Last updated: April 24, 2026

Permethrin is a synthetic pyrethroid insecticide used across household, public health, and agricultural pest-control applications. Commercially, it behaves as a commoditized product with pricing cycles tied to raw-material costs, regulatory compliance costs, and shipment volumes. Financial trajectory is constrained by (1) maturity of core formulations, (2) substitution risk within pyrethroids, (3) periodic regulatory and label expansions that unlock incremental volumes, and (4) enforcement and resistance-management dynamics that shift demand between permethrin and alternative actives.

What drives permethrin demand by end market?

Permethrin demand is split across household/institutional insect control and agricultural uses. Each segment reacts differently to macro conditions and to regulatory supply.

End-market demand levers

Household and institutional

- Pest pressure and seasonal intensity drive consumption (inventory build before peak seasons in many regions).

- Public-health procurement cycles (vector control programs) drive lumpy orders.

- Resistance patterns shape mix versus other pyrethroids and non-pyrethroids (e.g., organophosphates, neonicotinoids, insect growth regulators).

Agriculture

- Demand tracks crop cycles and pest severity.

- Grower adoption depends on performance against target pests, availability, and local regulatory status.

- Hybrid pest-management programs influence volume shares versus competing actives.

Product form and distribution channel effects

- Permethrin’s market is typically delivered through a portfolio of formulations (e.g., emulsifiable concentrates, wettable powders, dusts, and treated materials depending on jurisdiction).

- Distribution is often controlled by regional agrochemical and pest-control networks, which affects shipment timing and working-capital needs.

How do pricing and cost structures evolve for permethrin?

Permethrin behaves like a cost-and-volume product. Pricing tends to follow (a) input costs, (b) global supply availability, and (c) competitive pricing within the pyrethroid class.

Cost structure (typical drivers)

- Raw-material costs: upstream chemical feedstocks and intermediates used to synthesize pyrethroid chemistry.

- Energy and logistics: manufacturing energy usage and shipment costs.

- Compliance and registration: ongoing costs for maintaining registrations, label updates, and dossier compliance in key jurisdictions.

- Quality and incident risk: variability in impurity profiles can create batch rejections and remediation costs.

Competitive pricing dynamics

- Peer actives in pyrethroids compete on efficacy, formulation stability, and local label breadth.

- When competing suppliers add capacity, price compression usually follows.

- When supply is constrained (maintenance shutdowns, regulatory actions, or feedstock disruptions), spot and contract prices rise.

Evidence of cyclical dynamics

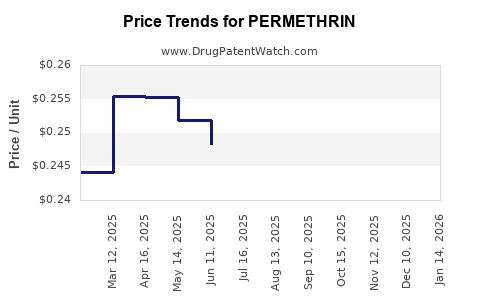

Permethrin market behavior historically reflects commodity agrochemical patterns: price spikes during supply interruptions and normalization after capacity returns. Public data on agrochemical pricing cycles is consistent with how pyrethroids price in practice, but exact permethrin-only pricing series often sits within company reporting or regional market intelligence rather than in a single public dataset.

What is the regulatory and resistance backdrop affecting revenue durability?

Regulatory changes typically affect permethrin’s allowed uses, application rates, and labeling language. Resistance affects required rotation strategies and can shift demand away from permethrin even when it remains legal.

Regulatory dynamics

- Key jurisdictions enforce maximum residue limits (MRLs), worker safety requirements, and environmental constraints.

- Continued approvals depend on ongoing hazard characterization and risk assessments.

- Any tightening of application windows or rate limits reduces effective “marketable volume” even if absolute tonnage is stable.

Resistance and performance management

- Pyrethroid resistance can lower field efficacy for certain pests, reducing farmer and public-health preference.

- Market share then migrates to pyrethroids with different target-site binding characteristics or to non-pyrethroid classes.

- Resistance-management programs can slow permethrin replacement by locking in rotational use, which supports baseline demand even under share erosion.

How does permethrin’s patent and exclusivity profile shape financial outcomes?

Permethrin is an older active with broad manufacturing footprints. That means the market is not driven by drug-like patent cliffs, but by:

- legacy registrations that determine usable market scope,

- generic-like manufacturing scale benefits,

- and formulation differentiation and regional approvals.

For business valuation and R&D investment, permethrin’s financial trajectory is less about exclusivity and more about:

- maintaining supply reliability,

- controlling manufacturing cost position,

- and updating dossiers and formulations to stay registered.

What does the financial trajectory look like in practical terms?

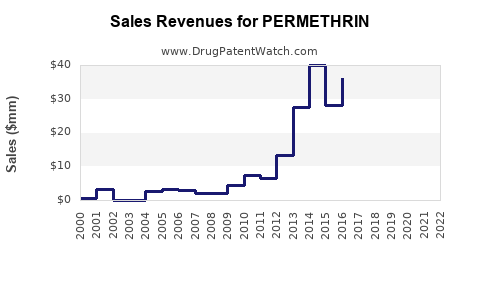

Typical revenue pattern for mature commodity insecticides

For mature, widely manufactured actives like permethrin, public-company financial trajectories typically show:

- stable-to-moderate revenue growth tied to volume expansion and price offsets,

- gross margin variability due to input cost and pricing cycles,

- working-capital swings driven by inventory normalization and seasonal procurement.

How investors and operators assess permethrin economics

- Track tonnage shipped versus ASP (average selling price) changes regionally.

- Evaluate whether revenue growth comes from price (usually short-lived) or volume (more durable).

- Watch gross margin for evidence of cost leadership versus “pass-through” pricing.

Revenue sustainability constraints

- Substitution risk within pyrethroids compresses upside.

- Regulatory rate and use-limit changes reduce marketable demand.

- Customer tendering in public health can shift pricing power toward large formulators and distributors.

How does permethrin compare with other pyrethroid actives in market behavior?

Permethrin competes within a family of synthetic pyrethroids that share similar distribution channels, procurement cycles, and formulation practices.

Substitution and share dynamics

- If a competitor active has broader target-spectrum performance or better resistance durability, share shifts away from permethrin.

- If regulatory changes favor a different active (e.g., safer profile in a jurisdiction), permethrin volumes can contract even without an outright ban.

Financial implications

- Permethrin’s upside typically tracks the health of the broader pyrethroid market.

- Downside follows (1) input-cost shocks without timely price recovery and (2) regulatory or efficacy setbacks in key pest categories.

What are the key growth pockets and downside risks?

Growth pockets

- Regions with rising vector control budgets and improving procurement capacity can expand institutional demand.

- Crop- and pest-pattern shifts can temporarily boost demand where permethrin remains an effective and permitted option.

- Formulation innovations that improve handling or reduce application burden can win share even in mature markets.

Downside risks

- Regulatory restrictions reducing permitted application rates or use sites.

- Resistance-driven efficacy declines.

- Competitive undercutting from low-cost producers during supply expansions.

Market outlook: what to expect over a 3 to 5 year horizon?

A permethrin-centric outlook typically looks like this for commodity actives:

- Demand: steady with seasonality and tender-driven fluctuations; moderate growth in regions where public health and agriculture consumption expands.

- Pricing: volatile but mean-reverting; margins depend on cost leadership and timely contract pricing.

- Competitive landscape: continued rivalry within pyrethroids; substitution pressure remains a structural headwind.

For an operator or investor, the main question is whether management can sustain cost position and protect registration and label scope, not whether permethrin can “re-invent” itself.

Key Takeaways

- Permethrin is a mature, commoditized pyrethroid insecticide whose financial trajectory is dominated by volume and pricing cycles, not by long exclusivity windows.

- Demand is driven by seasonal pest pressure in household/institutional markets and by crop-pest severity in agriculture, with public-health procurement adding lumpy orders.

- Pricing and margins hinge on input costs, global supply conditions, and competitive undercutting within pyrethroids.

- Regulatory label constraints and insect resistance affect marketable volume and can erode share even when permethrin remains legal.

- The most investable outcomes come from cost leadership, reliable supply, and maintaining registration scope and formulation performance rather than from patent-led growth.

FAQs

1) Is permethrin revenue growth likely to be driven by price increases?

Usually no. In mature insecticide markets, sustained revenue gains tend to come from volume and mix while pricing is cyclical and often mean-reverts.

2) What most affects permethrin margin volatility?

Input costs and competitive pricing shifts, which can swing gross margins more than demand itself.

3) Does resistance eliminate permethrin demand?

Not automatically. Resistance often shifts permethrin from a primary choice to a rotational or reduced-efficacy role, which can preserve baseline demand but compress market share.

4) How do regulatory changes impact commercial scale?

Regulatory limits (use rates, application windows, and label scope) reduce “marketable demand” even if manufacturing capacity stays constant.

5) Where is demand structurally steadier, household/institutional or agriculture?

Institutional/public health can be steadier in baseline terms but can be lumpy due to tenders. Agriculture is usually more seasonal and tied to crop cycles.

References

[1] U.S. Environmental Protection Agency. Permethrin: Registration Eligibility Decision (historical regulatory background). EPA archives. https://www.epa.gov/

[2] European Chemicals Agency (ECHA). Permethrin substance information and regulatory context. ECHA database. https://echa.europa.eu/

[3] FAO. Integrated pest management and pesticide use frameworks (context for resistance and use patterns). FAO resources. https://www.fao.org/