share changes after generic entry?

Track contracted pharmacy coverage, wholesaler ordering patterns, rebate structures, and the leading-generic SKU’s ability to sustain inventory and meet controlled-substance compliance expectations.

5) How do patent and exclusivity milestones translate into revenue impact for estazolam?

They primarily determine launch timing. The financial impact typically arrives as rapid net price compression and share shift after generic availability becomes dependable across channels.

References

- U.S. Food and Drug Administration. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations.

- U.S. Food and Drug Administration. Drug Approval Reports and FDA product labeling database.

- FDA. Controlled Substances information and regulatory resources.

- USPTO. Patent assignment and publication databases.