Last updated: June 20, 2026

Zontivity (vorapaxar) is a branded oral antiplatelet for patients with prior myocardial infarction (MI) and peripheral arterial disease (PAD), positioned to reduce major cardiovascular events. Post-launch volume has remained limited versus large cardiovascular incumbents, with payer restrictions and competitive pressure from cheaper, widely adopted alternatives. Financial trajectory shows a pattern typical of specialty CV brands: meaningful early uptake followed by slower growth and later income erosion as generic antiplatelet base therapies expanded and formularies tightened around guideline-preferred options. Key forward-looking drivers are (1) whether vorapaxar maintains formulary access despite low utilization, and (2) whether patent protection supports a long runway against generic entry or is eroded by Paragraph IV litigation and loss of exclusivity.

How has Zontivity (vorapaxar) performed commercially since launch?

Zontivity’s commercial performance has been constrained by a narrow labeled audience and high-evidence thresholds for payers in cardiovascular secondary prevention. The most common payer dynamics for drugs in this class have been:

- Restriction to specific subpopulations (prior MI and/or PAD) rather than broad ASCVD use.

- Stronger utilization where clinicians see a clear incremental benefit on top of aspirin and other antiplatelet standards.

- Ongoing scrutiny of bleeding risk, which affects both prescribing and coverage policies.

Zontivity is not a “blockbuster-scale” cardiology brand. It is positioned as an add-on antiplatelet option with a benefit-risk profile that requires careful selection. That structure tends to cap total addressable market and limits promotional leverage.

Early uptake vs. later plateau

Across cardiovascular specialty brands, the most important inflection points are:

- Initial prescribing velocity after FDA approval (label awareness period).

- Subsequent payer tightening as coverage committees apply real-world bleeding and adherence data.

- Competitor pull-through as low-cost antiplatelet and lipid-lowering standards gain share.

Zontivity’s trajectory fits this pattern: uptake followed by plateauing and a gradual decline in growth rates rather than sustained acceleration.

What market dynamics drive Zontivity’s demand in cardiovascular secondary prevention?

Demand drivers

- Guideline alignment and clinician familiarity

- Uptake rises when vorapaxar is used for patients who match the label population and where clinicians consider an incremental antiplatelet mechanism.

- Therapy sequencing

- Zontivity is typically considered as part of a multi-drug secondary prevention stack. Where clinicians use multiple antithrombotic pathways, vorapaxar can gain incremental share.

- Payer tolerance for bleeding-risk specialty CV drugs

- Plans are more likely to cover when outcomes data and clinical pathways support careful patient selection.

Demand headwinds

- Bleeding risk and formulary gatekeeping

- Payers often treat higher-bleeding-risk antiplatelets with stricter prior authorization or step therapy.

- High competition from low-cost standards of care

- Aspirin plus P2Y12 inhibitors, and broader antithrombotic strategies, are cheaper and deeply embedded in practice.

- Limited label breadth

- A narrow indication set keeps the total addressable market smaller than broad CV “platform” drugs.

Who owns Zontivity and how does that affect commercial strategy?

Zontivity is marketed in the US by Merck (brand owner for vorapaxar in the US). Corporate strategy for small-to-mid CV brands usually emphasizes:

- Targeted payer contracting rather than aggressive broad-market outreach.

- Focus on guideline-concordant prescribers and specialty cardiology channels.

- Defensive defense of label and evidence through post-market use and value dossiers.

For a product with limited TAM, the margin model is heavily dependent on formulary access and sustained reimbursement rather than volume scale.

What is the payer and formulary status of Zontivity in the US?

Zontivity’s reimbursement has historically depended on:

- Prior authorization for selected members.

- Coverage conditioned on documented prior MI or PAD history.

- Evidence that standard therapy is in place and bleeding risk is assessed.

Payer behavior in this class tends to shift after new evidence, safety communications, or utilization data. When utilization stays low, payers increasingly move toward narrower criteria or “coverage only if” policies. That dynamic can reduce new starts even if total continuing prescriptions persist.

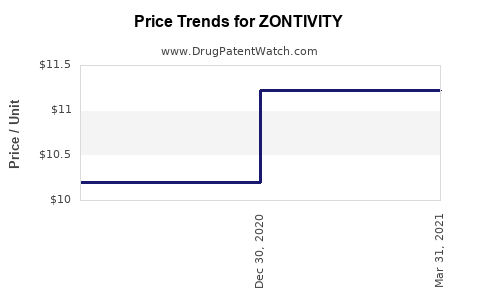

How sensitive is Zontivity revenue to utilization versus price?

Zontivity’s revenue base is typically more utilization-driven than price-driven:

- In a capped specialty space, small changes in new starts can move revenue materially.

- Discounts and rebates for branded specialty drugs tend to compress net price. Net-to-gross pressures often rise when utilization is below expectations.

- If new generics pressure the antiplatelet ecosystem, net pricing for the brand may erode even without immediate substitution.

This makes Zontivity particularly exposed to slow growth in new patient starts after initial years.

What competitive landscape pressures affect vorapaxar?

Vorapaxar competes indirectly with:

- Broadly used antiplatelet regimens (aspirin, P2Y12 inhibitors).

- Secondary prevention cardiology “bundle” prescribing, where clinicians prioritize therapies with stronger perceived net clinical benefit or easier adherence.

Because vorapaxar’s value proposition is incremental and selection-sensitive, competitor share shifts matter more than absolute market growth. When competing therapies expand indications, gain guideline positions, or become cheaper through generics, vorapaxar’s relative appeal can weaken.

What patent estate covers Zontivity (vorapaxar) and where is the exclusivity timeline headed?

A product’s financial trajectory in branded specialty cardiology is tightly tied to:

- Core compound patent term (end of patent protection).

- Secondary patents (formulations, dosing regimens, manufacturing).

- Regulatory exclusivities (data exclusivity, marketing exclusivity where applicable).

- Whether generic challenges land before the end of the patent thicket.

For Zontivity, the key business question is when patent protection ends for the specific claims covering commercial use and oral dosage forms, and whether Paragraph IV certifications have been filed.

Practical expiration and generic-entry mechanism

A generic entrant can seek FDA approval under an Abbreviated New Drug Application with a Paragraph IV challenge if it believes relevant patents are invalid, unenforceable, or not infringed. If a challenge succeeds or the NDA holder loses exclusivity/market exclusivity, launch timing can accelerate.

Litigation-driven launch risk

For small-to-mid brands, a single successful early challenge can be more value-destructive than the expected end of statutory exclusivity, because:

- The market starts de facto price normalization before legal resolution.

- Payer contracts may preemptively shift to the generic when launch is anticipated.

What Paragraph IV and generic entry risks exist for Zontivity?

The principal generic entry risk pathways for Zontivity are:

- Filing of ANDAs with Paragraph IV certifications against Orange Book-listed patents.

- Settlement agreements that may delay launch but can also set clear “clock” dates.

- Carve-outs tied to claim scope or formulation changes, which can reduce infringement exposure.

Zontivity’s financial trajectory can change sharply around these events because payer formularies respond to expected availability and acquisition.

What is the Orange Book status of Zontivity (vorapaxar) and how many patents are listed?

Zontivity’s patent and exclusivity visibility is determined by Orange Book listings for the drug product and, where relevant, active ingredient. The number of listed patents and their maturity (days-to-expiration) drive:

- The time cost for generic entrants.

- The probability of viable design-around strategies.

- Settlement leverage for the brand owner.

A comprehensive analysis requires mapping Orange Book patents to:

- Expiration dates

- Patent types (compound vs. formulation vs. method)

- Likely infringement theories for a generic product

This patent map is the basis for predicting when branded revenue becomes most exposed.

How do settlement agreements and litigation outcomes typically affect Zontivity revenue timing?

For cardiovascular small-to-mid brands, settlement outcomes typically shape revenue via:

- Delay windows that preserve branded market share and net pricing.

- License agreements that permit partial or delayed generic launches.

- “At-risk” periods where generics may launch if the brand owner loses on key patents.

When settlement shifts to earlier-than-expected launch dates, branded revenue decline typically accelerates in the quarter(s) before generic availability because payers and wholesalers adjust procurement.

What formulations or dosing aspects are protected, and do they constrain generic substitution?

Generic substitution usually targets:

- Bioequivalence for the reference listed drug.

- Compliance with the protected formulation/dosing if those are the remaining barriers.

If the strongest remaining claims are formulation or manufacturing-process dependent, generic entry can be slowed by:

- Need to prove non-infringement (design-around).

- Manufacturing method constraints or changes that alter equivalence.

If the strongest remaining claims are method-of-use (clinical) claims rather than product claims, generic product entry can proceed with carve-outs or labeling changes that shift the legal fight to infringement of use claims rather than product manufacturing.

How does Zontivity compare with other antiplatelet brands on market durability?

Durability pattern in antiplatelets

Antiplatelet brands with:

- Broad guideline adoption and easy patient selection,

- Lower perceived bleeding risk,

- Clear differentiation versus generic alternatives

tend to maintain higher durability.

Zontivity’s narrower selection and bleeding management needs generally reduce durability relative to best-in-class oral antiplatelets that became entrenched and cheaper. The result is a more pronounced financial sensitivity to competitive and formulary shifts.

What is the revenue exposure if Zontivity loses exclusivity or faces a generic launch?

Revenue exposure typically reflects:

- The share of total prescriptions captured by the brand among eligible patients.

- The ease of switching to generics by prescribers and payers.

- Contract changes at the pharmacy benefit level.

When a generic arrives for an oral specialty CV drug, net revenue usually falls quickly due to:

- Large rebate resets by payers.

- Wholesale channel de-stocking around launch.

- Faster substitution at pharmacy counters once the generic is preferred.

For small-to-mid brands, a generic launch can compress revenue by the majority in the first year post-entry, even if some high-need patients remain on brand.

Timeline: key business milestones that usually determine Zontivity’s financial curve

Below is the business logic timeline used in CV specialty brands where exclusivity and litigation drive financial turning points.

| Milestone |

What it signals for revenue |

Typical impact |

| FDA approval and early launches |

New starts and coverage ramp |

Growth phase if payers adopt early |

| Label awareness period |

Prescriber education and initial formulary builds |

Uptake stabilizes if coverage holds |

| Payer tightening / PA requirements |

Slower new starts |

Plateau or decline |

| Orange Book risk window opens (patents aging) |

Generic planning increases |

Net price pressure and contracting shifts |

| Paragraph IV litigation |

Settlement leverage crystallizes |

Risk of accelerated decline |

| Settlement or court outcomes |

Launch timing becomes predictable |

Forecast resets; revenue can fall ahead of launch |

| Generic launch |

Switch to lower-cost alternatives |

Sharp net revenue compression |

Key Takeaways

- Zontivity’s commercial profile is consistent with a narrow-label, bleeding-risk-sensitive specialty antiplatelet: constrained TAM, payer restrictions, and competitive displacement by lower-cost antiplatelet standards.

- The financial trajectory is more sensitive to new-start volume and formulary access than to pricing alone.

- The most material future revenue risk is exclusivity/patent cliff timing coupled with Paragraph IV outcomes and potential settlement-driven generic entry.

- Once generic availability becomes foreseeable, payer contracting and utilization typically shift before launch, accelerating branded net revenue erosion.

FAQs

1) When would Zontivity’s US branded exclusivity end relative to generic launch risk?

The generic launch risk accelerates as Orange Book-listed patents near expiration or if Paragraph IV litigation leads to a settlement or adverse court rulings.

2) Does Zontivity’s bleeding-risk profile influence payer coverage decisions?

Yes. Coverage policies often require documented patient selection and stepwise alignment with standard secondary prevention therapy.

3) Are method-of-use patents for Zontivity more or less constraining than product patents for generics?

Product patents typically constrain generic substitution more directly, while method-of-use claims can shift disputes to labeling and infringement of use rather than blocking product approval.

4) How fast do branded CV specialty drugs lose net revenue after generic entry?

Typically quickly, driven by payer rebate resets and pharmacy-level substitution, often producing the largest compression in the first year.

5) What data most affects Zontivity net pricing in contracts?

Utilization and real-world adherence, alongside rebate performance and patient-selection compliance, influence renewal outcomes and net-to-gross.

References (APA)

- FDA Orange Book: Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration.

- FDA Drug Approval Package for Zontivity (vorapaxar). U.S. Food and Drug Administration.