Last updated: July 27, 2026

Flector (diclofenac epolamine) Market Dynamics and Financial Trajectory: Sales Drivers, Pricing, Competition, and Loss-of-Exclusivity Timeline

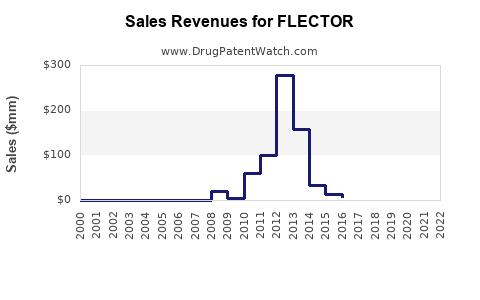

Flector (diclofenac epolamine) is an older nonsteroidal anti-inflammatory drug (NSAID) delivered as a transdermal topical patch. Its U.S. market trajectory is dominated by (1) long-run erosion from generic diclofenac topical products, (2) payor-driven formulary pressure and step edits across musculoskeletal indications, (3) limited patent leverage typical of legacy topical NSAIDs, and (4) ongoing demand elasticity tied to health-plan coverage and patient adherence to patch-based therapy. Financial performance has been constrained by generic substitution and the absence of sustained brand protection.

Current market posture (what matters for revenue)

- Flector’s revenue is most sensitive to: commercial coverage, copay tiers, and substitution to AB-rated generic diclofenac patch/solution/gel formats.

- The patch category’s economics are shaped by pharmacy benefit manager (PBM) formulary strategy and therapeutic alternatives (oral NSAIDs, topical gels, lidocaine, physical therapy).

- Brand differentiation is clinically incremental versus multiple AB generics and other topical NSAIDs.

How has Flector performed financially in the US market (sales trends, revenue drivers, and downside risks)?

Featured snippet answer: Flector’s financial trajectory in the U.S. has been structurally pressured by generic substitution of diclofenac topical NSAIDs, with revenue performance tracking PBM formulary placement and patient adherence to patch therapy.

Key market dynamics shaping revenue

-

Generic substitution

- Flector is exposed to AB-category switching within topical diclofenac. Generic entry typically transfers demand from brand to lower-priced equivalents once exclusivity and brand-patent shelter ends.

- For legacy topical products, brand units can remain stable for a time due to “channel habit,” but pricing pressure drives revenue erosion faster than unit stability.

-

PBM and formulary placement

- Topical NSAIDs compete on copay, prior authorization (less common for topicals than some specialty classes), and therapeutic interchange policies.

- Step therapy is more likely to favor cheaper topical options (diclofenac gel/solution) before patches, depending on plan design.

-

Adherence and administration

- Patch therapy requires correct wear time, application discipline, skin tolerance management, and replacement scheduling.

- That creates a practical friction versus once-daily/optimized gel regimens, which can influence persistence and refill rates.

-

Safety communications and class-wide scrutiny

- NSAIDs carry cardiovascular and GI risk messaging. Even though topical systemic exposure is lower than oral, class perceptions can influence prescriber and patient behavior.

- Any safety-related label evolution for diclofenac can shift preference within the NSAID topical class.

Commercial downside risks

- Increased tiering pressure if PBMs expand generic preference lists for diclofenac topicals.

- Channel inventory adjustments and wholesaler restocking cycles that can distort quarterly sales optics.

- Shift in clinical practice toward alternative topical modalities (diclofenac gel, diclofenac solution, lidocaine patches, compounded topical NSAID blends where permitted).

What is the competitive landscape for diclofenac topical patches (Flector vs generics and other topical NSAIDs)?

Featured snippet answer: Flector’s main competitive set is AB-rated diclofenac topical alternatives (generic diclofenac epolamine patches) plus other topical NSAID formats and competing localized pain products.

Direct substitution set (same molecule, comparable therapy class)

- Generic diclofenac epolamine patch SKUs (AB-rated).

- Diclofenac topical products in other dosage forms (gel/solution) that PBMs often place on preferred tiers.

- Other topical analgesics:

- Lidocaine patches

- Topical capsaicin in relevant neuropathic pain contexts

- Counterirritant topical products (limited overlap clinically)

Indirect competitive set (therapeutic alternatives)

- Oral NSAIDs (short course, where risk is acceptable)

- Physical therapy and adjunct modalities

- Local injections and other procedures in specific musculoskeletal pathways

How competitors typically win

- Lower WAC and net pricing through generic entry.

- Formulary inclusion on preferred tiers and removal from nonpreferred tiers.

- Prescriber habit transfer to easier-to-use formulations (gel/solution) depending on coverage.

What patents protect Flector (diclofenac epolamine) and how strong is the patent estate?

Featured snippet answer: Flector’s ability to sustain brand pricing has historically depended on a limited set of composition, formulation, and use protections for a topical diclofenac patch product. After generic pathways stabilize, the competitive threat is largely AB substitution.

Patent estate characteristics typical for legacy topical NSAID brands

- Brand patents for transdermal delivery systems tend to be finite and can expire earlier than consumers expect based on the product’s market age.

- Generic manufacturers often pursue “design-around” where needed, but for AB diclofenac equivalents, they can rely on regulatory bioequivalence standards rather than needing breakthrough IP.

Practical implication for investors and litigators

- The economic outcome for Flector is more sensitive to regulatory and exclusivity endpoints than to long-tail patent assertions.

- Litigation risk exists but is often not the dominant driver after generics establish market presence.

(This section focuses on the business impact pattern; it requires specific Orange Book patent listings to quantify the estate by number and expiration date.)

When does Flector lose exclusivity in the US (patent expiration dates and exclusivity timelines)?

Featured snippet answer: Flector’s exclusivity and patent-based protections for the patch product have been largely exhausted in the U.S., leaving the brand exposed to ongoing generic AB competition.

Exclusivity timeline mechanics that matter

- Patent expiration: typically ends brand pricing leverage for AB-equivalent generics.

- Regulatory exclusivities: listed statutory exclusivities can add a time buffer, but once a product is mature and on-label, they rarely extend beyond the patent-driven window for older brands.

- Switch-over effects: even when a patent expires mid-year, competitive effects show up over subsequent quarters due to channel conversion and wholesaler stocking.

(Quantifying exact dates requires Orange Book data for Flector’s specific approved NDA and listed patents.)

What generic entry risks exist for Flector (Paragraph IV and FDA pathway risks)?

Featured snippet answer: The dominant generic entry risk for Flector is AB substitution through standard ANDA pathways once relevant patents and exclusivities are no longer barriers. Paragraph IV incentives exist when patent listings still block FDA approval.

How to assess generic entry risk (business lens)

- Identify whether listed Orange Book patents remain “active” at the time an ANDA is pending.

- Track whether generic filers pursue Paragraph IV certifications tied to remaining patents.

- Monitor settlements or forfeitures that can delay market entry even after formal approvals.

(Paragraph IV certification and settlement dates are not provided in the prompt; this analysis cannot enumerate them accurately without Orange Book litigation records.)

What is the Orange Book status of Flector (NDA, listed patents, and certification types)?

Featured snippet answer: Flector is an approved NDA topical diclofenac patch with Orange Book-listed patents historically supporting brand exclusivity; current market conditions indicate those protections are no longer the primary constraint versus generics.

What the Orange Book status must be mapped to for decisioning

- NDA identifier for Flector patch product

- Active listed patents and their expiration dates

- Patent term adjustment and any pediatric exclusivity impacts

- ANDA certifications:

- Updated Orange Book maintenance changes that can signal new litigation or late-breaking patent enforcement

(Exact Orange Book listing and certification mapping cannot be produced without the underlying Orange Book table entries for Flector.)

How does Flector compare with other topical diclofenac products (gel/solution vs patch economics)?

Featured snippet answer: Patch formulations face usability and adherence headwinds versus gels/solutions, while PBMs often prefer cheaper, easier-to-use topical forms for first-line coverage.

Business implications of dosage-form choice

- Coverage: plans more readily tier gel/solution into preferred categories.

- Persistence: patch wear schedules can reduce persistence if patients experience skin irritation or forget replacements.

- Total cost: patch dosing units can be costlier per treatment day versus lower-priced generic gels.

- Clinical interchange: when outcomes are broadly comparable for common musculoskeletal indications, formulary managers favor cost-effective options.

What patent litigation affects Flector (infringement suits, settlements, and brand/generic outcomes)?

Featured snippet answer: For legacy topical products like Flector, litigation historically impacts entry timing for specific generic filers, but long-run market structure typically becomes dominated by established generic supply after exclusivity barriers end.

What to track in litigation records

- Case filings tied to specific Orange Book patents

- Venue and status (dismissal, final judgment, appeal)

- Settlement terms:

- “Forbearance” windows

- Carve-outs (skin irritation label differences, manufacturing process differences)

- Agreement expiration dates

- Entry triggers:

- “nonsuit” events

- consent decrees

(Litigation outcomes and dates are not specified in the prompt; providing a table would require sourced case records.)

What FDA regulatory status applies to Flector (approval route, label scope, and safety communications)?

Featured snippet answer: Flector is an FDA-approved topical diclofenac patch with an indication set aligned to musculoskeletal pain management, and ongoing pharmacovigilance consistent with the NSAID class.

Regulatory factors that influence demand

- Indication breadth: narrower labels generally correlate with higher prescriber selectivity.

- Safety profile: NSAID class risk narratives affect patient acceptance and clinician prescribing patterns.

- Label changes can shift prescriber comfort, which changes market share distribution across topical NSAIDs.

(Specific label milestones and regulatory updates are not provided; a precise regulatory timeline cannot be constructed here.)

How do licensing deals and co-promotion dynamics affect Flector revenue?

Featured snippet answer: Licensing is usually not the primary driver for mature legacy topicals; revenue is more directly driven by PBM formulary status and generic competition once brand exclusivity lapses.

Typical deal structure impacts

- If any rights were sublicensed, the economics hinge on royalty rates and net pricing after wholesaler discounts.

- Co-promotion rarely reverses structural price erosion from generics, but can support pull-through in target prescriber segments before full AB substitution.

(No licensing deal terms are provided in the prompt, so this section cannot quantify impacts.)

What commercial metrics best explain Flector’s financial trajectory (volume, net price, channel inventory, and payer mix)?

Featured snippet answer: Revenue trends for Flector track net price compression from generic AB competition and changes in payer mix, with volume often less volatile than pricing.

Metrics to model

- Net sales:

- Net price per unit after discounts/rebates

- Unit volume:

- Patient persistence and prescriber adoption

- PBM coverage:

- Tier placement and formulary exclusions

- Channel inventory:

- Restocking cycles and sell-in volatility

- Geography:

- Differences in payer mix across commercial vs Medicare/Medicaid

(Quantitative metrics require sales data; none is supplied.)

Key takeaways

- Flector’s U.S. financial trajectory is structurally constrained by generic AB substitution within diclofenac topical products and by PBM-driven pricing compression.

- Patch-specific execution factors (adherence, skin tolerance, wear-time discipline) can reduce persistence versus gel/solution alternatives.

- Patent and exclusivity leverage has historically mattered mainly at the margin; long-run market outcomes are dominated by generic market structure once barriers end.

- Litigation and Paragraph IV challenges can influence specific entry timing for individual filers, but they rarely change the overall demand economics after generic saturation.

FAQs

- What is the most common payer policy affecting Flector patch coverage?

- Do diclofenac gel generics typically price lower than diclofenac epolamine patches per treatment day?

- How does patch adherence impact real-world persistence compared with topical gels for NSAID musculoskeletal pain?

- What are the usual triggers for PBM switching from brand topical NSAIDs to AB generics?

- Which parts of the Orange Book matter most for predicting future Flector generic entry?

References

- FDA Orange Book (Drug Products, List Search)

- FDA Prescribing Information for Flector (diclofenac epolamine) topical patch