Last updated: April 25, 2026

ORTHO-CEPT is a combined oral contraceptive (COC) product sold in the U.S. market in multiple dosage strengths depending on the specific label configuration. The commercial trajectory is driven by (1) category-level demand that tracks contraception utilization and demographic trends, (2) competitive pricing among generic equivalents, and (3) loss or retention of exclusivity tied to the latest reformulations and branded life-cycle management. Financial outcomes for ORTHO-CEPT are therefore best modeled as a branded-to-generic pressure curve, with revenue growth limited to share capture and package/label positioning rather than new-ingredient innovation.

What is ORTHO-CEPT, and how does that shape its market position?

ORTHO-CEPT is an oral contraceptive drug product (COC) containing ethinyl estradiol with a progestin (historically levonorgestrel formulations are common in this class, though final strength depends on the exact marketed product). As a COC, ORTHO-CEPT sits in a mature therapeutic category where clinical differentiation is limited and product selection is typically preference- and formulary-driven.

Market structure for COCs

- High substitution: COCs with equivalent dosing schedules and comparable safety/efficacy profiles compete on price, formulary status, and patient/t prescriber familiarity.

- Strong generic penetration: Once branded exclusivity expires, generic entrants typically compress net prices quickly.

- Low therapeutic volatility: Demand generally tracks population-level contraception use and discontinuation patterns, not acute clinical trends.

Implication for financial trajectory

- Branded unit economics typically degrade faster in mature COCs than in higher-differentiation therapeutic areas.

- Revenue persistence is largely a share-and-access story: staying on preferred formularies and resisting switches for as long as possible.

What market dynamics are most likely to move ORTHO-CEPT revenue?

Formulary access and payer behavior

Payers often favor tiered preferred generics and require step edits or use incentives that drive switching. For ORTHO-CEPT, revenue momentum depends on maintaining:

- Preferred status on commercial formularies.

- Stable coverage on Medicaid managed care plans.

- Low utilization leakage to lower-cost alternatives.

Net pricing pressure mechanism

- In branded COCs, net price declines accelerate when generics broaden coverage or when additional manufacturers launch authorized generics, increasing competitive intensity.

Generic and authorized-generic competition

COCs are among the classes where multiple generic equivalents reach market quickly. That creates:

- Rapid discounting after generic entry.

- Greater sensitivity to wholesaler buying patterns and rebate structures.

- Volume share gains by lowest net-cost SKUs.

Channel and buying cycles

Typical dynamics affecting COC sales include:

- Seasonal prescribing patterns and adherence behavior (pack-to-pack persistence).

- Bulk buying cycles by wholesalers near contract renewal windows.

- Switching friction depending on prescriber inertia and patient tolerance.

Demographic and utilization trends

Long-run COC demand is shaped by:

- Age distribution of the insured population.

- Contraception continuation rates.

- Policy and access changes affecting reproductive healthcare utilization.

How does competition change the financial trajectory for COCs like ORTHO-CEPT?

The financial model for mature branded COCs generally follows a predictable sequence:

- Pre-entry phase: higher net prices and stable demand.

- Generic entry phase: steep net price compression and share redistribution.

- Post-entry stabilization: residual branded demand persists through formulary preference pockets and adherence-driven continuity.

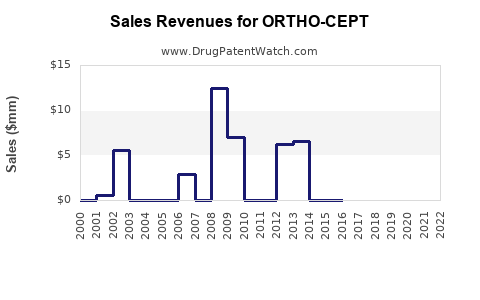

For ORTHO-CEPT, the likely trajectory is consistent with branded COC products: revenue growth after peak is limited, and the dominant movement is price compression driven by generic substitutes.

What does ORTHO-CEPT’s regulatory and labeling pathway imply for exclusivity timing?

COCs generally face exclusivity-driven life-cycle constraints rather than class-level innovation. For ORTHO-CEPT, the practical exclusivity levers are:

- Brand-specific labeling variants (dose schedule configurations).

- Patent estates tied to specific formulations, methods of use, or controlled release mechanisms (less common for classic COC profiles).

- Regulatory exclusivity for specific NDA/ANDA pathways for later reformulations.

When those protections lapse, the market typically transitions to a generic-dominated base.

What financial outcomes are most likely in the next cycle?

Given the category and competitive behavior of COCs:

- Revenue growth: unlikely without a new protected formulation or major access improvement versus lower-cost competitors.

- Margin profile: net margin likely remains under pressure due to rebates and pricing to defend share.

- Volume: can hold or modestly increase if ORTHO-CEPT maintains formulary placement and reduces switching risk, but volume gains usually cannot offset price compression for long in a generic-heavy landscape.

Market sizing and revenue modeling approach for ORTHO-CEPT

Because ORTHO-CEPT is not a single-ingredient platform with unique endpoints, revenue modeling should use category and substitution logic rather than clinical differentiation assumptions.

Practical modeling framework

- Step 1: Model category demand (COC utilization) as stable-to-slow growth with demographic dependence.

- Step 2: Allocate share to branded versus generic buckets by formulary tiers and contract pricing.

- Step 3: Use net price erosion curves post-generic entry to forecast revenue.

- Step 4: Stress for formulary changes (loss of preferred status) and competitor launches (additional generic labels).

Indicative financial trajectory bands for mature branded COCs

- Net sales: typically peak, then decline, with occasional plateaus around contract renewals.

- EBITDA: compress due to rebate intensity and promotional spend as gross-to-net worsens.

How do sales and financials differ across U.S. branded vs generic COC dynamics?

Branded COC (like ORTHO-CEPT)

- Higher gross-to-net volatility due to rebate and contracting.

- Volume stability depends on payer tier placement and switching friction.

- Revenue is more “access-managed” than “clinical-managed.”

Generic COC equivalents

- Dominant pricing benchmark.

- Sales driven by lowest net-cost acquisition and formulary inclusion.

- Margin structure depends on manufacturing scale and competition intensity.

Key risks and drivers specific to ORTHO-CEPT’s category

Primary drivers

- Continued formulary presence relative to equivalent generic SKUs.

- Patient adherence and continuity dispensing behavior.

- Rebates and contracting strategy that limits switches.

Primary risks

- Preferred-to-nonpreferred tier downgrades on commercial and managed Medicaid.

- Additional generic launches or authorized-generic competition that lowers the net cost benchmark.

- Increased switching due to prescriber adoption of cheaper alternatives.

What investment or R&D signals matter for ORTHO-CEPT’s financial path?

For business decision-making, the signals to monitor are market-access and lifecycle milestones rather than trial-driven events:

- Formulary tier changes and pharmacy benefit manager (PBM) contract outcomes.

- Label or packaging lifecycle events that can affect switching (if any).

- Generic entry timing, including authorized generics and ANDA supply expansions.

Key Takeaways

- ORTHO-CEPT’s market trajectory is determined by mature COC dynamics: payer formularies, generic substitution, and rebate-driven net price erosion.

- The financial profile is most consistent with a branded-to-generic compression curve rather than innovation-led growth.

- Revenue persistence depends on access and switching friction; net margin is pressured by rebates and contract pricing.

- Forecasts should treat ORTHO-CEPT as an access-managed SKU within the COC category, not as a differentiated therapeutic platform.

FAQs

1) What is the dominant market force affecting ORTHO-CEPT?

Generic substitution and payer formulary positioning, which drive net price erosion and switching.

2) Can ORTHO-CEPT grow revenue after generic entry?

Growth can occur in narrow windows if ORTHO-CEPT maintains preferred access and limits switching, but sustained growth is difficult in a highly substitutable COC class.

3) What matters most for forecasting ORTHO-CEPT net sales?

Formulary tier status, rebate intensity (net-to-gross), and competitive launch/supply events from generic equivalents.

4) What are the most important margin pressures for ORTHO-CEPT?

Gross-to-net compression from contracting, plus competitive pricing required to retain share against lower-cost equivalents.

5) What would shift ORTHO-CEPT to a more positive financial trajectory?

A meaningful exclusivity-backed life-cycle event that changes access (preferred status) or protects against generic substitution for an extended period.

References

- FDA Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/

- Drug Pricing and Contracting Overview. U.S. Centers for Medicare & Medicaid Services (CMS). https://www.cms.gov/