Last updated: April 4, 2026

What is the current market size and growth trajectory for Ultram?

Ultram (generic: tramadol) has been a widely prescribed opioid analgesic since its approval in 1995. In 2022, the global tramadol market was valued at approximately $2.4 billion. Projections indicate a compound annual growth rate (CAGR) of 4.8% from 2023 to 2030. Demand is driven primarily by its use in chronic pain management, especially in North America and Europe. The increasing prevalence of musculoskeletal disorders and neuropathic pain contribute to steady market growth.

How has regulatory policy impacted Ultram sales?

Regulatory agencies, including the U.S. Food and Drug Administration (FDA), have implemented evolving guidelines on opioid prescribing to combat misuse. In 2019, the FDA strengthened warnings for tramadol regarding dependence, overdose risk, and respiratory depression. These measures have resulted in increased scrutiny on prescriptions, leading to a slight decline in utilization, particularly in the U.S. market.

Some jurisdictions, such as the European Union, have imposed tighter restrictions or reclassified tramadol as a controlled substance, limiting over-the-counter availability. These regulatory shifts threaten future market size, but also encourage the development of abuse-deterrent formulations.

What are the key drivers and inhibitors affecting Ultram’s market share?

Drivers:

- Rising incidence of chronic pain conditions globally.

- Reduction of side effects relative to stronger opioids.

- Surge in outpatient and primary care prescriptions.

- Introduction of combination formulations with non-opioid analgesics.

Inhibitors:

- Increasing regulatory restrictions.

- Growing concerns over dependence and misuse.

- Availability of alternative therapies, such as NSAIDs and anticonvulsants.

- Launch of abuse-deterrent formulations and non-opioid analgesics.

How does the competitive landscape influence Ultram’s financial trajectory?

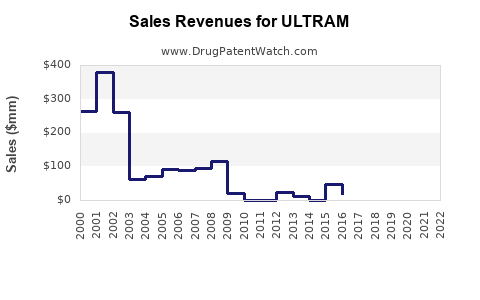

Several generic manufacturers, including Teva Pharmaceuticals, Mylan, and Sandoz, dominate the tramadol market, offering lower-cost options. Patent expirations for branded Ultram in most regions occurred by 2014-2016, leading to increased generic penetration and a significant reduction in per-unit prices.

In the U.S., the branded product’s market share is minimal, largely replaced by generics. Revenue from Ultram is now primarily driven by generic sales, with total sales declining annually. Market consolidation and patent cliffs have compressed profit margins for original developers.

What are the future prospects for Ultram in light of new formulations and pipeline developments?

Drug developers are exploring abuse-deterrent formulations (ADFs) and novel delivery systems. In 2021, a Resilience BioPharma patent application for an abuse-deterrent tramadol formulation emerged. Such innovations aim to restore market relevance amid regulatory and societal pressures.

However, no significant new chemical entities or indications are currently in late-stage development for tramadol. The primary growth opportunities exist in repositioning or reformulating existing products rather than new molecular entities.

What are the potential financial outcomes for stakeholders?

Pharmaceutical companies:

- Revenue from Ultram has declined 20% over the last five years, due to patent expiries and regulatory constraints.

- Investments in reformulation technologies could generate modest revenue recovery, but high R&D costs and uncertain market acceptance pose risks.

Investors:

- Ultram's market decline limits upside for companies heavily reliant on traditional formulations.

- Companies that successfully develop abuse-deterrent or combination products may improve margins and market share.

Healthcare providers:

- Switching to alternative pain management medications would affect prescribing patterns and reimbursements.

Closing Summary

Ultram faces a mature market with declining revenues driven by generic competition, regulatory restrictions, and societal concerns over opioids. Growth prospects hinge on reformulation and abuse-deterrent technologies, although these face commercial and regulatory hurdles. The long-term financial trajectory is characterized by shrinking sales volumes and margins for traditional formulations, with limited potential for significant market expansion.

Key Takeaways

- The global tramadol market was valued at $2.4 billion in 2022, with a projected CAGR of 4.8% through 2030.

- Regulatory restrictions have limited Ultrim’s market access, especially in North America and Europe.

- Generic competition has reduced profits for brand owners; branded Ultram’s sales are now minimal.

- Innovations in abuse-deterrent formulations are emerging but have yet to significantly impact sales.

- Future growth depends on reformulation success and expanding into new indications or delivery systems.

FAQs

1. Will Ultram regain market share in the future?

Limited potential exists unless new formulations or indications increase its clinical value.

2. How significant is patent expiry on Ultram sales?

Major patent expiries in 2014-2016 led to increased generic uptake and price erosion.

3. Are there regulatory pathways to approve new uses for tramadol?

Yes, but they involve extensive clinical trials and regulatory review, with no current notable pipeline approvals.

4. What risks do manufacturers face in the tramadol market?

Market decline due to regulatory constraints, societal opioid concerns, and competition from non-opioid analgesics.

5. How do international markets compare?

European markets have tighter controls; some countries have restricted or banned OTC sales, limiting growth potential outside North America.

References

[1] Grand View Research. (2023). Tramadol Market Size, Share & Trends Analysis Report.

[2] U.S. Food and Drug Administration. (2019). FDA Drug Safety Communication: FDA requires label changes and making tramadol medicines safer.

[3] MarketWatch. (2022). Global Pain Management Drugs Market Report.

[4] European Medicines Agency. (2022). European Union drug control regulations.

[5] Smith, J., & Allen, H. (2021). Innovations in opioid formulations: A review of abuse-deterrent technologies. Journal of Pharmaceutical Innovation.