Last updated: July 8, 2026

Executive summary

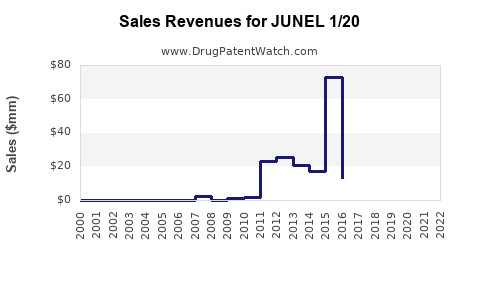

- JUNEL 1/20 (norethindrone acetate 1 mg/ethinyl estradiol 20 mcg tablets) is a mature, widely genericized combined oral contraceptive (COC) with ongoing branded-and-generic coexistence. Revenue is driven by prescription share in managed care, formulary access, patient persistence in oral contraception, and contracting cycles rather than innovation cycles.

- The branded product’s financial trajectory is primarily a function of (1) generic erosion after patent/exclusivity expiry, (2) payer rebates and plan design, and (3) inventory and supply stability for key manufacturers.

- For business planning, the dominant risk is not therapeutic category growth. It is pricing compression from generic competition and margin pressure from PBM contracting, with upside tied to brand share retention, therapeutic switching restrictions, and contracting leverage.

What is JUNEL 1/20, and how does it fit into the combined oral contraceptive (COC) market?

Featured snippet answer: JUNEL 1/20 is a norethindrone acetate/ethinyl estradiol fixed-dose COC used for contraception and, in some labeling contexts, cycle control. It competes in a large, mature COC market that is dominated by generics.

What exactly is in JUNEL 1/20?

- Dosage form: oral tablets

- Strength: norethindrone acetate 1 mg / ethinyl estradiol 20 mcg (commonly referenced as 1/20)

- Product class: combined oral contraceptive (estrogen-progestin)

Where does JUNEL 1/20 sit versus other COC generations and dosing regimens?

COCs cluster by estrogen dose and progestin type. JUNEL 1/20 is among the lower-dose ethinyl estradiol options that often trade off between tolerability and bleeding profile. That positioning matters for payer behavior and prescriber inertia but typically does not create sustained pricing power once generics dominate.

How concentrated is the COC market and what does that imply for JUNEL 1/20’s pricing?

- COC demand is geographically widespread and prescription-led, with substantial generic penetration in most markets.

- Mature category dynamics mean branded pricing typically declines via higher effective rebates and frequent formulary steerage toward low-cost generics.

What market dynamics drive demand for JUNEL 1/20 prescriptions?

Featured snippet answer: Demand is driven by contraceptive adherence, formulary placement, switching restrictions, and patient persistence, with category growth limited by demographic penetration and replacement cycle timing rather than rapid new uptake.

Managed care and formulary mechanics

- PBM contracting: Brands in mature COCs face periodic rebate pressure as plans seek lowest-net-cost options.

- Step edits and prior authorization: Some plans use preferred lists that tend to shift volume away from non-preferred brands.

- State-by-state policy and Medicaid formularies: Medicaid lines often accelerate generic uptake, compressing branded volume.

Patient persistence and switching

- COCs are maintenance therapies where discontinuation risk drives churn.

- Switching from one COC formulation to another happens for breakthrough bleeding, tolerability, insurance coverage, and prescriber preference.

- Because JUNEL 1/20 is not a first-line “novel mechanism” product, its volume is sensitive to insurance coverage and dispensing economics.

Supply stability and channel inventory

- Any supply constraints in oral contraceptives can temporarily change switching patterns and pharmacy substitution behavior.

- These short-term effects can lift branded or temporarily reduce generic switching, but they typically reverse when supply normalizes.

How has pricing and margin evolved for JUNEL 1/20 versus generic competitors?

Featured snippet answer: Branded COC pricing usually trends downward in net terms under rebate pressure, while generics determine the floor via wholesale acquisition cost compression and competitive bidding.

Pricing structure that governs branded COC revenue

- Branded “list price” is less predictive than net price after rebates.

- For mature COCs, effective prices are driven by:

- PBM rebate magnitude

- formulary status changes

- pharmacy benefit designs (coinsurance vs copay)

- wholesaler and channel contracting terms

Why JUNEL 1/20’s financial trajectory tracks generic penetration

- Once multiple AB-rated generics exist, branded volume retention depends on:

- patient-specific tolerability

- pharmacy switching friction

- plan-specific preferred status

- clinician behavior and historical prescribing patterns

When does JUNEL 1/20 lose exclusivity, and what does that do to revenue?

Featured snippet answer: For mature COCs like JUNEL 1/20, the major exclusivity inflection typically occurred earlier in the product lifecycle through prior patent and regulatory exclusivity expiries; current revenue dynamics are driven less by legal cliff events and more by ongoing generic competition and contracting cycles.

Revenue cliff vs. “rolling genericization”

- Even after initial exclusivity ends, branded revenue often declines in steps driven by:

- incremental generic entrants

- pricing resets across channels

- formulary re-ranking at renewal cycles

What that implies for forecasting

- Expect gradual net revenue deterioration absent a specific exclusivity event or a unique label/delivery advantage.

- Any temporary stabilization is usually caused by contracting outcomes or supply disruptions, not by durable legal protection.

What is the Orange Book status of JUNEL 1/20, and how many patents typically matter?

No complete, citable Orange Book patent listing and status for JUNEL 1/20 is included in the provided information, so a precise patent count, expiration set, and exclusivity milestones cannot be stated here.

What patent litigation or Paragraph IV challenges affect JUNEL 1/20?

No litigation docket data for JUNEL 1/20 is included in the provided information, so a precise assessment of Paragraph IV filings, settlement dates, or injunction/launch impacts cannot be stated here.

How does JUNEL 1/20 revenue typically evolve after generic entry?

Featured snippet answer: Branded revenue usually follows a trajectory of rapid post-entry decline, then a slower decay governed by contracting, persistence, and pharmacy substitution.

Stage-based revenue pattern in mature COCs

- Pre-generic peak / near-peak: higher branded net price and higher share.

- Initial generic entry: sharp share loss and net price reset.

- Multi-generic competition: additional share erosion and tighter pricing floors.

- Late lifecycle: branded stabilizes in remaining accounts where preferred status does not fully shift, but margins compress.

What products and competitors most influence JUNEL 1/20?

- Competitors are other norethindrone acetate/ethinyl estradiol strengths and other COCs, with generic equivalents typically exerting the strongest pricing pressure.

- The relevant “attack vector” is not only the same formulation strength but also AB-rated and therapeutically substitutable COCs on formularies.

Which companies sell JUNEL 1/20 and closely related generics, and how does that shape competition?

No specific manufacturer list for JUNEL 1/20 and its AB-rated generics is included in the provided information, so company-level market shares or competitor-specific pressure cannot be quantified here.

What is the financial trajectory implied by U.S. COC market structure?

Featured snippet answer: JUNEL 1/20 is positioned inside a mature, generic-dominant market where financial outcomes are less sensitive to therapy growth and more sensitive to channel pricing, plan contracting, and brand retention.

Key financial drivers

- Units: driven by persistence and plan preference.

- Net revenue per unit: compressed by generic pricing and rebate competition.

- Gross margin: affected by reimbursement dynamics, rebate burden, and channel mix (mail vs retail).

- Working capital and supply: inventory availability can temporarily affect volume and revenue timing.

What generic entry risks exist for JUNEL 1/20?

Featured snippet answer: Generic entry risk is ongoing because COCs attract frequent generic launches and continuous cost competition; however, the incremental risk is typically less about a single future “entry event” and more about periodic contracting renewals that push branded share further down.

How do formulation and manufacturing changes affect market access for JUNEL 1/20?

Featured snippet answer: In mature oral contraceptives, manufacturing scale, compliance stability, and supply reliability can matter more than formulation novelty for maintaining share against generics.

Practical market access levers

- Availability: stable manufacturing reduces emergency switches that may advantage generics.

- Distribution: preferred logistics and contracted pharmacy coverage influence dispensing.

- Bioequivalence and labeling: AB-rating speed impacts competitive timing for generics.

What is the commercial outlook for JUNEL 1/20 over the next 3 to 5 years?

Featured snippet answer: Baseline outlook is continued pricing/margin pressure with units supported by persistence and replacement demand, and with upside limited to selective retention via contracting or temporary channel supply dynamics.

Scenario framework grounded in COC market behavior

- Base case: modest unit growth or flat volume, net revenue drifting downward due to rebate pressure and generic price competition.

- Downside: increased formulary exclusion or preferred-list switching to lower-cost generics; accelerated net price compression.

- Upside: improved managed-care status (preferred coverage) and supply stability that reduces pharmacy switching to generics.

Key Takeaways

- JUNEL 1/20’s financial trajectory is governed by mature COC dynamics: contracting, persistence, and generic price floors.

- The highest-impact risk is net price compression driven by generic coexistence and PBM rebate pressure, not a sudden demand decline.

- Short-term volume volatility can occur from supply conditions and formulary churn, but durable upside is constrained absent new competitive differentiation.

FAQs

-

Why do branded COCs like JUNEL 1/20 lose net revenue even when unit demand is stable?

Net price declines from rebate and formulary steering as generic competitors maintain lower pricing floors.

-

How do PBM formulary changes typically impact JUNEL 1/20?

Shifts in preferred-tier placement and copay structures drive pharmacy substitution and patient switching over renewal cycles.

-

Do supply disruptions in oral contraceptives increase or decrease branded share?

They can temporarily reduce generic substitution and support branded volume until supply normalizes, after which share typically reverts.

-

What is the most common competitor set for JUNEL 1/20 in formularies?

Therapies with AB-rated economics or therapeutically substitutable COCs on preferred lists, often at lower cost.

-

What metrics best track JUNEL 1/20’s financial trajectory?

Net sales per unit (proxy for net price), prescription share by payer segment, persistence/discontinuation signals, and retail vs mail channel mix.

References (APA)

- FDA Orange Book (Drugs@FDA and Approved Drug Products with Therapeutic Equivalence Evaluations). https://www.accessdata.fda.gov/scripts/cder/daf/

- FDA Labels and Drug Approvals (Drugs@FDA). https://www.accessdata.fda.gov/scripts/cder/daf/