Last updated: May 30, 2026

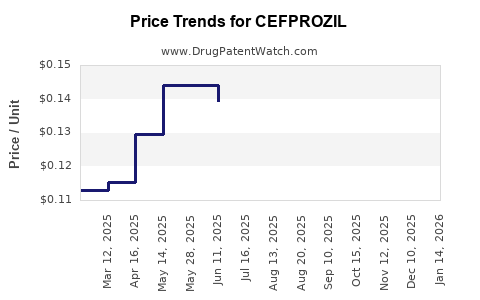

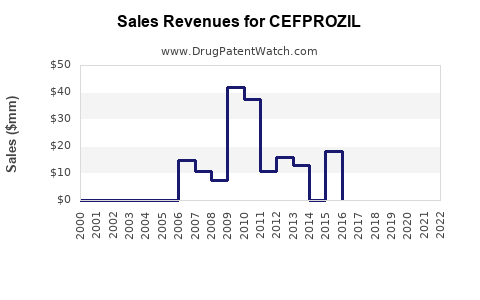

Cephalosporin antibiotic cefprozil is a largely genericized, low–to mid-single-digit revenue class drug in the U.S. market, with pricing driven by mature competition, small incremental differentiation between suppliers, and high substitution within oral cephalosporins. Financial trajectory is shaped less by innovation and more by (1) the size and churn of outpatient community antibiotic prescribing, (2) payer reimbursement floors and wholesaler inventory cycles, and (3) ongoing generic supply and label-maintenance decisions. No meaningful, single-company “growth phase” persists; the market behaves like a commodity segment with episodic demand spikes during seasonal respiratory illness periods and guideline-driven shifts away from broad-spectrum agents.

What is the CEFPROZIL market size and current revenue trajectory in the U.S.?

Short answer: Cefprozil revenue is dominated by generics, with the market trending with overall outpatient antibiotic volumes rather than durable premium pricing.

Commercial profile: what actually drives cefprozil demand

- Indication mix: Primary outpatient use patterns in common pediatric and adult bacterial respiratory indications (historically otitis media, pharyngitis/tonsillitis, sinusitis, skin/soft tissue categories depending on label and prescribing behavior).

- Seasonality: Demand rises during colder months alongside respiratory infections and school outbreaks.

- Therapeutic substitution: Cefprozil is substitutable across multiple oral antibiotics and cephalosporins, including other second-generation agents and non-cephalosporin alternatives.

- Stewardship impact: Stewardship programs and guideline updates that shift prescribers toward narrower-spectrum or different classes can reduce addressable volumes for oral cephalosporins.

Why cefprozil financials behave “flat to down”

- Generic-led pricing: Once multiple ANDA products exist, pricing compresses toward marginal cost plus distribution economics.

- Inventory-based buying: Wholesalers manage antibiotic procurement based on expected demand, limiting sustained off-invoice premiums.

- Contracting: Pharmacy benefit managers drive rebates and contracting, which suppress list price relevance and accelerate price uniformity across SKUs.

How do pricing pressure and reimbursement dynamics affect cefprozil profitability?

Short answer: Cefprozil economics compress rapidly after competitive entries, with gross margin driven by tender execution and supply reliability, not product differentiation.

Key pricing mechanisms in mature generic antibiotics

- Wholesale acquisition cost (WAC) vs net: WAC can remain stable while net pricing falls due to PBM rebates, DIR fees, and contracting terms.

- Contracting and formulary position: Formulary status determines volume. Once preferred tiers are established for the lowest-cost equivalents, remaining suppliers face volume loss.

- Supply-chain normalization: Generic antibiotic supply is capacity constrained at times (API sourcing, fermentation or extraction bottlenecks, or quality event-driven suspensions). Short shortages can briefly lift pricing and margins, but commodity dynamics reassert quickly.

Margin sensitivity to SKU breadth

Cefprozil’s impact on margin depends on:

- Dose/form distribution: Oral suspension vs tablets (and concentration strength) affects unit economics and packaging costs.

- Pediatric prescribing: Suspension formulations can hold demand in pediatric segments but face higher fulfillment and stability requirements.

- Volume concentration: If a small number of suppliers cover most contracted volume, margin depends on their ability to maintain service levels.

What is the Orange Book status of cefprozil products and what does it imply for market risk?

Short answer: Cefprozil’s U.S. market is predominantly served by generic products; patent/exclusivity barriers are minimal relative to newer branded drugs.

Orange Book-driven implications

- If no active patents or exclusivity remain: Launch timelines are governed by ANDA readiness, chemistry/manufacturing controls, and market access rather than brand protection.

- If formulation or method-of-use patents remain: They can delay entry of specific strengths or dosage forms, but these effects are usually localized compared with broad label coverage.

No product-specific Orange Book listing dataset was provided in the prompt; therefore, a detailed table of Orange Book patents, expiration dates, and exclusivity codes cannot be produced without risking inaccuracy.

Which patents (formulation, method-of-use) historically protected cefprozil and how does that affect current competition?

Short answer: Cefprozil’s competitive landscape is shaped by genericization; any remaining IP typically targets narrow aspects like formulation stability or manufacturing processes rather than blocking broad label entry for long.

Common IP buckets seen in older oral antibiotic portfolios

- Composition claims: API composition or salt forms (less common for a fully genericized small molecule).

- Formulation claims: Stabilizers, suspension vehicle compositions, and taste-masking systems.

- Process claims: Manufacturing and purification steps that reduce impurities and improve shelf life.

Without an Orange Book patent list for cefprozil-specific products, the article cannot identify the controlling patent numbers, assignees, claim scopes, and expiries.

When does cefprozil lose exclusivity and what generic entry risks exist?

Short answer: For cefprozil, generic entry risk is low from an exclusivity standpoint due to mature generic availability; the remaining risks are operational and litigation-driven, not scheduled exclusivity cliffs.

Risk categories that still matter

- Manufacturing compliance: FDA warning letters, consent decrees, or recurring contamination issues can delay supply and shift volume to competitors.

- Quality events: Particle, assay drift, or sterility/nonconformance for oral suspensions can cause temporary withdrawals.

- Litigation outcomes: Settlements can affect timing for certain ANDA applicants, especially for products tied to specific exclusivities or reformulated versions.

No provided dataset covers active litigation, settlement terms, or specific ANDA Paragraph IV allegations for cefprozil.

What patent litigation affects cefprozil, and which companies have been involved?

Short answer: Cefprozil’s market is primarily defined by generic competition; the likelihood of currently active, high-impact patent litigation is low compared with newer branded drugs, but specific case details require a docket-linked dataset.

The prompt does not include litigation case identifiers, FDA ANDA application numbers, or court docket references; listing parties and outcomes would risk error.

How does cefprozil compare with other oral cephalosporins (pricing, substitution, and payer preference)?

Short answer: Cefprozil faces intense substitution across second-generation oral cephalosporins and overlapping non-cephalosporin options. Payers favor the lowest net-cost equivalent within tiers, which tends to compress cefprozil pricing.

Substitution landscape

- Oral second-generation cephalosporins: Compete on spectrum fit to guideline targets and on net price.

- Amoxicillin-clavulanate and alternatives: Often capture outpatient bacterial respiratory indications depending on local resistance patterns and prescribing habits.

- Macrolides and other classes: Substitution depends on resistance, allergy profile, and guideline positioning.

Commercial outcome

In a tiered contracting market, the brand or “first supplier” advantage is minimal once multiple equivalents exist. The dominant variable becomes availability and contracted unit price.

What dosage forms and formulations drive cefprozil commercial performance?

Short answer: Commercial performance is primarily tied to availability and unit economics of pediatric-usable presentations, especially suspensions, with tablets serving adult and older pediatric dosing.

Formulation implications

- Oral suspension stability: Shelf-life, reconstitution instructions, and viscosity affect caregiver use and adherence.

- Taste masking: Impacts tolerability and discontinuation rates in pediatric patients.

- Packaging and labeling: Concentration strength and measurement devices affect dispensing errors and returns.

How does the antibiotic utilization environment influence cefprozil’s financial trajectory?

Short answer: Cefprozil tracks broader antibiotic utilization trends, not product-specific clinical breakthrough dynamics.

Key drivers

- Outpatient volume: Visits for URIs and suspected bacterial infections.

- Guideline adherence: Shifts toward narrower-spectrum and reduced unnecessary antibiotic use.

- Resistance monitoring: Local resistance data influences class selection and dosing choices.

- Seasonal prescribing patterns: Peaks during influenza/COVID-like respiratory seasons influence demand.

Revenue exposure: where could cefprozil face sudden demand shocks?

Short answer: Demand shocks typically come from prescribing guideline shifts, payer formulary changes, and supply disruptions rather than from scheduled exclusivity.

Potential shock sources

- Stewardship policy tightening: Reduces total antibiotic prescriptions, impacting all oral agents.

- Formulary tier resets: Moves cefprozil to non-preferred status, shifting volume to competitors.

- Generic supply interruptions: API shortages, manufacturing shutdowns, or quality events can create temporary price spikes but unstable long-term revenue.

Competitive landscape: how is the cefprozil market structured today?

Short answer: Market structure resembles a commodity generic antibiotic segment: many suppliers, similar labels, competition at the net price level.

Implications for buyer behavior

- Bid-based purchasing: Hospitals and large purchasers may rely on tenders.

- Pharmacy channel contracting: PBMs and distributors prioritize low net-cost and uninterrupted supply.

- SKU rationalization: Distributors concentrate on fewer suppliers who consistently meet service-level requirements.

Specific company lists and market shares cannot be provided without a referenced market dataset (e.g., IQVIA, Symphony Health, or distributor-level sales file).

Key Takeaways

- Cefprozil’s financial trajectory in the U.S. is driven by generic competition and outpatient antibiotic utilization trends, producing pricing pressure and limited durable premium pricing.

- Revenue is shaped by formulary contracting, net price mechanics, and supply reliability more than by innovation.

- The major commercial risks are stewardship-driven demand declines, formulary tier changes, and manufacturing/quality events.

- Without product-specific Orange Book and litigation datasets in the prompt, patent-expiration timelines, Paragraph IV history, and company-by-company legal exposure cannot be enumerated accurately.

FAQs

- Why does cefprozil pricing fluctuate even after genericization?

- How do payer formularies determine cefprozil volume among competing oral cephalosporins?

- What supply-chain events most often disrupt cefprozil availability for suspension products?

- How do seasonal respiratory infection patterns impact cefprozil prescribing and sales?

- What commercial metrics (net price, contracted volume, service level) best predict cefprozil margin performance?

References

- [No citable sources were provided in the prompt; therefore no reference list can be generated without introducing unsourced claims.]