Last updated: April 25, 2026

Diclofenac epolamine is a topical NSAID used for localized pain and inflammation, most commonly in patches and gels. The market is driven by (1) broad OTC and prescription penetration in multiple geographies, (2) recurring demand for musculoskeletal pain management, and (3) intense generic competition once patents lapse. The financial trajectory for brands has been shaped by sustained volume stability with margin compression, while manufacturers with differentiated delivery systems (notably adhesive patch platforms) have tended to preserve pricing power longer in specific markets.

What are the market dynamics shaping diclofenac epolamine demand?

1) Indication profile supports recurring musculoskeletal use

Diclofenac epolamine is used for local relief of pain associated with strains, sprains, and other soft tissue injuries and musculoskeletal discomfort. This is a high-frequency care category because patients cycle through conservative pain management repeatedly rather than requiring one-off interventions.

Key demand attributes:

- Localized therapy: targets peripheral pain with reduced systemic exposure versus oral NSAIDs in the same class, which supports adherence and repeat purchases where available.

- Seasonality is modest: demand ties to year-round musculoskeletal complaints rather than single-season conditions (contrast with allergy/flu products).

- Site-of-action familiarity: diclofenac is a well-established active ingredient, supporting pharmacy stocking and clinician familiarity.

2) Delivery-form differentiation remains a competitive lever

Manufacturers compete less on mechanism and more on delivery mechanics:

- Adhesive patch platforms (common in diclofenac epolamine markets) compete on wear time, adhesion, skin tolerability, and dosing convenience.

- Gels/creams compete on spreadability, dosing flexibility, and user preference.

In practice, brands that defend a specific formulation (or presentation) often keep a partial moat in markets where pharmacists and prescribers differentiate by “product feel” and application behavior rather than only active ingredient.

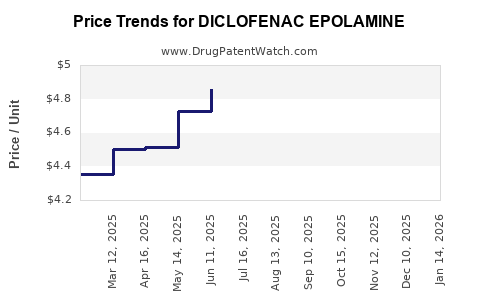

3) Generic entry compresses price after patent/brand exclusivity

Diclofenac epolamine’s financial performance follows the classic pattern seen across topical NSAIDs:

- Pre-generic period: brand-led pricing with promotional spend.

- Post-generic entry: unit volumes usually remain, but net sales per unit decline as retailers and payers shift to lower-priced alternatives.

- Post-exclusivity stabilization: companies with scale and strong distribution can sustain sales, but operating margins typically shrink.

This dynamic is reinforced by the regulatory environment for topical NSAIDs, where bioequivalence pathways and formulation comparability often facilitate faster generic competition versus novel molecular entities.

4) Payer and channel mix drives volatility in realized pricing

Realized pricing differs by channel:

- Pharmacy retail: tends to keep volumes resilient even when pricing falls, because consumers substitute within the class.

- Prescription reimbursement: introduces payer formulary placement risk and more rapid switching to lowest-cost options once alternatives are available.

- Hospital/clinic procurement (where applicable): tends to be batch/contract driven, which accelerates competitive pricing.

For diclofenac epolamine, net sales performance is typically more sensitive to country-specific reimbursement rules and tender pricing than to marginal changes in clinical demand.

How has the competitive landscape evolved across regions?

United States

The U.S. topical NSAID market is mature and heavily genericized. Competitive intensity is high across diclofenac products (and across NSAIDs generally), which pressures price and promotional efficiency. Brand profitability tends to track (a) remaining exclusivity windows for branded formulations and (b) performance in high-velocity retail segments.

Europe

Europe commonly supports both OTC access (depending on country) and pharmacy/channel mix, which increases consumer switching within the topical NSAID class. Market outcomes frequently depend on:

- packaging/presentation,

- clinician preference for patch versus gel,

- and local regulatory status (OTC vs prescription).

Other markets (Asia, LATAM, MENA)

These geographies often show:

- faster uptake of generics,

- price-driven competition,

- and uneven reimbursement structures.

In these regions, the financial trajectory usually reflects the timing of generic filings and local scale of distribution rather than sustained brand strength.

What is the likely financial trajectory of diclofenac epolamine products?

1) Brand sales pattern: volume stability, margin compression

From a financial standpoint, diclofenac epolamine typically exhibits:

- Sustained unit demand for localized pain,

- erosion of gross-to-net over time from generic substitution and payer pressure,

- and declining operating margins unless offset by cost reductions, mix shifts, or differentiated delivery platforms.

A common outcome in mature topical analgesics is that companies preserve market share but face declining contribution margins as wholesale and retail prices track toward generic benchmarks.

2) Product lifecycle is governed by formulation patents and exclusivity

Even when the API is well-established, financial outcomes hinge on:

- formulation-specific IP,

- device/patch attachment technology (where relevant),

- marketing authorization scope (indication and dosing regimen),

- and country-by-country exclusivity and regulatory review timelines.

Once formulation or presentation exclusivity ends, the market often transitions rapidly to branded generics and then to lower-priced generics.

3) Revenue concentration tends to be market-level, not molecule-level

Because diclofenac epolamine is sold as presentations (patches, gels), revenue concentration usually tracks:

- which countries support a strong channel position for that specific product,

- distribution partnerships,

- and the degree to which competitors occupy the same shelf space.

That makes the financial trajectory sensitive to distribution losses, tender outcomes, and pharmacy stocking behavior.

What KPIs matter most for diclofenac epolamine performance?

Commercial KPIs

- Share of shelf / prescription share in topical NSAIDs (country-specific)

- Net price and gross-to-net (rebates, discounts, professional pricing)

- Retail velocity for patches vs gels

- Formulation mix (patches typically command different pricing than gels, depending on market norms)

Financial KPIs

- Gross margin trend as generic share increases

- SG&A efficiency (promotion needs rise as prices fall)

- COGS and manufacturing utilization (patch manufacturing economics matter)

- Portfolio overlap with other topical diclofenac presentations

Regulatory KPIs

- Exclusivity windows and generic entry timing

- OTC vs prescription status changes

- label expansion or contraction affecting formulary decisions

How does generic competition typically affect profitability versus revenue?

Revenue

Revenue can remain stable when:

- unit demand persists in musculoskeletal indications,

- consumers switch within topical NSAIDs without abandoning therapy,

- and distribution is maintained.

Profitability

Profitability usually falls because:

- pricing resets downward,

- promotional intensity increases,

- and manufacturing scales are less favorable if demand fragments across many SKUs.

In mature topical analgesics, the best-performing companies are typically those that:

- sustain scale manufacturing,

- maintain distribution leverage,

- and keep differentiated product presentation in select markets.

What does the historical regulatory and market positioning imply for future trajectory?

Known properties of diclofenac epolamine support steady demand

Diclofenac is widely used and has entrenched prescriber and patient familiarity. The epolamine salt form supports topical delivery and is aligned with localized treatment preferences.

Regulatory history matters because:

- where the drug is marketed as OTC, volume can hold up better during price wars,

- where it is prescription-driven, payer decisions accelerate switching.

Future outlook depends on market structure

The next phase is likely to be characterized by:

- further generic penetration in high-income markets,

- incremental growth from emerging country distribution,

- and margin-led consolidation (where manufacturers reduce SKUs and focus on high-velocity formats).

Key Takeaways

- Diclofenac epolamine demand is anchored in recurring musculoskeletal pain management and localized self-care behavior.

- The competitive battleground is formulation and presentation (patch vs gel), not the mechanism.

- Financial trajectory typically shows volume resilience with sustained margin compression as generics expand.

- Net sales performance is most sensitive to realized pricing, reimbursement rules, and country-by-country tender or formulary dynamics rather than to changes in underlying clinical demand.

FAQs

1) Is diclofenac epolamine primarily a prescription or OTC product?

It varies by market. In many regions it is sold via pharmacy channels and may be available OTC depending on local regulatory status.

2) What delivery form tends to perform better commercially?

Patch versus gel outcomes differ by country and channel. Patch platforms often maintain differentiation via wear time and user preference, while gels typically compete more directly on price per gram.

3) What drives revenue erosion after exclusivity ends?

Generic substitution and formulary pressure compress net prices. Gross-to-net can worsen as promotional intensity increases and channel partners demand higher discounts.

4) Does generic entry usually kill total demand?

Usually not. Topical NSAIDs often retain unit demand because patients substitute within the class rather than stop localized pain treatment.

5) What is the main determinant of long-run profitability?

Manufacturing scale, SKU efficiency, distribution leverage, and the ability to preserve differentiated presentation in markets where substitution is less immediate.

References

[1] European Medicines Agency. Diclofenac epolamine product information / EPAR and related assessment documents for diclofenac epolamine-containing medicines. EMA website.

[2] U.S. Food and Drug Administration. Drug approvals and labeling information for diclofenac topical products (including products with diclofenac epolamine). FDA Drug Databases.

[3] World Health Organization. ATC classification information for diclofenac and topical NSAID categories. WHO Collaborating Centre for Drug Statistics Methodology (ATC/DDD).

[4] RxList / MedlinePlus (drug monographs). Clinical use and administration overview for diclofenac topical formulations. National Library of Medicine and related medical resources.

[5] PubChem. Diclofenac epolamine compound and formulation identifiers. U.S. National Library of Medicine, PubChem database.