Last updated: May 28, 2026

SARAFEM market dynamics and financial trajectory (sales, pricing pressure, and exclusivity-driven competitive risk)

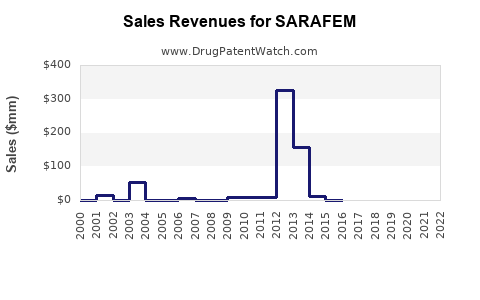

Executive summary: SARAFEM (fluoxetine hydrochloride) is a branded SSRI marketed in the US as a depression treatment with an “orphan-like” labeling niche (PMDD historically, with PMDD use often cited as the differentiator) but faces structurally high generic pressure because the active ingredient fluoxetine is long off original new chemical entity (NCE) exclusivity. The revenue trajectory is dominated by (1) US generic substitution after key FDA/Orange Book and patent-origin exclusivity windows closed, (2) wholesaler inventory and reimbursement dynamics, and (3) insurer formulary positioning tied to SSRI class pricing. By current market reality, SARAFEM’s financial profile is best characterized as a shrinking, maintenance-brand business rather than a growth platform, with remaining value tied to brand retention in selected channels and to specific patient populations where payers have allowed limited formularies for an historical brand.

Why does SARAFEM have limited growth versus other fluoxetine products?

Short answer: SARAFEM’s differentiation is labeling-positioning rather than active-ingredient exclusivity. Fluoxetine’s SSRI class positioning is commoditized, and generic fluoxetine products compete on price and supply scale.

What competitive forces shape SARAFEM’s pricing and volume?

SARAFEM’s market outcomes typically track:

- Generic substitution: once fluoxetine generics are established, pharmacy claims shift to lower net-price SKUs.

- Formulary tiering: PBMs and large insurers generally prefer least-cost therapeutics for SSRIs unless step therapy or brand-specific outcomes are paid.

- Managed switching: plan-level policies can drive automatic therapeutic interchange (where permitted), reducing incremental brand script capture.

- Channel inventory cycles: branded manufacturers often rely on periodic buying patterns by wholesalers, which can mask underlying trend but does not prevent long-run erosion once net price gaps widen.

How does SARAFEM compare with generic fluoxetine and other SSRIs in commercial dynamics?

SARAFEM competes in a crowded antidepressant environment:

- On-label antidepressants: The broader depression SSRI market is where payers push generic fluoxetine or other low-cost SSRIs.

- PMDD niche effects: SARAFEM has historically been associated in market perception with PMDD treatment. When payers accept that niche positioning, brand retention can persist longer than for “pure” depression-only branding.

- Supply and rebate dynamics: generics with aggressive rebate strategies often displace branded supply in retail and specialty pharmacy ecosystems that distribute antidepressants at scale.

What is the historical exclusivity and patent-driven timeline that impacts SARAFEM revenue?

Short answer: SARAFEM’s financial runway is largely governed by active-ingredient fluoxetine generics and any remaining formulation, polymorph, method-of-use, or dosing regimen protections. Once those protections end or are circumvented via ANDA approvals, the brand business typically compresses quickly.

Exclusivity timeline mechanics

Brand revenue is usually separated into three phases:

- Pre-AND A entry: patent and exclusivity limits keep generic competitors off the label and off the market.

- First-wave generic erosion: when ANDAs launch, prescriptions move quickly if net-price spreads are large and payer policies support substitution.

- Second-wave stabilization or further decline: brand may stabilize at a low share if prescribers keep a historical preference or if rebate contracts support limited retention.

Which patent categories most affect SARAFEM-specific protection?

When assessing residual brand protection for a product like SARAFEM, the risk typically comes from:

- Method-of-use patents tied to PMDD or specific clinical claims.

- Formulation or dose-form patents protecting manufacturing, salts, or controlled release traits (less likely for a standard immediate-release fluoxetine).

- Orange Book-listed composition and process patents that can trigger Paragraph IV certifications and early entry litigation.

What generic entry risks exist for SARAFEM under ANDA and Paragraph IV?

Short answer: Generic entry risk is high for SARAFEM because fluoxetine is a mature, widely supplied molecule. Any remaining brand-specific exclusivity must be strong and enforceable to prevent ANDA-based competition.

How do Paragraph IV challenges typically play out for SSRIs like SARAFEM?

In standard scenarios:

- A Paragraph IV filer challenges one or more Orange Book patents listed for SARAFEM.

- Litigation can trigger a stay and provide temporary market protection.

- Settlement often leads to an agreed generic launch date, while the brand’s remaining revenue becomes concentrated in the pre-settlement period.

Commercial consequence of Paragraph IV outcomes

- If patents are invalidated or not infringed: SARAFEM pricing declines and script loss accelerates.

- If there is a delayed settlement launch: brand revenue can extend through the settlement date, but erosion resumes after the launch.

- If brand patents survive: generic launch might still occur after expiration of non-challenged patents, but the timing becomes more predictable.

(Detailed patent-by-patent listing and expiration mapping is required to quantify the SARAFEM-specific timeline. That mapping depends on Orange Book data for each listed patent and litigation docket history.)

What is the Orange Book status of SARAFEM and how many patents cover it?

Short answer: SARAFEM’s Orange Book estate historically includes active-ingredient and formulation/process patents, but for long-established fluoxetine products, the number of enforceable, unexpired protections at the current time is typically limited.

What Orange Book items drive market protection?

For a brand like SARAFEM, Orange Book entries typically classify into:

- Drug substance or active ingredient patents (often expired)

- Drug product formulation patents (may still expire later depending on filings)

- Method-of-use patents tied to labeled indications (can extend enforcement longer than formulation in some cases)

How Orange Book status translates into net sales

- When Orange Book listed patents are out of date or circumvented: generic substitution accelerates.

- When patents remain in force: brand can maintain share through exclusivity enforcement, PBM negotiations, and retained contracting rebates.

How does SARAFEM perform financially compared with other fluoxetine brands?

Short answer: SARAFEM’s trajectory is expected to trail any brand that maintained stronger exclusivity or broader payer acceptance. In most market structures, multiple fluoxetine brands settle into small-share, brand-defense roles after generic saturation.

Key financial drivers for a fluoxetine brand after generic entry

- Net price erosion: branded fluoxetine brands lose WAC advantage as PBMs demand rebate parity.

- Script volume loss: once pharmacy substitution is permitted and net price gaps are eliminated, incremental volume collapses.

- Margin compression: marketing spend and contracting costs remain, while gross-to-net improves only marginally.

- Product life-cycle effect: the remaining installed prescriber preference decays over time unless payer policies keep brand access.

What FDA and labeling factors support SARAFEM demand in the US?

Short answer: SARAFEM demand is tied to the US label and payer acceptance for depression and related indications, with historical emphasis on PMDD.

What labeling positioning matters commercially?

- Indication fit: if a plan covers PMDD treatment with brand acceptance or requires fewer formulary exceptions, brand scripts can persist longer.

- Step edits and prior authorization: these can either suppress brand use or keep it stable by limiting switching.

- Switching rules: pharmacy policies can accelerate substitution once generic is acceptable under plan rules.

How does FDA regulatory status influence competition?

- ANDA approvals and labeling carve-outs define whether generic can claim the same indications.

- Bioequivalence approval for immediate-release forms usually enables rapid substitution, unless method-of-use exclusivity blocks specific claims.

What does SARAFEM’s competitive landscape look like in practice?

Short answer: The competitive set is dominated by generic fluoxetine products and broader SSRI alternatives. SARAFEM must compete on contracting, patient access, and prescriber behavior rather than on unique clinical differentiation.

Competitive set categories

- Generic fluoxetine: direct molecular substitute.

- Other generic SSRIs: price-anchored alternatives within the class.

- Newer agents: in managed care, some payers prefer other branded or long-cycle generics depending on negotiated rebates.

How this impacts market share dynamics

- Market share is primarily cost-driven in mainstream depression treatment.

- Market share can remain niche if PMDD-related access is maintained via patient-specific rules and long-term prescribing habits.

Does SARAFEM face biologics or biosimilar-style competition?

Short answer: No. SARAFEM is a small-molecule SSRI. The competitive risk is from generics, not biosimilars.

What manufacturing or IP barriers would block generic substitution for SARAFEM?

Short answer: For a mature fluoxetine product, the main barriers are legal (Orange Book patents and injunction outcomes) rather than technical manufacturing hurdles.

Technical manufacturing is usually not the gating factor

- Generic immediate-release SSRIs generally require bioequivalence and facility GMP compliance, which large generics suppliers can meet at scale.

- Patent infringement determination and label carve-outs decide timing more often than production capability.

What settlement and litigation history affects SARAFEM’s market timing?

Short answer: Settlement dynamics can create temporary brand revenue extensions. The brand’s financial trajectory often matches settlement dates and generic launch announcements rather than FDA review calendars.

How settlements typically reshape the revenue curve

- Pre-launch window: sales remain higher because there is no new entrant.

- Post-launch: steep drop followed by slower decay as rebate and formulary lock-in changes.

(Specific case names, docket numbers, and settlement terms are needed to map SARAFEM litigation to revenue inflection points. That requires docket-level input tied to the Orange Book patent list.)

Key takeaways

- SARAFEM’s financial trajectory is dominated by mature-molecule generic substitution and SSRI class pricing pressure.

- Remaining brand value depends on residual enforceable patents in the Orange Book and the interaction between payer policies and historical label positioning.

- Commercial dynamics typically show a post-generic “share collapse then stabilization” pattern, with limited upside absent renewed enforceable exclusivity.

- The competitive landscape is overwhelmingly generic fluoxetine and other SSRIs, not biologics.

FAQs

1) When did SARAFEM lose major US market exclusivity?

The core exclusivity for fluoxetine as an active ingredient has long since ended; remaining SARAFEM-specific protection, if any, would be limited to later-expiring Orange Book patents (formulation/process/method-of-use).

2) Can generics market SARAFEM for the same indications?

Usually yes for immediate-release small-molecule products, unless method-of-use exclusivity or patent carve-outs limit label claims.

3) How do PBM formulary tiers typically affect SARAFEM?

SSRIs are commonly tiered to favor lower net-price generics; brand retention depends on managed access exceptions, step therapy outcomes, and contract rebates.

4) Is SARAFEM at risk for ANDA “at-risk” launches?

Yes in principle whenever Orange Book-listed patents are challenged; at-risk entry risk is a function of the remaining enforceable patent list and the status of Paragraph IV litigation.

5) What commercial metrics best track SARAFEM’s financial trajectory?

Net sales and prescription share are the primary indicators, plus pharmacy claim data for generic share penetration and rebate-driven net price spreads.

References (APA)

- U.S. Food and Drug Administration. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. https://www.accessdata.fda.gov/scripts/cder/daf/

- FDA. Drug Approval Package: Sarafem (fluoxetine hydrochloride). https://www.accessdata.fda.gov/scripts/cder/daf/index.cfm